|

|

Over 20 Years of Middle Market Investing | | | |

|

IRONWOOD CAPITAL PERSPECTIVE:

RESIDENTIAL CONSTRUCTION SERVICES AND THE

SINGLE-FAMILY HOUSING SUPER CYCLE

| |

|

In this post, we will discuss Ironwood’s perspective on the United States single-family residential construction market. The US housing market has built to sub-historic levels since the Great Recession, with numerous geographies and regions experiencing systemic housing undersupply. This, coupled with the suburbanization and near-zero interest rate trends seen in and immediately after the COVID-19 pandemic, led to a boom in single-family construction starts across several regions of the US. While the market tempered in 2023 and early 2024 as builders acclimated to a rising interest rate environment, recent interest rate declines and continuing long-term housing demand are anticipated to provide investment opportunities in this sector in the coming years.

Ironwood has long been an investor in the US construction services / products and related home services industries, investing across both new construction and renovation as well as home services businesses since our inception.

| |

|

Industry Trends

Overall, the US single-family construction market has lagged historical averages since the Great Recession. As shown below1, the overall US single-family construction market experienced a material decline in new starts during the Great Recession, a trend which has yet to revert back to pre-2008 levels. While the market saw activity increase immediately after the COVID-19 pandemic as builders and consumers alike benefitted from near-zero interest rates, these levels remain below historical averages.

| |

As a result of the above, the nation has been in a net undersupplied housing position for the past decade. Builders, having learned from the overproduction issues of the early 2000s, have been hesitant to reengage full production volumes across the nation. | |

|

In concert with the above underproduction2, consumers reaped the benefit of sub-historical interest rates for the decade following the Great Recession. As well documented, this trend was further exacerbated in and immediately following the COVID-19 pandemic amid further rate cuts.

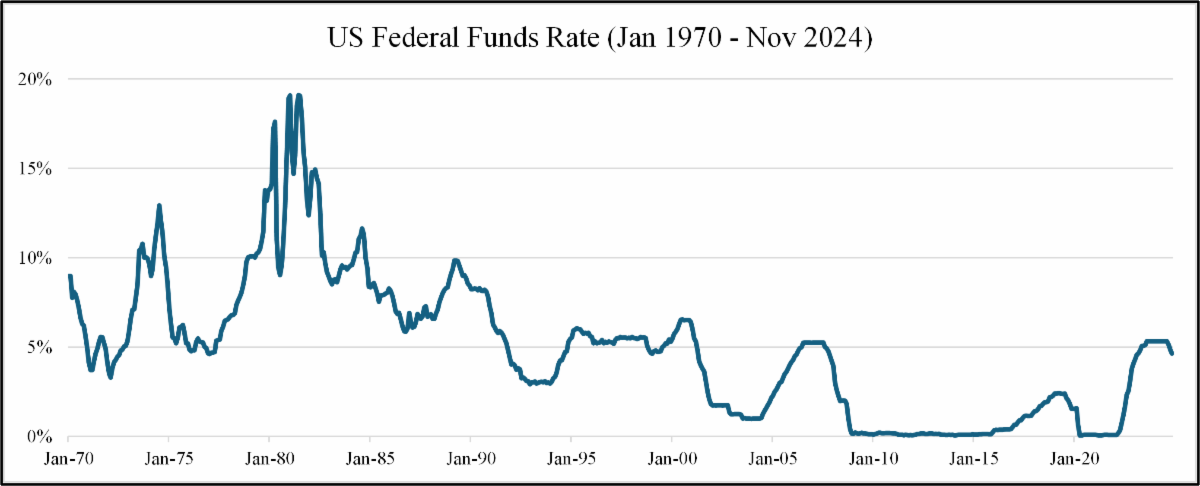

As shown below3, even as the US Federal Funds Rate was increased in 2022, rates remained at or below historical averages. Furthermore, initial rate cuts in 2024, the latest and third of which occurred in December, and the broader market sentiment that rates will remain stable to declining in the near term, are a meaningful confidence driver for homebuilders evaluating near-term construction starts.

| |

|

Another key factor regarding interest rates is the “Gridlock effect,” whereby existing homeowners hesitate to sell their homes and move as their home mortgage interest rate could double from the current rate. With homebuyers taking advantage of mortgage rates approaching 3% during the COVID pandemic, a large portion of the existing housing supply – the primary competition for new home construction – is in gridlock, meaning housing undersupply can only be satiated via new construction. While rates have stabilized at or below historical interest rate levels, mortgage rates above COVID-era rates are anticipated to drive a continued gridlock in existing housing inventory over the coming years.

Materials such as concrete saw frequent and significant price increases from 2020-2022 as a result of supply chain disruption exacerbated by growing consumer demand as a result of near-zero interest rate lending environments. In concert, labor shortages amid work-from-home mandates and government benefits led to pay increases for both manufacturing and contract labor, all of which culminated in new home price increases passed on to the end consumer.

| |

While the immediate impact of this price increase was not felt due to low-interest lending conditions, interest rate increases throughout 2022 to curb the rapid inflation seen across sectors led to monthly ownership costs increasing demonstrably for the end consumer. As evidenced in several key pricing indices – and as shown with key input costs, such as cement as shown above4 – prices have stabilized into 2024 as market demand cooled in response to the interest rate increases. | |

Another key factor in housing demand is US demographic trends. As shown below5, the nation’s population of peak first-time home buyers has experienced growth in recent years as the Millennial generation reaches peak household formation ages. Furthermore, Millennials have exhibited later participation in household formation and homebuying than prior generations, with a growing number of Millennials expected to drive near-term demand for housing. Conversely, the Baby Boomer generation is exhibiting a desire to age within their homes rather than downsizing or moving in with family or to assisted living facilities. A 2018 AARP survey, for example, denoted that 46% of Baby Boomers believe there are feasible options to age in place rather than relocating6. As these homes (32 million homes across the US) are less frequently relinquished compared to prior generations, the onus remains squarely on new construction to supply future market needs7. | |

|

Investment Considerations

The national single-family housing market remains poised for growth and represents a fragmented industry for M&A activity in the coming years. Key investment considerations include:

-

Geographic Focus: The US single-family construction market is largely driven by overall national economic performance, though housing markets are highly regional in nature, with providers’ underlying demand tied to their respective service areas. Thus, operators active in regions experiencing secular tailwinds (i.e., population and economic immigration) experience the majority of new housing demand, while regions with slowed or declining demographic trends lag behind national averages. As a result, investors heavily weigh the regional trends for potential acquisitions. Moreover, multi-regional providers offer a natural hedge against exposure to a single market’s economic outlook, with operators across several growing and non-correlated markets likely to gather increased interest by the M&A market.

-

Interest Rates: As noted above, interest rates are a primary input for homebuilders and the broader construction market. As the cost of borrowing increases, both builders and consumers react to the increased capital requirements, as evidenced in the market pause in 2023 and early 2024. The anticipated movement of interest rates is also an important confidence factor, with recent rate stabilization coupled with rate cuts driving increased confidence across the market. Also important to note, the current rate environment – stable, but at elevated levels compared to prior years – offers a unique dynamic for homebuilders, as current homeowners are reluctant to relinquish their current mortgages for a new, higher rate. This dynamic continues to support increased demand for new home construction as the solution to the nation’s present housing shortage.

-

Aging Population: The US housing markets are also experiencing a housing demand boom from the Millennial generation, who have continued to lag behind prior generations for key life milestones including marriage, homeownership, and family formation rates. Millennials, having reached college graduation age coinciding with the Great Recession and peak homebuying age amid the COVID-19 pandemic, represent significant pent-up demand for housing over the coming years.

Regarding M&A trends, US population trends also impact the housing industry as founder- and owner-operated businesses seek a change of control or liquidity event. As the US population continues to age, business owners who do not have a formal succession plan are anticipated to continue to seek liquidity events to effectuate retirement or other lifestyle changes. The “Great Wealth Transfer” refers to the anticipated transfer of $84 trillion of wealth from the Silent Generation and Baby Boomer generation to younger generations through 2045. For the lower middle market, this transfer will require a vast swath of founder- and owner-operated businesses to seek a change of control or liquidity event over the coming years.

-

Key Material and Labor Trends: Building services and material providers experienced supply chain and pricing disruption throughout the COVID-19 pandemic, with elongated lead times and surge pricing leading to frequent and significant increases in key input costs. Major materials (i.e., concrete as denoted above) experienced significant increases in recent years, while labor shortages and competition led to wage inflation both for manufacturers and contractors. As these input costs have both stabilized in 2024, pricing and margin profiles have largely reverted to historical averages. Investors continue to focus on both a provider’s historical margin profile and key pricing agreements (both for input cost purchases and customer contracts) to evaluate a company’s ability to respond to future pricing fluctuations.

-

Position in Value Chain: Another key consideration for investors is where the provider sits in their respective value chain. For building products manufacturers, products with an established name or with a differentiated product (e.g., premium vinyl windows) present a competitive differentiator compared to a generalized product manufacturer whose prices are more directly linked to commodity indices. Similarly, a provider’s customer mix (e.g., end homebuilder versus distribution or other non-end-user applications) impacts the competitive differentiation a provider is able to present in the market, as direct interactions with a homebuilder offer more service and quality differentiation versus end customers such as distributors which primarily value price as purchasing determinants.

| |

|

While less applicable for the single-family housing market, consideration should be given to multi-service providers who produce or sell into other construction end markets (e.g., multi-family, commercial, or municipal). Key considerations for non-single-family applications include bonding and/or retainage requirements for projects, as well as a greater understanding of the company’s accounting practices if operating percentage-of-completion accounting.

In summary, the single-family housing market in the US continues to experience long-term and significant undersupply, with an amalgam of market- and demographic-driven shifts driving continued demand toward new construction. Within the broader market, higher growth regions (e.g., Southeastern US) are positioned to continue outperforming the national average amid secular population and economic growth trends, representing both compelling and forecastable growth opportunities. Ironwood is actively pursuing new platforms for building product and service providers, and we look forward to sharing how our prior experience and value-added approach position us as a valuable partner.

| |

|

Ironwood Investment Experience

Ironwood’s investments in the single-family residential construction market include both active and exited portfolio companies:

-

Southern Design Companies (Active): A Cumming, GA-based provider of landscaping and concrete services across the Atlanta, GA metropolitan statistical area and the Florida panhandle. Southern Design primarily serves tier-1 national and regional residential homebuilders, as well as multi-family customers across these markets.

-

Pinnacle Contracting (Active): A Kernersville, NC-based provider of concrete and landscaping services across North Carolina and South Carolina, primarily serving tier-1 national and regional homebuilders. Pinnacle also offers multi-family services as well as masonry services.

-

Paradigm Windows (Active): A Portland, ME-based provider of premium vinyl windows to primarily new construction end markets across the Northeastern US. Paradigm offers an array of branded vinyl windows, as well as patio doors and ancillary products, to residential and commercial construction end markets.

-

Peltram Plumbing (Exited): A bicoastal plumbing services provider serving both residential and commercial construction markets in complementary yet distinct MSAs across the US. The Peltram platform initially served the Seattle, WA and Charlotte, NC markets, subsequently expanding to Mint Hill, NC, as well as Houston, Dallas-Fort Worth, and San Antonio, TX. Following these initiatives, Ironwood’s investment in Peltram culminated in a sale to an institutional buyer.

For a complete list of Ironwood Capital’s investment experience, please visit our website: www.ironwoodcap.com/portfolio.

| |

We’re excited about the opportunities we see in the residential construction services sector and are actively evaluating investments aligned with this thesis. To learn more, please visit our website and reach out to one of our team members: | |

The information contained herein has been obtained from sources believed to be reliable, but the accuracy of such information cannot be guaranteed. Views expressed are as of the date provided. Ironwood is under no obligation to update this information or to advise on further developments relating to the investments discussed herein. References to a particular investment is not a recommendation to buy or sell such investments. The information contained in this document is prepared for general circulation and is circulated for general information only. Past performance is no guarantee of future results. Any investment contains risk including the risk of total loss. There is no assurance that the investment objectives will be achieved or successful. Please refer to the Firm’s Form ADV 2A Brochure for more information about the Firm, services and fees on file with the SEC, www.adviserinfo.sec.gov. Firm CRD #321642. You may also contact us at 860-409-2100 or visit our website for a complete list of investments at www.ironwoodcap.com. | |

|

Works Cited

1 - Pew Research Center, Pew Research Center, 3 Mar. 2023, www.pewresearch.org /Raymond James, Raymond James Building Products Newsletter, Sept. 2023, www.raymondjames.com/-/media/rj/dotcom/files/corporations-and institutions/investment-banking/industry-insight/building_products_quarterly_newsletter.pdf

2 - Vanguard Research. “U.S. Housing: Cyclical Weakness, Structural Strength.” Vanguard, 8 June 2023, https://corporate.vanguard.com/content/corporatesite/us/en/corp/articles/us-housing-cyclical-weakness-structural-strength.html.

3 - FRED, Federal Reserve Bank of St. Louis; www.fred.stlouisfed.org/series/FEDFUNDS/.

4 - IBISWorld. “IBISWorld - Industry Market Research, Reports, and Statistics.” IBISWorld Industry Reports, 22 Aug. 2024, www.ibisworld.com/us/bed/price-of-cement/190/.

5 - United States Census Bureau Bureau, US Census. “Data.” Census.gov, www.census.gov/data/

6 - Binette, Joanne, et al. “2018 Home and Community Preferences: A National Survey of Adults Ages 18-Plus.” AARP, AARP, 31 July 2019, www.aarp.org/pri/topics/livable-communities/2018-home-community-preference/.

7 - “Housing Insights: The Coming Exodus of Older Homeowners.” Fannie Mae, www.fanniemae.com/media/20281/display.

| | | | |