|

Stocks Down

Middle Eastern conflict, rising oil prices, and a disappointing monthly jobs report weighed on stocks, and U.S. indexes fell for the second week in a row. The Dow finished down 2.9% on a total return basis, the S&P 500 retreated 2.0%, and the NASDAQ ended 1.2% lower.

Ex-U.S. stock indexes sustained far bigger weekly declines than their U.S. counterparts. An ex-U.S. developed-market benchmark, the MSCI EAFE Index, and an emerging-markets counterpart, the MSCI Emerging Markets Index, were both down nearly 7% for the week.

An index that tracks investors’ expectations of short-term U.S. stock market volatility climbed on Friday to the highest level since last spring’s tariff-related surge in volatility. On Friday afternoon, the Cboe Volatility Index closed at 29.5, up 48% from its closing level of the previous week.

Companies in the S&P 500 posted an average earnings gain of 14.0% over the same quarter a year earlier, according to FactSet data from the recently concluded fourth-quarter earnings season. That result marked the fifth consecutive quarter of double-digit growth. Information technology posted a 33.0% earnings gain, the highest among all 11 sectors.

Prices of U.S. government bonds fell, sending yields higher, as rising oil prices added to recent inflationary pressures. On Friday, the yield of the 10-year Treasury closed at 4.15%, up from 3.96% the previous week, when yields had tumbled to the lowest level in more than four months.

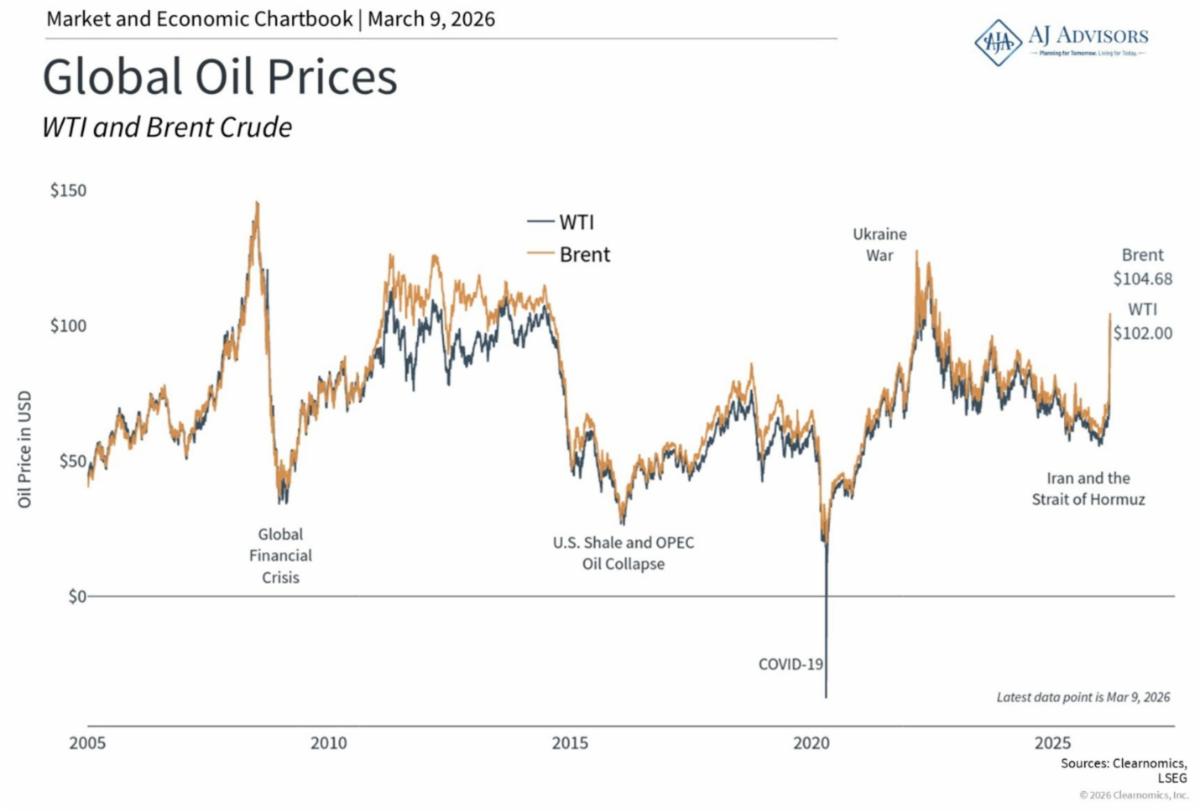

Escalating military conflict rippled throughout the Middle East, pushing oil prices to the highest levels since September 2023. With oil shipments in the Persian Gulf’s Strait of Hormuz sharply curtailed, U.S. crude was trading around $91 per barrel late Friday afternoon, up from $67 a week earlier.

February’s net loss of 92,000 jobs came as a surprise, as most economists had forecasted that Friday’s report would show a gain of around 50,000. The setback marked the third monthly job decline over the past five months, and initial figures for December and January were revised downward by a combined 69,000 jobs.

A Consumer Price Index report scheduled for release on Wednesday and a Personal Consumption Expenditures Price Index reading due on Friday could offer some clarity about inflation trends after recently divergent results. The most recent monthly CPI report showed that inflation eased to a 2.4% annual rate, while the PCE report showed a 2.9% rate, with prices rising at the fastest pace in nearly a year.

Source: John Hancock Investment Management

| | Markets and Middle East Conflict | | The ongoing conflict in Iran has seen oil prices surge from about $70 to around $100 per barrel following disruptions in the Strait of Hormuz, a key route for roughly 20% of global oil shipments. Attacks on tankers and halted shipping have forced major Middle Eastern producers to store excess oil and cut production, tightening supply and driving prices higher. This has driven significant uncertainty across global markets, with headlines mentioning a “global economic downturn,” “stagflation,” and more. | | |

It is often thought that when oil prices rise above $100, the economy starts to falter, affecting household budgets and inflation. Yet, it’s important to keep these moves in perspective. While oil prices have been quite low over the past few years, they have experienced swings throughout history. When Russia invaded Ukraine in early 2022, Brent crude surged to nearly $128 per barrel, pushing average gasoline prices in the U.S. above $5 per gallon. Before that, the mid-2000s saw oil reach record highs driven by rapid global economic growth ahead of the 2008 financial crisis. In each case, prices eventually settled as supply and demand adjusted.

Higher oil prices can raise gasoline costs, increase business expenses, and contribute to short-term inflation. However, the U.S. is better positioned than in past oil shocks due to strong domestic production from the shale revolution, which helps cushion the economic impact.

| | |

Private credit is money that investors lend directly to companies outside the public bond market. In broad terms, it’s like lending money to a local restaurant instead of buying a bond from a large national restaurant chain.

When a big chain issues bonds, its financial information is public. The bonds usually have credit ratings to help investors understand risk. These bonds also trade in public markets, so prices are updated regularly, and investors can easily see what the bonds are worth.

With a private loan, the terms are worked out directly between the lender and the company. The details are not public. The lender may get financial updates from time to time, but there is no active market setting a daily price.

Private credit can be riskier than highly rated corporate or government bonds because less information is available to the public and it can be harder to sell the assets quickly if you need your money back. To compensate for those risks, private loans usually offer higher interest payments, reported Eliza Ronalds-Hannon and Silas Brown of Bloomberg.

The private credit market has grown fast

The private credit market grew quickly in recent years as investors searched for higher returns. According to data from the Federal Reserve Bank of New York cited by Ronalds-Hannon and Brown, the U.S. private credit market more than doubled between 2020 and late 2024 and now accounts for roughly 30 percent of debt issued by below-investment-grade companies, up from 13 percent after the global financial crisis.

Typically, private credit investors include large institutions, pension funds, insurance companies, family offices, and high net worth individuals, reported Fang Cai and Sharjil Haque in FEDS Notes.

Recent investor anxiety

In 2024 and 2025, more than 50 companies restructured their debt, reducing returns for lenders, according to Ronalds-Hannon and Brown. Defaults have remained relatively low, but these restructurings raised questions about what could happen if the economy weakens.

Investor concerns about the strength of private loans also increased after a broad selloff in software stocks. Abby Latour of Morningstar noted that private credit lenders favored software companies for years because of their strong profit margins, loyal customers, and predictable subscription revenue. More recently, concerns that AI may erode those advantages, lowering barriers to entry and enabling customers to build their own software tools, caused lenders to reassess the underlying value of those loans.

While these developments bear watching, it’s unclear whether current concerns will prove prescient or overblown. Either way, private loans have become a meaningful part of the lending market, and it’s important to understand how they differ from traditional bonds.

| | |

AJ Advisors

www.ajadvice.com

|

|

|

Phone: (615) 709-8709

Fax: (615) 709-8709

| |

| |

John Stauffer, CFP®

Partner

| |

Andrew Quinn, CFP®

Partner

| | Past performance does not guarantee future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, strategy, or product (including those recommended or undertaken by AJ Advisors, LLC), or any non-investment related content, made reference to directly or indirectly in this communication will be profitable, equal any indicated historical performance level(s), be suitable for your portfolio or individual circumstances, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. You should not assume that any discussion or information contained in this communication serves as the receipt of, or as a substitute for, personalized investment advice. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to their individual situation, they are encouraged to consult with the professional adviser of their choosing. AJ Advisors, LLC is neither a law firm nor a certified public accounting firm and no portion of the content herein should be construed as legal or accounting advice. If you are an AJ Advisors, LLC client, please remember to contact the firm, in writing, if there are any changes in your financial situation or investment objectives or if you wish to impose, add, or modify any reasonable restrictions on our investment advisory services. Until so notified, AJ Advisors, LLC will continue to rely on the most recent information provided. A copy of our current written disclosure statement discussing our advisory services and fees continues to remain available upon request. | | | | |