|

This months issue is a 10 min read

Download Images or Open in Browser for optimal viewing

|

| |

On May 19th, 2025, The Canadian Securities Exchange (CSE) and the National Stock Exchange of Australia (NSX) announced in a joint press release their intention to proceed with an acquisition that would see the CSE acquire all of the NSX.

For issuers, Canada and Australia have always been parallel markets with similar regulatory cultures, investor profiles, and resource-heavy economies. The CSE-NSX transaction is the first real step toward turning that parallel structure into a connected pathway - one that could materially expand access to investors, capital, and dual-market visibility.

Last week, AGM Connect - a Grove company - hosted CNSX Global Market Inc.'s Annual Meeting of Shareholders. Being in the room gave us the opportunity to connect directly with the CNSX CEO and senior leadership. It was another step in our journey that began in May to understand how this acquisition is being positioned internally, how it's being received by stakeholders, and what our clients - both issuers and investors - can expect as the CSE and NSX begin operating under a unified framework.

| | |

From TradingView

As of close on Tuesday November 25, 2025

| | Interview with Richard Carleton | |

Richard Carleton

CEO at CNSX Global Markets Inc.

| | |

Our Director of Issuer Services, Danielle Cavalcante, had the opportunity to sit down with Mr. Carleton to discuss the transaction and the implications for our clients. This interview was conducted on September 24, 2025.

How is the news being taken in Canada and in Australia? And how do you feel this acquisition will grow the CSE?

The reaction has been extremely positive whether we’re talking in Canada, Australia, or internationally.

We’re now about a month away from closing the transaction formally, remember NSX is a public company listed on the Australian Stock Exchange so there’s a lot of moving parts and it’s been a lengthy process - but we’re about a month away from closing the transaction, and we expect in a month that all of the hurdles will have been cleared, and it’s smooth sailing.

Basically, there are two motivations for the transaction.

Number one, we believe that Australians will embrace the creation of a venture exchange in Australia. Remember, there’s only one exchange listing framework in Australia. And what that means - for example for mining exploration companies, or early-stage life sciences companies, or pre-revenue technology companies – is that they have to meet the same listing requirements that much bigger, more mature enterprises have to in order to either list or to maintain their listing on the exchange. So what that means is that as you list an early-stage company, your legal counsel, your auditors, your advisors are negotiating for exemptions from the existing rules in order to get you listed on the market. That’s a lengthy process. It’s involved. There are dozens of exemptions that are required, even for a relatively simple, straightforward mining exploration company. That takes time, increases the risk and of course the expense of a going public transaction in Australia. We think that the Australian market will embrace a marketplace which is specifically designed for the needs of early-stage companies in Australia. And again, we’re very excited at the prospects of growing this market because like Canada, Australia is a dynamic public market, generates a lot of companies, especially in the early-stage space. And it isn’t all about mining. There are a number of life sciences issuers, infrastructure companies, technology companies across a wide range of disciplines that are accessing public capital. We believe we can provide a clear path to the public markets for these companies, and we think that in the domestic market it will be embraced by the entrepreneurial community.

| | |

From: Australian regulator urges lighter disclosure rules to help revive public markets

November 4, 2025

Written by Scott Murdoch

Reuters

"Under Australia's existing 'one-size-fits-all' rules small companies must meet the same listing rules as multibillion dollar corporations. ASIC said it would support the government if it introduced lighter disclosure and corporate governance frameworks for small businesses"

| | |

Now, one of the interesting things, of course, after we announced the transaction back in the spring of this year, was the positive reaction from Canada. There’s a view in the mining space across a broad range of commodities that the Australian markets provide a higher valuation for exploration stage companies than markets in Canada and the United States. So, companies are often looking to essentially exploit that valuation bump by seeking a dual listing in Australia, and raising money from Australian investment funds, who are of course experienced and knowledgeable across a number of mining disciplines.

It has been historically challenging, for a variety of reasons, for international companies to list on the incumbent exchange. And so one of the key areas of focus for us in working with our colleagues at NSX is, again, to create a better path for current international reporting issuers to dually list into Australia to better support their capital formation activities in Australia, to improve the liquidity and the price discovery for these companies and ideally, of course, help them increase the asset valuation for the company.

| Grove Director of Issuer Services, Danielle Cavalcante, with CEO Richard Carleton at their Meeting of Shareholders hosted by AGM Connect. | We have had numerous conversations over the course of the summer with international companies, principally but not exclusively from Canada, interested in listing into the Australian marketplace through the facilities of the NSX. One of the interesting aspects of our recent work in Australia is that the CSE is now recognized as a designated foreign market by the Australian Securities & Investments Commission (ASIC), the national securities regulator in Australia. There are a small handful of international exchanges so recognized, and it will make it significantly easier for CSE issuers to list onto an Australian exchange. Companies, for example, will not have to redo a lot of their continuous disclosure, quarterly financial reporting, annual audits, or be supervised closely by the Australian authorities. They accept that the home market in Canada is a recognized and well-organized and regulated marketplace and that will dramatically lessen the burden for CSE issuers looking to list their securities in Australia. There are still some challenges on the trading side, particularly in the back office. Unfortunately, the clearing and settlement facilities in Australia don’t necessarily talk all that well to the Canadian clearing and settlement facilities. This puts a meaningful burden on the transfer agents to knit the company’s the cap table back together across the two jurisdictions. But we’ve had indications of support from all of the folks active in Canada, in Australia, in the transfer agency space to address some of these concerns. | |

I was under the impression that when you do your listing to the NSX, they help you get onto the settlement system, CHESS I believe?

NSX trades clear and settle on the CHESS system, Australia’s clearing and settlement system which is owned and operated by the ASX. The challenge for an international issuer dually listed in Australia is ensuring that there is enough stock ‘on shore’ in Australia to support meaningful trading activity locally. Unlike the relationship between the US and Canadian clearing systems, where stocks are ‘fungible’ meaning the actual stock is delivered to purchasers across the border without any friction, in Australia a trust instrument (backed by physical stock) has to be created to facilitate local trading. This service, performed by the company’s transfer agent adds a layer of cost and friction to the trading process that limits the amount of cross market trading. We will be working with the transfer agents to find ways to reduce the cost and pain points for issuers and investors.

| |

I think it’s going to be very interesting to see how it shifts things for Canadian companies, and it’ll be interesting to see whether or not Australian companies take that bridge and head over here.

That is certainly possible. Again, you know ultimately it depends on your cost of capital. There are times in the business cycle where capital in Canada is more attractively priced for certain issuers than in Australia. Companies will look to take advantage.

And of course, the other benefit of a Canadian listing, of becoming a reporting issuer in Canada, is the opportunity that that opens up in the United States. Canadian reporting issuers can take advantage of the prospectus-exempt capital formation opportunities in the US, the same way that US reporting issuers can. So whether those are private placements using Reg CF, Reg A, Reg A+, the sophisticated investor exemptions, and so on, you can access the US capital markets for private placement capital to a significant degree. Most of our issuers are quoted and traded on the OTC markets in the US, meaning that an issuer can offer an organized US dollar market for US dollar investors supporting your fund raising activities with secondary market price discovery and liquidity locally. So ultimately, what we’re looking to do is to broaden access to capital for CSE companies as much as possible, give them as many options as we can. And obviously, Australia, especially in mining, technology, and life sciences sectors, is a very important source of capital in those industries.

| |

Well thank you very much for talking to me today. I’m really looking forward to seeing how this all plays out. I think it’ll be very interesting, and definitely a positive experience for Canadian companies, and Australian companies as well.

We’re very excited about the opportunity, and I guess as a final thought, I want to highlight the shared experience of the teams, because ultimately it comes down to the people involved. The folks at the NSX have gone through all of the same trials and tribulations that the team at the Canadian Securities Exchange went through about 15 years ago. And when we look at them, we see ourselves in 2010; a well-respected management team, with an interesting offering, but lacking the resources to execute on the opportunities that are presented to them. With our investment, they’ll be able to bolster the team with additional business development resources, we will be rebuilding the technology infrastructure of the company so that they will be able to provide significantly higher levels of service on the trading side. And again, just as we did 15 years ago, once those building blocks were in place, that provided us with the opportunity to grow at world-leading rates. It was very exciting and we hope to bring the same program to our friends and colleagues in Australia.

Yeah it’s great to have that support, and because you’ve been through it you know how valuable it truly is.

| | |

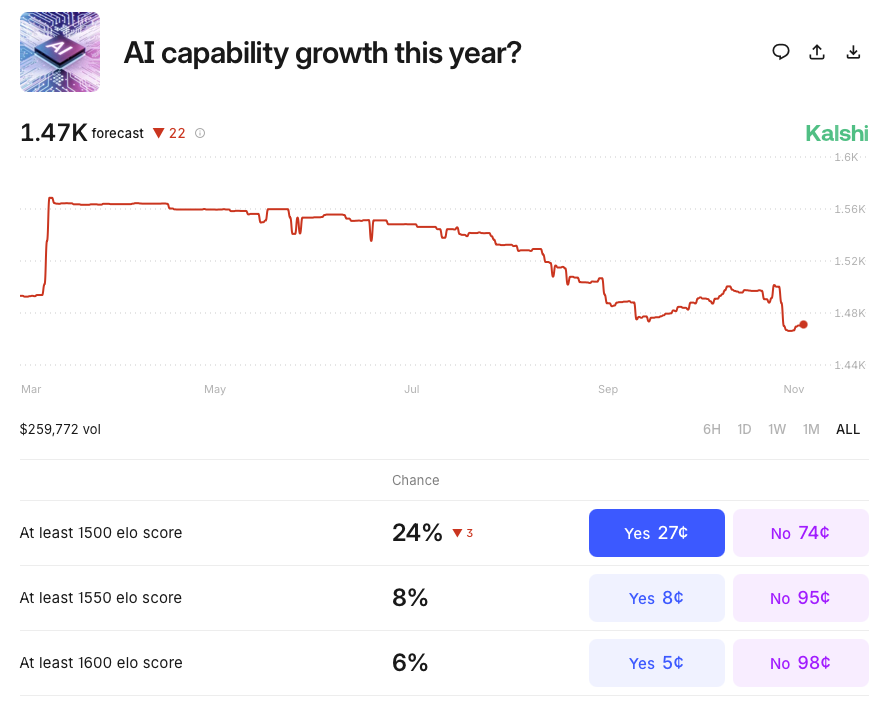

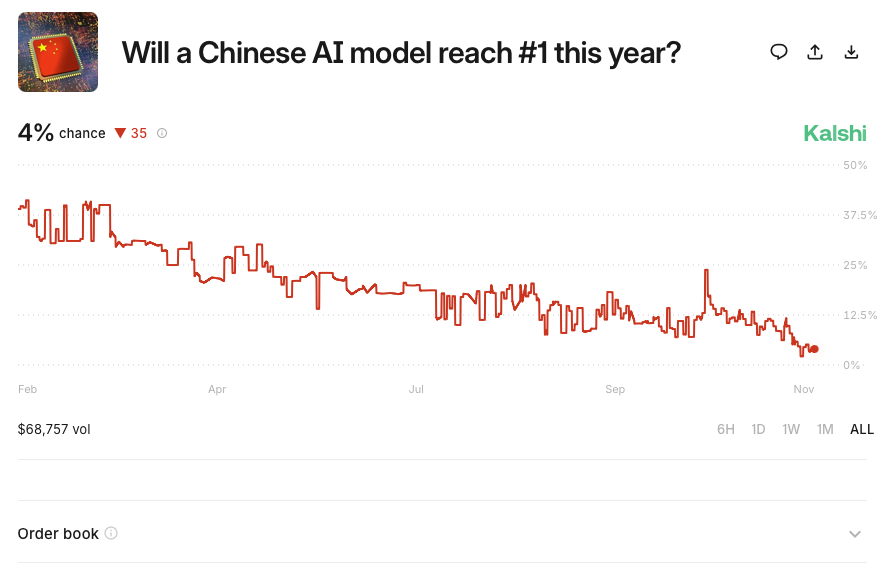

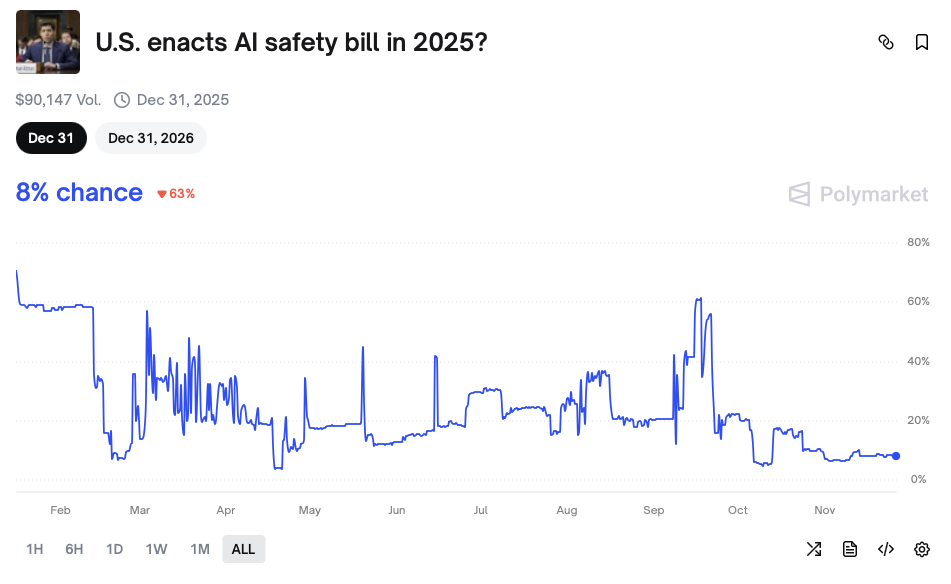

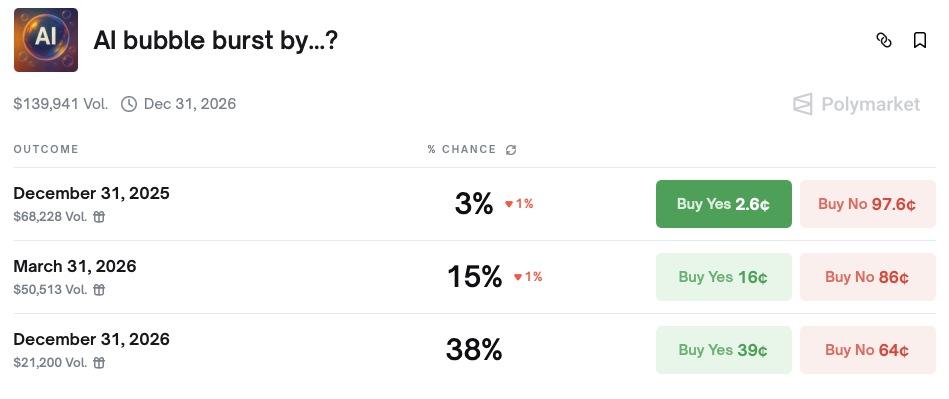

Prediction Markets offer their users a unique tool for risk mitigation and portfolio diversification.

The stock market has performed well this year in large part due to AI excitement. Companies like Nvidia and Microsoft, who have invested heavily in AI, have both had fantastic years with their share price rising 30% and 16% respectively.

However, what if all this investment doesn't equate to returns?

Below, we've provided 4 interesting predictions that an AI investor might consider as a way to mitigate against that outcome.

| | And if there wasn't any confusion, you were sure there was a bubble, but your margin account is getting hammered as excitement persists, then you can mitigate risk through a prediction on when it will happen. | | |

Where insight meets opportunity - tailored solutions and strategic guidance to help you navigate the capital markets with confidence. Reply to this email or reach out to Nick at nick@grovecorp.ca to explore how Grove can help your business.

| | From our Grove Departments | | |

Our Company | Contact Us | FAQs | Privacy Policy |

| | | |