Mile Marker Newsletter - January 2022 |

|

Hello All-

As most of you know, it’s been a very busy few months for our team. We are quite happy with our decision to move, but this transition period has been fairly labor intensive and we appreciate your patience with us as we’ve been working through it.

It’s been a while since I’ve been able to dedicate the necessary time to write these, but I really enjoy writing and it’s good to be back at it---and this is certainly the right moment to get something out!

With the recent volatility we’ve been experiencing, I think it’s important to review three important things. The first is the role my team and I play (and don’t/can’t play) as financial/investment advisors, our methodology, and the importance of owning stocks for the longevity of your assets, especially at a time like this when bond yields relative to the inflation rate are quite concerning.

1. Nobody, even those of us in this business, can with any consistency or precision forecast the direction of stock prices on any given day, month, or year. A famous economist John Kenneth Galbraith (which happens to be my middle name!) famously said “Economic forecasting exists to make astrology look respectable.” Similarly, we also cannot forecast the markets with any consistency or precision. And lastly, we cannot, based on past relative performance, forecast the future relative performance of equity portfolios. No one can do these things, plain and simple. With that being said, great advisors thus deal not in prediction and “performance”, but in planning, perspective, and behavioral coaching. Since advisors can’t forecast the economy or time the markets with much accuracy, nor say for sure which equities will outperform at any given point in time, regardless of the way markets are zigging or zagging at any given moment, you should expect us to act on opportunities as they present themselves (tax loss harvesting and/or more attractive valuations/buying opportunities for certain stocks), but otherwise take the position that if your goals haven’t changed, and if your portfolio was built to fund those most cherished long-term goals (and it was), then there is probably no compelling reason to change the portfolio.

|

|

2. So, if we’re not prognosticators, what is our role then? How do we go about selecting what goes in the portfolios? Traditional money managers will try to look for an ‘edge’. Overly confident in their ability to pick winners, these managers assume they have some predictive ability and knowledge of the future. And clearly, no one has that. Worst, this outdated approach fuels a portfolio mispricing risk which can significantly erode returns over time. We believe that instead of trying to pick winners, managers should simply avoid the companies who are weakening from both a fundamental, and technical perspective. We work with two major research partners: Goldman Sachs and Nasdaq/Dorsey Wright, and tap into the research done by thousands of analysts who are determining which companies (that you might otherwise find in the S&P 500 ETF) are showing signs of deterioration, and look to either avoid them altogether, or try to exit more quickly. Quite simply, picking winners is a losing game—so we’re simply looking for weakness (which we feel is easier to spot) and seeking to weed out the losers sooner in the game. Hand in hand with this philosophy, we believe that overall, clients will benefit when they focus on “time in the market” rather than “timing the market.” Rather than trying to benefit by tactically going to cash or bonds, which raises the second and more complex question of when to re-enter the market, a better approach is to exhibit patience in times of market duress and realize that a market recovery will ultimately prevail, since every stock market sell-off in history has historically led to all-time market highs. By making tax-and price-based judgments of stocks, we accomplish he dual goal of harvesting tax-losses on an ongoing basis, as well as quickly exiting losing positions. |

|

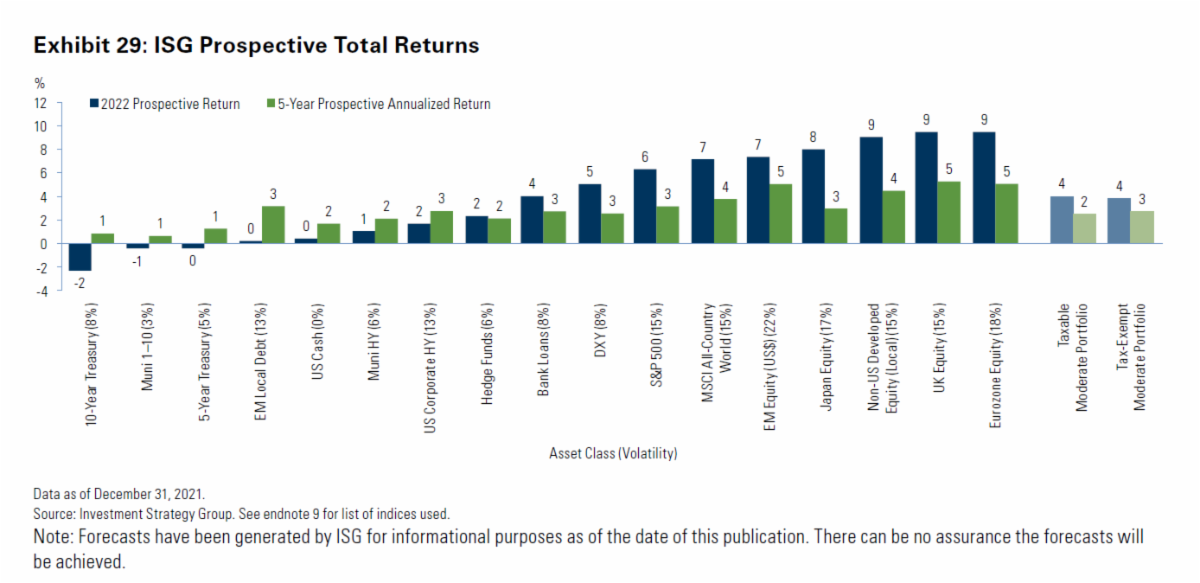

3. Moments like this, where we’re seeing 10%+ corrections, can obviously be quite worrisome when it comes to your life savings. The first thing I’ll say is--remember that you’ve hired us to do the worrying—and just do your best to trust that all hands are on deck paying close attention to both opportunities to buy other stocks at attractive price points, and of course to try to mitigate losses when there may be concern regarding changing outlook for particular stocks. As we know, stock-price fluctuations are more volatile than bonds, and this volatility can be quite unpleasant, which can result in the temptation to hedge or move into other less volatile assets. Furthermore, in a historically low interest rate environment like this, even with the likelihood of two or more rate hikes this year, and the prospect of sustained high inflation rates, we need to be very, very careful. When you invest in stocks, you’re an owner of businesses. When you invest in bonds, you’re a lender to businesses (or governments). All of our common sense and all of our own life experience tell us that owners of good businesses make more money than do their lenders, if only because owners take more risk. Historically, net of inflation (very important factor right now), the real returns to the owner have been upwards of three times of the loaner. And with lower interest rates likely to persist for years to come, coupled with inflation, the gap between stock and bond returns is likely to widen further. Goldman Sachs highlights this and drives home the point in the 2022 prospective returns for this year, and on an annualized five-year outlook: stocks will dominate with a global index (MSCI ACWI) expected to generate 7% return this year, and 4% annually going forward, vs more meager returns for bonds: |

|

(Source: Goldman Sachs 2022 Outlook: Piloting Through page 27) |

|

What’s important to highlight next is that we humans fear loss much more than we hope for gain. Therefore, we can react much more emotionally to declining markets than to rising ones. This can sometimes lead to irrational decisions to sell stocks (in spite of their annual 9% returns over the long run) and move to cash or other less volatile asset classes. But in the long run, an adequately diversified stock portfolio’s performance is quite predictable. Volatility isn’t risk, and temporary decline isn’t loss. Volatility, viewed through the appropriate lens, is nothing more than an opportunity to upgrade your portfolio and capture taxable losses. If you do not panic, you will not sell. And if you don’t sell (again, an adequately diversified portfolio), you do not lose. So, what I’m getting at is that the greatest risk for us to pay attention to in terms of longevity of your assets is actually not owning enough stocks, especially right now with bonds paying so little, and with inflation being so high. In other words, the real long-term risk of stocks is not owning them. This is a risk that most people totally underestimate. But it’s more true now than ever, as stocks continue to be our best long-term protection against high inflation. So not owning equities, especially during a 30-year retirement, will prove fatal to wealth. If you think that what you don’t own can’t hurt you, think again. Investments that get ravaged by decades of rising living costs, and are not able to preserve purchasing power, are in fact ‘risky’. At the end of the day, there’s no such thing as no risk. Sometimes we just need to embrace volatility and anxiety now for wealth later on. Or take comfort in ‘guaranteed’ debt instruments now, and face destitution later on as rising living costs overwhelm a fixed income. Strong language, I know. But necessary to effectively get the point across. |

|

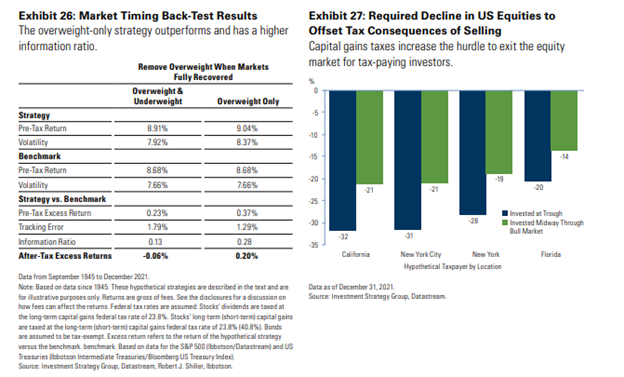

As stewards of your wealth – we are constantly looking out for compelling research to challenge our own views and present us with new ideas. In this year’s Goldman Sachs 2022 market outlook (link sourced below), they highlight the challenges involved with deviating from a strategic asset allocation. They simply compare two strategies: one in which an investor tactically goes underweight and/or overweight equities; the other in which the investor simply remains overweight equities the whole time. Perhaps unsurprisingly, the “overweight only” strategy wins over time. Furthermore, excessive trading when done in a vacuum can wreak havoc on client portfolios from a tax perspective, as the second chart shows. Especially in high tax-rate domiciles, where the potential cost of blindly raising capital is even higher: |

|

(Source: Goldman Sachs Outlook 2022, “Piloting Through” – Page 25) |

|

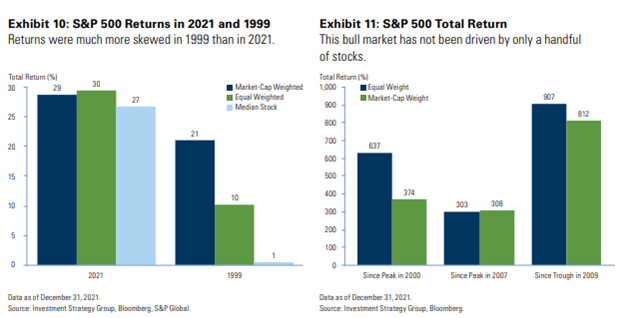

One of the most interesting aspects of this bull market has been the media narrative around “market concentration” in only a handful of companies. Goldman’s 2022 outlook disputes this assertion, and goes so far as to invalidate it. The graph below shows that while in 2021, an equal-weighted index of S&P 500 stocks outperformed its market-cap weighted counterpart narrowly, the second chart on the right shows much more powerfully that over the course of the entire bull market since 2009, Equal-weighting the S&P 500 actually delivered a 907% total return vs the 812% enjoyed by the market cap weighted counterpart. Talk about the benefits of staying fully invested and not just investing in a market-cap weighted index! Our team has been aware of this phenomenon for a long time, and thus our conviction in overweighting small and mid-cap stocks, which are persistently underweighted in the ETF world. |

|

(Source: Goldman Sachs 2022 Outlook: Piloting Through Page 21) |

|

Despite the Omicron variant, companies in the United States are enjoying record-high profits (even though the scare-tactics of the modern day media may have us feeling like the opposite is happening). Since corporate profits are often a harbinger of how the economy will go in the future, we find scant evidence of a recession in the near future; which is great news, because large market sell-offs normally go hand-in-hand with a recession. Improved supply and lower demand should take some pressure off the severe supply-chain pressures experienced in 2021. We believe the mid-cycle (economic expansion) environment should be generally constructive for asset markets in 2022, but markets will likely continue to be more volatile. Monetary policy risk will continue to be front and center, with the Fed facing a difficult balance of trying to address rising inflation expectations without overly tightening financial conditions. |

|

(Source: Goldman Sachs 2022 Outlook: Piloting Through page 19) |

|

Thank you for your trust,

-Your Marathon Team

|

|

Charlie G. Brown

Financial Advisor, Financial Services Representative

|

|

|

Charles G Brown IV | Financial Advisor | cgbrown@meetmarathon.com

Evan Shifley, CLU | Financial Advisor | eshifley@meetmarathon.com

Cooper Grady, CFP | Financial Planning Director | cgrady@meetmarathon.com

Brent Wood | Director of Operations | bwood@meetmarathon.com

Indrani Namilikonda | Client Services Coordinator | inamilikonda@meetmarathon.com

Allison Duquette | Administrative Assistant | aduquette@meetmarathon.com

|

|

REQUIRED DISCLOSURE:

Investment advisory services provided by NewEdge Advisors, LLC doing business as Marathon Financial Group, as a registered investment adviser. Securities offered through NewEdge Securities, Inc., Member FINRA/SIPC. NewEdge Advisors, LLC and NewEdge Securities, Inc. are wholly owned subsidiaries of NewEdge Capital Group, LLC.

The information contained in this email message is being transmitted to and is intended for the use of only the individual(s) to whom it is addressed. If the reader of this message is not the intended recipient, you are hereby advised that any dissemination, distribution or copying to this message is strictly prohibited. If you have received this message in error, please immediately delete.

|

Marathon Financial Group | 857-201-34320 | 131 Dartmouth St 3rd Floor Boston, MA 02116 | meetmarathon.com

|

|

|

|

|

|

|