Hello All-

I hope you’re enjoying summer and staying cool despite the stifling heat from which no region seems to be spared. I’m just returning from a trip to Italy and conditions were so uncomfortable that we decided to shift away from a lot of city sightseeing planned in advance, in favor of spots like Lake Como, where it seemed it would at least theoretically be easier to stay cool. We spent most of the time either in the lake or pool, and it was quite relaxing and beautiful. And the favorable (at least from a tourist’s perspective!) euro/dollar exchange rate made it a very economical trip compared to many other places we could’ve gone in the US that probably wouldn’t have been nearly this pretty (

photo here). The other guy in the photo is my new-ish significant other, Stephen, who recently moved to New England from New Orleans and will soon be practicing primary care at Southcoast Health in Dartmouth, MA. Special shout-out to our client and my dear friend Dr. Jonelle Raphael for helping Stephen land this new gig. Thanks Jonelle!

Speaking of client shout-outs, I also want to give special mention to Oz Mondejar, who just recently retired as Sr. Vice President of Mission & Advocacy at Mass General Brigham & Spaulding Rehabilitation Network. Oz is one of the most charismatic, inspiring people I know. He spent most of the last 2 decades in this role building community partnerships and designing diversity, equity and inclusion initiatives for MGB. Even though he’s retired now, Oz is still putting his gifts/talents to good work, as he sits on a number of non-profit boards, including Partners for Youth with Disabilities (PYD). In short, PYD invests in building the skills and abilities of young people with disabilities, and increase the inclusivity of workplaces, organizations, and communities. This spring, Oz introduced me to PYD and their important work, and invited me to join the planning committee for their big annual event/fundraiser. I joined and while party planning is not my forte, I found it very rewarding to meet and/or hear the stories of so many kids/young adults whose lives have been positively impacted by their work. This motivated me to pledge $5k to the organization on behalf of Marathon, and I also pulled out my ‘rolodex’ of professional partners and was able to help secure additional $5k fundraising from the following:

- SBLI- Savings Bank Life Insurance of Woburn, MA

- Green Oak Tax Services- JJ O’Connor CPA

- GradFin (Student Loan Refinance)

- Bob Doherty @ Burgin Platner Hurley (Auto/home insurance)

So thanks to Oz for connecting me to this wonderful organization, and for all of the work you continue to do on behalf of many important charities. And congrats on your retirement!

Before I get started with the content you’ve so patiently (and I’m SURE quite eagerly) been waiting for, I wanted to quickly mention that lately we have received a number of inquiries from clients asking if we would be willing to connect with a friend, family member, neighbor, or colleague to act as a sounding board or provide a second opinion, even if just on an informal basis given urgent concerns popping up these days. If you are approached by someone, or if you know of someone looking for a financial wellness check, or perhaps just a sympathetic ear, please let them know that we will always find the time to listen, and we’ll do our best to help.

Over the last few months, I’ve dedicated even more time than usual to consuming and digesting financial media, and I have a lot to say and articles to share on inflation, recession, etc. But first, I want to say this: like so many of you, I have spent much of 2022 thinking about how to keep myself centered in a world filled with so much uncertainty. Right now, no matter how intentional we may be, it is hard not to fall into bouts of anxiety and despondence as we read headlines, social media posts, etc. And as many of you know, I can be quite pessimistic when it comes to geopolitics—it’s really hard not to be when you’re paying attention. Regardless, as a student of the history of financial markets and macroeconomics, I remain steadfastly optimistic that the fundamentals will continue to prevail, and the stock market will recover recent losses and ultimately climb on to new highs. So, at the risk of sounding like a broken record, as your financial advisor, in times of volatility it is my principal duty to continuously remind you of a select few unwavering and timeless principles of our behavioral investment philosophy (i.e. the ‘big picture’) and away from (albeit perfectly human) negative emotions that lead to investing mistakes in these moments. In short, we don’t do Armageddon here. Dread is not an investment policy.

For our clients in or approaching retirement---I understand that there’s only so much that words/historical context, charts, and graphs can do to calm nerves right now, because we need these assets to cover your income needs, right here, right now. And creating a reliable income stream has become more challenging these days, given dismally low yields on bonds. But we have been carefully considering the inevitability of the current market environment since the moment you hired us, and rest assured that your portfolio has been constructed with all of that stress testing in mind, as well as an almost obsessive focus on income (e.g. stock dividends) to mitigate the extent to which we need to sell off principal to make sure you have what you need. Income is the ‘driver’ of our retirement plans.

So we’re now officially in a howling bear market. And with good reason. The level of near-term economic uncertainty seems astronomical. Both of the most feared outcomes are bad. Yet if we avoid one, we risk running smack into the other. Either (1) inflation continues to rage at unacceptably high levels, destroying the purchasing power of Americans’ trillions of dollars in retirement savings. Or (2) the Federal Reserve, scrambling belatedly to stamp out the inflationary fire, plunges the economy into recession.

This after 30 months of relentless economic, financial and political upheaval: a hundred-year global pandemic. A bitterly partisan presidential election which didn’t end on Election Day. Massive supply chain issues, including inexplicable shortages of that most basic building block of modernity, the semiconductor. A forty-year surge in gasoline, food, and industrial materials prices. War in Ukraine, concerning which the Russian dictator appeared to threaten the use of nuclear weapons. Interest rates spiking. Consumer confidence near all-time lows.

Never mind that, at its January 3 peak (4,797), the S&P 500 had gone up seven times from its March 2009 closing low (677) in the Global Financial Crisis. A septupling of mainstream equity values in just under 13 years represents one of the greatest market advances of all time. The average annual compound rate of growth during this run was 17.5%, versus the long-term average of 10.5%.

Yet all that seems to matter these days is that the market is down nearly a quarter from its most recent peak, with no end in sight. That’s what happens to people in a bear market: they lose whatever long-term perspective they might briefly have had. There’s a potential remedy for this loss of perspective, and it begins with remembering that what we’re supposed to be investing for is not the near-term prices of stocks, but the long-term values of companies. This is the first step in escaping the maelstrom of hysterical noise that threatens to engulf us in sheer terror at times like this. Once more, with feeling: not stocks. Companies.

The second step is to turn off the television, log out of your market news feed, and make the time to look seriously at the list of the companies in the S&P 500, which is where a majority of your capital is invested. You will probably recognize most if not quite all of the names. And you will begin to remember what you always knew: that these companies are among the largest, most strongly financed, best managed and most innovative businesses in the world.

Many are iconic brands whose products and/or services you and your family use regularly—some as often as every day. As an exercise, put a check mark next to each of these names. As you do, ask yourself if you’re planning to stop patronizing these companies. When for the most part you conclude that you’re not—and suspect that most other people won’t either—you’ll have taken the third step.

Having done so, you’re now prepared to ask yourself the one absolutely critical question, the answer to which (a) should be pretty obvious, and (b) may just be enough to get you through this ugly time: “Do I believe that these iconic companies have—just since the turn of the year—permanently lost a quarter of their enduring value as superior businesses?” If you don’t—and I certainly don’t—there will be your answer. And if, a couple of months from now or whenever, the question has become “Have they lost a third of their enduring value,” I suspect your “no” will be that much stronger. When it is, you’ll be well on your way to a lifetime of successful investing. Because you’ll have fully realized that the near-term prices of stocks and the long-term value of companies are two entirely different—and sometimes downright contradictory—things.

Peter Lynch said it best: “The real key to making money in stocks is not to get scared out of them.”

So, before I get into inflation and recession, let me just quickly reiterate a few important bullet points to try to keep in mind as this volatility persists:

- Over these last three calendar years (2019-2021), the S&P 500 Index compounded at 24% per year. The average annual return is 10%. It’s now fairly evident that some part of the extraordinary accretion in equity values over these three years was due to excessive monetary stimulation by the Fed. And to that extent, we are having to give some of that gain back, at least temporarily. Monetary tightening by the Fed is an important step to curbing inflation, and while this ‘cure’ will hurt for a bit, it is not more painful than the disease (of inflation).

- We act continuously on our financial and investment plan; we do not react to current events, no matter how distressing they may be. However, contrary to what we often hear in these volatile moments, we shouldn’t simply shield our eyes and stay invested in all of the same ‘stuff’ we owned before. Outlook for various regions and sectors has now materially changed, and market environments like this one present many meaningful opportunities to add value by swapping out some companies and/or asset classes in pursuit of discounted companies/asset classes that now have much more attractive valuations. Over the last 7 months, we have made a number of trades, and have been working hard to identify these opportunities and reposition portfolios for optimal upside potential when the market rebounds.

- When we select investments on your behalf, we are not speculating. We are buying high quality, profitable companies with durable competitive advantages, with a lot of diversification across sectors. And we are deliberately screening out weaker companies that are signaling a possible long-term decline in earnings and momentum. The goal is to own companies that hold up better in more challenging environments because they are profitable and have strong balance sheets. These companies have demonstrated the ability to increase earnings and dividends over time, thus supporting increases in their value.

- At the end of the day, the equity market is going to go down as much and as long as it needs to. The longer and deeper it does go down, the more dynamic the ensuing advance will be. This is virtually a law of nature. This is our logical progression:

- The economy cannot be consistently forecast.

- The equity market cannot be consistently timed.

- Therefore, the only way to be reasonably sure of capturing (and compounding) the permanent return of equities is to ride out their sometimes significant but always temporary declines

OK, so now let’s talk about recession.

To many investors, this week’s GDP report (Thursday 7/28) is more important than usual. The reason is that real GDP declined in the first quarter and might have declined again in Q2. If so, this could mean two straight quarters of negative growth, which is the rule of thumb definition many use for a recession.

We think investors are paying too much attention to the GDP numbers; the US is not in a recession, at least not yet. Industrial production rose at a 4.8% annual rate in the first quarter and at a 6.2% rate in Q2. Unemployment is lower now than at the end of 2021. Payrolls grew at a monthly rate of 539,000 in the first quarter and 375,000 in Q2. If we were already in a recession, none of this would have happened. That’s why the National Bureau of Economic Research (NEBR), the official arbiter of recessions, uses a wide range of data from consumption to industrial production when assessing whether the economy is shrinking.

The NEBR is a private non-partisan, eight-member group of macroeconomists, and their analysis has occasionally led them to declare that the economy is in recession even when GDP is growing. America managed to avoid two consecutive negative quarters of growth in 2001, but NBER still deemed it to be a recession. What makes the present moment so unusual is that the NBER may, for the first time, come to the opposite conclusion: that the economy has avoided a recession despite consistently negative growth.

Let’s take a closer look at the variables used to calculate GDP:

Consumption: “Real” (inflation-adjusted) retail sales outside the auto sector grew at a 2.2% annual rate, and it looks like real services spending should be up at a solid pace, as well. However, car and light truck sales fell at a 19.7% rate. Putting it all together, its estimated that real consumer spending on goods and services, combined, increased at a modest 1.2% rate, adding 0.8 points to the real GDP growth rate (1.2 times the consumption share of GDP, which is 68%, equals 0.8).

Business Investment: Current estimates point to a 5.5% annual growth rate for business equipment investment, a 7.5% gain in intellectual property, but a 4.0% decline in commercial construction. Combined, business investment looks like it grew at a 4.4% rate, which would add 0.6 points to real GDP growth. (4.4 times the 14% business investment share of GDP equals 0.6).

Home Building: Residential construction looks like it contracted at a 4.0% annual rate. Mortgage rates should eventually become a headwind, but, for now, it looks like an increase in spending on construction was more than accounted for by inflation in construction costs. A decline at a 4.0% rate would subtract 0.2 points from real GDP growth. (-4.0 times the 5% residential construction share of GDP equals -0.2).

Government: Only direct government purchases of goods and services (and not transfer payments like unemployment insurance) count when calculating GDP. We estimate these purchases – which represents a 17% share of GDP – were roughly unchanged, which means zero effect on real GDP.

Trade: Exports have surged through May while imports, after spiking late in the first quarter, have remained roughly flat so far in Q2. That means a smaller trade deficit. At present, we’re projecting net exports will add 1.0 point to real GDP growth, although a report on the trade deficit in June, which arrives on July 27, may alter that forecast.

Inventories: Inventories look like they grew at a slower pace in the second quarter than they did in Q1, suggesting a drag of about 1.7 points on the growth rate of real GDP. However, just like with trade, a report out July 27 may alter this forecast.

Add this all up, and we’d be looking at a 0.5% annual real GDP growth for the second quarter. In addition, it’s important to recognize that once a year the government goes back and revises all the GDP data for the past several years. That happens in July, including with the report arriving this Thursday. Given the strength in jobs and industrial production, it wouldn’t surprise us at all if Q1 is eventually revised positive.

However, with inflation so persistent (and now at a 40-year high), the Fed has embarked on a course of monetary tightening that seems destined to be its sharpest since the early 1980s. Increases in interest rates do not always precede recessions. But it will be at least a small miracle if America can absorb tightening of this magnitude without suffering a pronounced rise in unemployment. While the war in Eastern Europe and supply chain woes of various kinds have exacerbated inflation, in our judgement, they’re irritants. At the end of the day, it’s monetary policy (seasoned as well with a bit too much fiscal stimulus) that got us into this mess, and monetary policy must now get us out. In short: The Fed created far too much money (via ultra low rates) and then left it sloshing around out there far too long. The Fed is now moving belatedly to sop up that excess liquidity by raising interest rates and shrinking its balance sheet, and the fear now is, of course, that they will overtighten and put the economy into recession in order to sufficiently tame prices.

While there may not be many positive catalysts to drive the market higher over the short-term- especially while several more interest rate hikes appear likely down the road—there does appear to be some emerging good news: Inflation may be peaking. If that is indeed the case, it might alleviate some of the pressure pushing the Fed to aggressively raise rates.

Despite the June CPI report showing inflation rose 9.1% year over year, most commodity prices have started to put the brakes on recently. The Bloomberg Commodities Index—which tracks more than 20 commodity futures including energy, metals, and livestock—has declined 19% since this year’s most recent high reached on June 9th (Fidelity). Take oil, for example. West Texas Intermediate Crude (benchmark oil price in North America) is trading at just under $97 barrel, as of early July, down from the near-term peak of $120 per barrel in early June. Among food commodities, wheat prices are near $8 per bushel, down from $13 per bushel in mid-May. While those prices are still quite high relative to pre-supply chain problems from just a few years ago, they are down substantially from post-Ukraine invasion levels—providing some measure of relief to many consumers around the world.

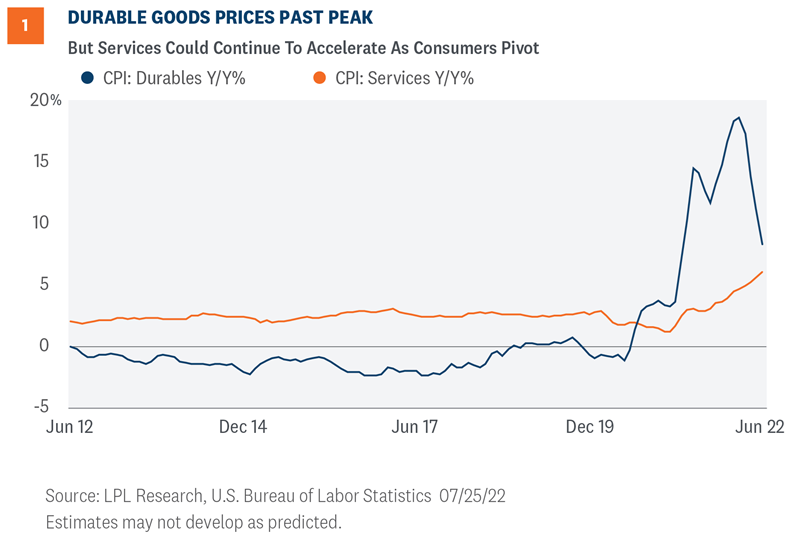

Beyond core commodities, I should note that inflationary reports are highly nuanced at the moment. Durable goods prices are clearly past peak but in contrast, services inflation is not slowing down. As consumers pivot to more services spending, travel-related consumer prices will likely take a longer time to moderate relative to goods prices.