|

Win $50!

|

|

There are two member numbers spelled out within the text of this eNewsletter. Find your number and give us a call at (888) 387-8632 to claim $50!

|

|

|

|

|

|

ONLY TWO MORE WEEKS TO

TAKE ADVANTAGE OF THIS OFFER!

*Referred person must be 15 years of age or older, eligible for membership with 1st Northern California Credit Union, present a completed referral form when they apply, and become a member for referring member to receive the $25 deposit into their share account. Current members may refer up to 4 new members. Offer ends September 30, 2016.

|

President's Corner President's Corner

|

Wells Fargo's $185 million fine by federal and state bank regulators for the widespread illegal practice of secretly opening unauthorized deposit and share account would almost be funny if it weren't so revolting. The credit union industry has been buzzing about the outrage about 5,000 of the bank's employees essentially defrauding their customers all for the sake of hitting their compensation incentives. Outrageous? Yes. Surprising? Not so much.

After the financial meltdown ten years ago, Congress created the Consumer Financial Protection Board (CFPB), a multi-headed monster to originally oversee the "too big to fail" banks, which include Wells Fargo, to ensure the banks' financial shenanigans would not recur. According to the CFPB's press release announcing the fine, "...employees boosted sales figures by covertly opening accounts and funding them by transferring funds from consumers' authorized accounts without their knowledge or consent, often racking up fees or other charges."

Prior to working at 1st Nor Cal, I audited credit unions for over ten years. Auditors have a word describing covertly opening accounts and unauthorized funds transfers: Fraud. It's really that simple. Creating phony accounts for the purpose of personal financial benefit is fraud. My bosses at the CPA firm asked us to tiptoe around the "F" word and use less provocative terms such as unauthorized, erroneous, nonexistent, improper, and misleading. Make no mistake. What Wells Fargo did was commit Fraud, with a capital "F."

These 5,000 employees were fired. However, these employees didn't independently come up with this scheme. Someone, probably originating high up in Wells' bloated bureaucracy, was the brains of this policy. Has this person or persons been identified? Have they been fired? Has anyone involved in this debacle been convicted of fraud and thrown in a prison cell?

Sadly, the likely outcome is that there will be no senior executives getting punished. Besides the monetary fine which includes refunds to more than one million affected customers, the bank must hire an independent consultant to conduct a thorough review of its procedures and require employees to undergo ethical sales training.

The largest banks have been using unethical sales tactics for years. Most don't get caught. The few that do merely get a slap on the wrist. While $185 million is hardly a slap, it won't affect their business plan or profitability going forward. Senior management will still get their large salaries and stock options. I will be looking to see how many customers close their accounts to protest these corrupt actions. Sadly again, most people don't pay attention, so the loss of accounts will hardly register a blip. The only way to stop bad behavior is to hit them where it hurts-in the old money belt.

David M. Green

President/CEO

(925) 335-3802

|

Stat-of-the-Month

|

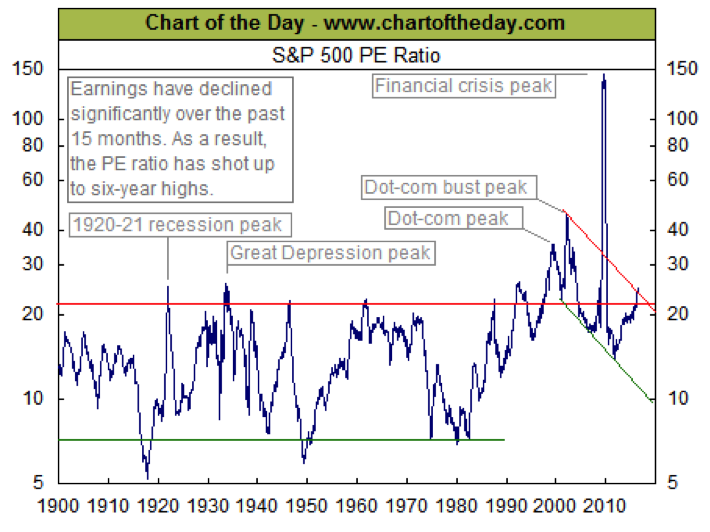

This chart illustrates the price to earnings ratio (PE ratio) from 1900 to present. Generally speaking, when the PE ratio is high, stocks are considered to be expensive. When the PE ratio is low, stocks are considered to be inexpensive. From 1900 into the mid-1990s, the PE ratio tended to peak in the low to mid-20s (red line) and trough somewhere around seven (green line). Notice how most PE ratio peaks that occurred well above the upper threshold (red line) were a result of a massive bear market / recession. The only real exception to this was the dot-com boom which resulted in a PE ratio peak well above 30 in 1999. Viewed in this way, the current PE ratio (25) is noteworthy and suggests that the stock market as a whole is by no means cheap.

[SIX EIGHT ONE FIVE SEVEN]

|

1st Nor Cal Updates

|

NEW Expanded Hours!

NEW Expanded Hours!

Monday - Wednesday: 9:00 am - 4:00 pm

Thursday: 9:00 am -

6:00 pm

Friday: 9:00 am - 5:00 pm

|

Disneyland has discontinued their corporate ticket discount program as of September 15th, 2016. There's a great selection of other discounted theme park tickets still available to our members. Visit our

Member Discounts

page to learn more.

|

In an effort to have all Californians comply with the required Electronic Lien for vehicle titles, DMV will no longer accept a paper form to release a title. Titles must be released through DMV's electronic system. What does this mean to you? When you pay off your car/truck loan, our DMV specialist will put in an electronic request, and you will receive your title in 5 to 7 days. Your title will no longer be available at the Credit Union. It will come directly from DMV.

|

Tips for Teens

|

The Key to Keeping Kash

Fal

l is almost here. The air feels cooler, the leaves are beginning to change color, and Starbucks is serving Pumpkin Spice Frappuccino's again! Also, school is back in session, so by most accounts, Fall is already here.

Recently, in my first period class, I was seated with a group of not-so-savvy shoppers. It seemed to me that their biggest problem was not having a budget. They complained about how quickly their money disappears when they go out. When I suggested to one of my classmates to consider a budget, her response was, "Budgets?! I don't do budgets. I spend on the things I like, when I see them." Another classmate said that when he gets his paycheck, he's overwhelmed by the things he could spend his money on.

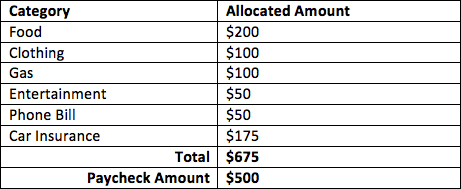

You don't need a Master's Degree in Finance in order to create a budget. Let's start by considering your income. Let's say you make $500 dollars in a month. Next, think about what you spend your money on. If you have no idea where your money disappears to, check your statements and categorize by the places you shop. For example, if Starbucks, Safeway, and Subway appear on your statement (thank you English teachers for teaching me alliteration!), then you should categorize them as food. You'll want to find the average amount you spend monthly for each category. To find the averages, total up each category for a span of at least a few months, then divide those totals by the number of months you're working with. Categories like food, clothing, gas, and entertainment are examples of

variable expenses, meaning that they might change each month. You might spend more on clothing in August then you would in February. That's why they're called variable. For this example, let's say that on average, you spend $189 on food, $86 on clothing, $65 on gas, and $40 on entertainment. Then there's your

fixed expenses, which include bills such as a phone or car insurance. Let's say you spend $50 dollars on your phone bill and $175 dollars on your car insurance. You'll want to make a table like the one below. You can do this on paper or you could download a spreadsheet app on your phone or laptop to create your table. Find your averages and add them to the table along with your fixed expenses.

Notice how I allocated an amount for each

variable expense category that is slightly above their averages. This is to be sure you have enough for those extra expenses when they arise. The totals here have exceeded the paycheck amount. Based on this budget, you would spend your entire paycheck, and then some. What this means is that you have to intentionally cut back your spending within some of your

variable expenses categories. You can change your spending habits but not your

fixed expenses. This is why budgeting is important! You can easily see why you might be running out of money each month and start making changes to stay on track.

Now that you've established a budget, stick with it! If the allocated amount for a certain category is less then what you need, find another category that you can cut back on. Make it work for you. It's your budget!

Luis Dominguez

Student Social Media Intern

1st Nor Cal Credit Union

|

The Cost of Procrastination

|

By Jason Vitucci, CFP & Gene A. Schnabel

Some of us share a common experience. You're driving along when a police cruiser pulls up behind you with its lights flashing. You pull over, the officer gets out, and your heart drops.

"Are you aware the registration on your car has expired?"

You've experienced one of the costs of procrastination. Procrastination can cause missed deadlines, missed opportunities, and just plain missing out.

Procrastination is avoiding a task that needs to be done-postponing until tomorrow what could be done today. Procrastinators can sabotage themselves. They often put obstacles in their own path. They may choose paths that hurt their performance.

Though Mark Twain famously quipped, "Never put off until tomorrow what you can do the day after tomorrow." We know that procrastination can be detrimental, both in our personal and professional lives. Problems with procrastination in the business world have led to a sizable industry in books, articles, workshops, videos, and other products created to deal with the issue. There are a number of theories about why people procrastinate, but whatever the psychology behind it, procrastination potentially may cost money-particularly when investments and financial decisions are put off.

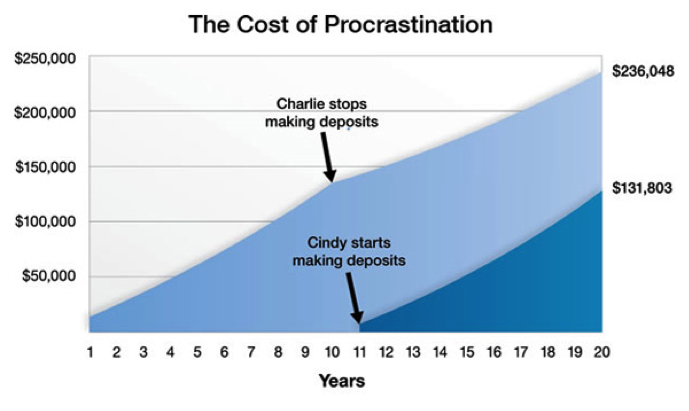

As the illustration below shows, putting off investing may put off potential returns.

If you have been meaning to get around to addressing some part of your financial future, maybe it's time to develop a strategy. Don't let procrastination keep you from pursuing your financial goals.

Early Bird

Let's look at the case of Cindy and Charlie, who each invest $100,000.

Charlie immediately begins depositing $10,000 a year in an account that earns a 6% rate of return. Then, after 10 years, he stops making deposits.

Cindy waits 10 years before getting started. She then starts to invest $10,000 a year for 10 years into an account that also earns a 6% rate of return.

Cindy and Charlie have both invested the same $100,000. However, Charlie's balance is higher at the end of 20 years because his account has more time for the investment returns to compound.

At Vitucci Integrated Planning, we are happy to take a look at your current retirement plan. As a valued credit union member, we invite you to contact us for a complimentary financial planning meeting. We also invite you to attend any of our Retirement Planning workshops that we hold. We have a workshop coming up on Saturday, October 1st. For more information about our practice, our workshops, or to make an appointment, please call us at (925) 370-3750 or visit our website www.vitucciintegratedplanning.com.

Vitucci Integrated Planning

1330 Arnold Drive, Suite 249

Martinez, CA 94553

Securities through First Allied Securities, a registered broker dealer, member FINRA/SIPC. Advisory services offered through First Allied Advisory Services, Inc. Registered Investment Advisor. Investments not FDIC or NCUA/NCUSIF insured, not insured by Credit Union, may lose value. Products offered are not guarantees or obligations of the Credit Union, and may involve investment risk including possible loss of principal.

1st Nor Cal CU, Bay Area Retirement Solutions and First Allied are all separate entities.

Gene A. Schnabel CA Insurance Lic.: 0663016, Jason Vitucci CA Insurance Lic.: 0F59894

The graph pictured is a hypothetical example of mathematical compounding. It is used for comparison purposes only and is not intended to represent the past or future performance of any investment. Taxes and investment costs were not considered in this example. The results are not a guarantee of performance or specific investment advice. The rate of return on investments will vary over time, particularly for longer-term investments. Investments that offer the potential for high returns also carry a high degree of risk. Actual returns will fluctuate. The types of securities and strategies illustrated may not be suitable for everyone.

|

FREE Financial Counseling

|

Are you in need of financial counseling?

1st Nor Cal is here to help. Timely and honest debt advice is available to our members at no cost or obligation. Learn how to manage your finances.

(EIGHT ZERO ONE EIGHT)

Make your appointment TODAY!

Just a reminder, you can annually request FREE Credit Reports from all 3 credit reporting agencies online by going to:

For FREE Financial Counseling, don't hesitate to contact:

Shelley Murphy

Senior Vice President of Lending & Collections

(925) 228-7550 Ext.824

|

Did you know we're on Social Media?

|

New Video - 1st Nor Cal vs Big Bank

|

|

|