|

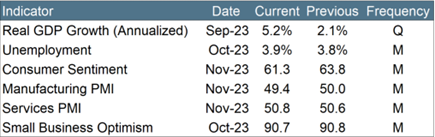

In Q3 2023, the U.S. economy grew at a 5.2 percent annual rate, up from 2.1 percent in Q2. This was the strongest growth since Q4 2021. Consumer spending, the largest contributor to the increase in GDP, grew at an annualized 3.6 percent. The second largest contributor to GDP growth was private inventory investment, including wholesale trade, manufacturing, and retail trade.

In October, Small Business Optimism registered 90.7, near even with September’s reading of 90.8 and remaining below the 49-year average of 98. The decline reflects persistent inflation concerns and a negative outlook for future business conditions. Labor challenges remain significant, with 43% of owners struggling to fill job openings. To address these challenges, business owners noted plans to raise compensation.

In Q3 2023, the CFO Survey's average optimism rating for the U.S. economy was 56.2 out of 100, slightly up from Q2. Approximately 40% of CFOs are cutting back on spending amid indicated heightened concerns around monetary policy, labor quality, and weak demand. Looking ahead, CFOs anticipated an improved 2024, expecting revenue growth of over 6% and nearly 4% employment growth.

|