| | 631-923-2485; 888-342-6436 | | Investment Newsletter - Q4 2025 | | |

Greetings! Fall is upon us and the leaves and calendar changing (as well as coffee shops nationwide frantically adding pumpkin spiced everything to their menu) means we have another quarter to recap and a brand new one to look forward to.

On the equity front the story of the quarter - and really the year so far has been very similar to the most recent main story in the world of sports; world outperformance. Much like the Justin Rose led European Ryder Cup team which retained the Ryder Cup in Landmark’s backyard, Bethpage Black, international equities continued to outpace their American contemporaries. With that said the market, as measured by the S&P 500, still had a very solidly positive quarter.

On the fixed income front we finally saw a rate cut, in September, of twenty five basis points, which gave a small boost to bonds while also keeping yields relatively attractive. The general markets consensus seems to be that there will be one or two more rate cuts in the year (however, market predictions are just that, predictions and should be taken with a grain of salt as the market is generally unpredictable), but with softer than expected job numbers and inflation that is remaining sticky, as well as a government shutdown and potential tariff impacts, the Federal Reserve will once again have to be careful in navigating when and how much more to cut rates.

We give you a deeper insight into our thoughts on the past quarter and an outlook for Q4 further below. If you would like, we also have a link to the S&P Global economic and market outlook for Q4 2025 (click here), and BlackRock's Q4 market outlook for 2025 (click here).

In this issue of our Investment Newsletter:

-

Our investment topic this issue is: "The Benefits of a Currency-Neutral Strategy"

- Recent articles where Landmark Wealth Management was quoted in the press

- An overview of recent market activity, along with Our Perspective...

- A recap of the performance of major market indices from the past quarter

- Upcoming Economic Calendar

You will find past investment articles, by clicking the Articles tab above, or directly on our website, found under Periodicals.

If there is a topic of interest you would like to see covered in the future, please reply back to this email to let us know, or click here. Likewise, if you have any questions on this or anything else, feel free to reply back.

| | |

"The Benefits of a Currency-Neutral Strategy."

For our investment topic, "The Benefits of a Currency-Neutral Strategy" we give our thoughts and suggestions. To learn more, please click here.

Please note - this investment topic, as well as past investment topics, can be found on our website under the Articles tab, or you can click here.

| |

Landmark Wealth Management Quotes in the Press | | |

The past few years, Landmark Wealth Management has been quoted in the press for various articles. We have decided to start sharing these when they happen. If curious about past times we were mentioned, you can see it on our website under Articles > In The Press, or simply click here.

______

From an article on the website MarketWatch: "‘I am clueless.’ I am 65 and had $100K in my 401(k). An adviser put it all into an annuity, promising a 10% return. Now what?" To access this article, please click here.

______

From an article in Moneyasif.com, "Should you have an annuity?". To access this article, please click here.

______

From an article that was on the website MarketWatch: "‘Is all hope lost?’ I’m 65, make $40K a year and will get $1,890 a month in Social Security. I live in my late mother’s house and want to retire at 70. Who can help?". To access this article, please click here.

| | Our Perspective on Recent Market News and Activity | | Our synopsis of the past quarter, a look ahead, and putting it all in perspective: | | |

In contrast to last quarter, Q3 was much less volatile. Despite this, there still remains much to recap and much to anticipate in Q4.

The Federal Reserve cut rates in September by 25 basis points, which wasn’t a particularly shocking decision. The latest jobs report being somewhat disappointing seemed to be what galvanized this move, although the Federal Reserve likely looked at many factors before ultimately making their call. Market prognosticators still believe there will be additional rate cuts in the year (which should always be taken with a grain of salt) however, inflation remains sticky, hovering around 3% per the latest print. With this in mind, it may be difficult for the Federal Reserve to make additional cuts, although the aforementioned consensus is that one or two more cuts are in store for later in the year.

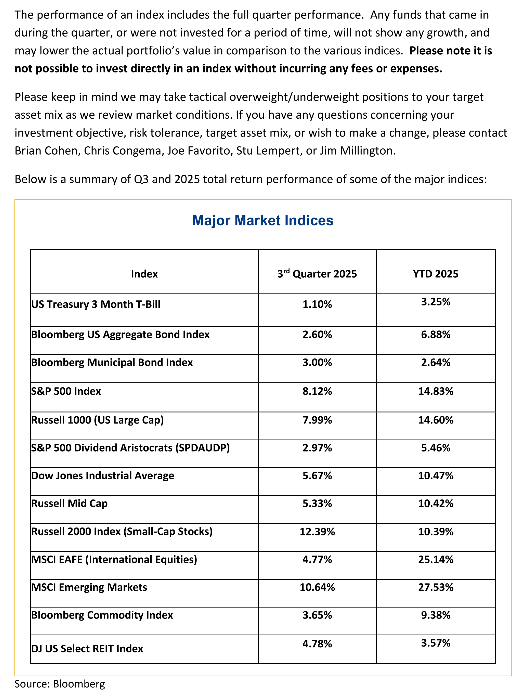

Looking at equities, the S&P 500 had a strong quarter (in fact the strongest Q3 since 2020) and returned nearly 8%. U.S. small-caps (as represented by the Russell 2000) continued their extremely positive momentum from Q2 and managed to close Q3 up around 12%. The Russell Mid-Cap index also posted a solid Q3 closing up around 5%. International equities continued their steady rise as the MSCI EAFE (developed international equities index) posted another positive quarter while the MSCI Emerging Markets Index posted another double-digit positive return after it did so in Q2.

Fixed income saw a truly meaningful increase in return because of the previously discussed rate cut in September, and closed up around 2% in Q3, as measured by the Bloomberg Aggregate Bond Index. Municipal bonds also received a similar lift, although it remains to be seen if any of their returns will be affected by the government shutdown and advanced talks of reduced government spending.

While the previous quarter (Q2 2025) was a story of volatility Q3 2025, in retrospect, was a story of solid positive momentum. The market continued its trend of broadening out beyond just the top names in the S&P 500 and NASDAQ and most sectors, including fixed income, were positive for the quarter. A big concern entering Q3 had been whether the market would react well to The Big Beautiful Bill and the market reacted positively, much to the delight of investors everywhere. With all this positivity in the market, it bears repeating: this is not the time to abandon your asset allocation and try to chase excess returns. Having exposure to many different asset classes both allows you to participate in times like this and keeps you safe should markets come back down to earth.

Looking ahead to Q4 there are a few key outstanding questions that will likely shape how the market performs. First, the recent government shutdown has produced some amount of uncertainty in the market, given that it will delay knowing for certain how much government spending is on the horizon. Next, tariffs (as they were in the beginning of the year) are in the headlines as the current administration has both threatened to levy more and is fast approaching the enforcement date of tariffs placed on certain nations such as China.

If it has been a while since we last sat down and went over your own personal numbers, we encourage you to make an appointment and meet with us for a review.

| | Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns. | | Below is the Q3 '25 total return performance of some of the major indices: | |

On The Investment Horizon | | |

Upcoming Key Dates on the Economic Calendar

- First Friday of each month: Unemployment report for the prior month, released at 8:30AM.

- Tuesday, October 28th - Wednesday, October 29th: The Federal Open Market Committee (FOMC) meets, and releases their announcement on Wednesday at 2PM.

-

Wednesday, October 30th - Gross Domestic Product, 3rd Quarter 2025 (Advance Estimate)

-

Tuesday, November 26th - Gross Domestic Product, 3rd Quarter 2025 (Second Estimate) and Corporate Profits (Preliminary)

- Thursday, November 27st- Thanksgiving: US Markets Closed

- Tuesday, December 9th - Wednesday, November 10th: The Federal Open Market Committee (FOMC) meets, and releases their announcement on Wednesday at 2PM.

-

Friday, December 19th - Gross Domestic Product, 2nd Quarter 2025 (Third Estimate), GDP by Industry, and Corporate Profits (Revised)

- Thursday, December 25th- Christmas Day: US Markets Closed

- Thursday, January 1st- New Years Day: US Markets Closed

| | We Value Your Opinion - Leave a Review Today! | | If you would like to leave a Google Review for our services, please click the link below to do so. If you are not signed into Gmail, when you click the link, you will be prompted to sign in and then you can leave a star rating and review. If you do leave us a review, thank you for doing so as it helps Landmark with online visibility and allows us to see the ways in which we impact our clients. | | |

General & Contact Information | | |

For our clients - You should have received your statement directly from our account custodian, Charles Schwab & Co. If you have not, please let us know so that we may investigate the matter. Please review your statement carefully and let us know if you have any questions or comments.

Also, as a reminder, our office has a nice sized conference room to use for our meetings and updates. If you do not feel comfortable coming into our office or if it is inconvenient, we recommend that we set up a Zoom or teleconference call to update your planning numbers, especially if it has been more than a year since we have last done so. Please feel free to reach out.

For everyone - If you desire an appointment, have any questions on any of this material, or any other financial subjects may relate to your own financial circumstance, please reach out to us at the contact information below:

Sincerely,

Brian Cohen, CCO; email: brian@landmarkwealthmgmt.com; phone: 631-923-2487

Chris Congema, CFP®; email: chris@landmarkwealthmgmt.com; phone: 631-923-2486

Joe Favorito, CFP®; email: jfavorito@landmarkwealthmgmt.com; phone: 631-930-5336

Jim Millington, CFP®; email: jim@landmarkwealthmgmt.com; phone: 631-470-0765

Aaron Belletsky; email: aaron@landmarkwealthmgmt.com; phone: 631-982-8049

Stu Lempert, CWS®; email: stuart@landmarkwealthmgmt.com; phone: 631-485-3055

Direct office email: info@landmarkwealthmgmt.com

Direct phone: 631-923-2485 or 888-342-6436

| | | | |