|

This fall, the MFG team is continuing to work hard on enhancements to the client experience, which we will be rolling out on a personalized basis in these final few months of the year. I have also been working on my video content production skill set, so that we can more proactively create and distribute content in which we share anticipated and/or common questions and answer them in detail, for everyone. We’ll be building a content ‘library’ for clients and will also share these videos as we produce them. You’ll probably start to see more of these roll out closer to the end of the year, as I am still very much a ‘student’ in this area and effectively ‘building the plane as it’s in flight’! In any case, I know my first few of these aren’t going to be ‘great’ in terms of production quality (although content should be strong!) so bear with me—they’ll get better and we’ll just have to take a ‘trial and error’ approach in terms of finding the right assistance with professional editing. Ultimately, the goal is to create a vast library of video Q&A’s with supporting visuals (charts, graphs, etc.) built in, and also just to get so good at making these that we can share/film a live answer to most questions within hours of being asked, to save you time. Stay tuned!

Even though we’re focusing on financial market content within the weekly updates (and in year-end deliverables going out by 11/10), I’ll talk about this briefly before getting more into financial planning strategies and ‘to-do list’ reminders. For those interested, I’ll note that John will be getting deeper into the state of the bond market, and its current opportunities and risks, in this week’s market-focused distribution.

As we enter what we hope will be the final stage of the Fed’s monetary tightening program, multiple economic and market challenges face the Federal Open Market Committee (FOMC), investors, households, and leaders in Washington DC. These challenges run the gamut from high oil prices to the threat of a government shutdown. Consumer confidence is weakening and the Biden administration’s economic approval rating is tanking. What could lie ahead?

The price of a barrel of crude has spiked to over $90/bbl, up from $70/bbl as recently as July. The move coincided with simultaneous production cutbacks by Saudi Arabia and Russia amounting to nearly one million barrels/day. Prices at the gas pump are up to $3.82/gallon, up from $3.52/gallon at the beginning of the summer.

Adding to the economic woes are the writers, actors, and autoworkers strikes. It appears that the 148-day Writers Guild of America walkout could be nearing a conclusion. However, the more than 4,000 days of idleness due to work stoppages as of the end of August dwarfed all strike activity over the last decade. This suggests labor costs will rise and, in today’s tight market, margins could compress at a time when earnings among S&P 500 companies are expected to be flat for the year.

Meanwhile, if Congress doesn’t pass a continuing resolution over the next few days the government will be forced to shut down. While policymakers attempt to negotiate a higher debt ceiling, few in Washington are focused on our immediate budget challenges. The Treasury faces $2.6 trillion in bond maturities next year with existing bonds carrying a two percent coupon, on average. That suggests interest expenses, as part of the federal budget, will likely increase by about $100 billion annually as those maturing bonds are rolled over and new bonds are issued. Current trends indicate interest expense will surpass defense spending to become the largest discretionary spending item by the end of 2025.

Another factor upsetting the equity apple cart is higher Treasury rates. The benchmark 10-year Treasury yield has been climbing steadily since the summer, pushing the yield to over 4.5 per cent, its highest reading since 2007, long before the Fed embarked on its quantitative easing program. The move was fueled by rising real rates, the 10-year Treasury yield relative to inflation expectations. Perhaps bond investors are beginning to impose a “distrust premium” on the federal government. The impending government shutdown, underscoring rating agency Fitch’s concern that fiscal intransigence poses a credit risk to our nation’s debt worthy of a downgrade. Unfortunately, higher real rates filter through to all borrowers, increasing the cost of financing businesses, housing and automobiles, among other things.

For the most part, higher energy and interest costs are helping do the Fed’s work for it, suggesting that rising energy and interest costs will serve as a tax, funneling resources away from discretionary spending. The recent deterioration in consumer confidence exemplifies that trend. That also mirrors a significant decline in President Biden’s approval rating. According to a recent ABC News/Washington Post poll, only 30% of those surveyed approve of his job on the economy, with 64% disapproving. While the Fed’s game plan may be cloudy as monetary policymakers weigh the second-order impacts of recent trends, President Biden’s game plan should be clear: he needs to offer leadership on the federal budget and spending before the bond market does.

In short, the fiscal situation of the United States is a slow-motion train wreck. If and how this situation will be resolved is not possible to predict. The outcome depends to a great extent on our finding the political will to enact the kind of pro-growth policies which have propelled us out of stagnation in the past. The reality is that things may have to get worse for that to happen.

So, as we speak with clients who presumably can only become progressively more alarmed by these trends, we won’t sugar coat it. It is a developing situation, not yet of crisis proportions but continuing to go south. I know I’m not going to train resilient investors with only happy talk.

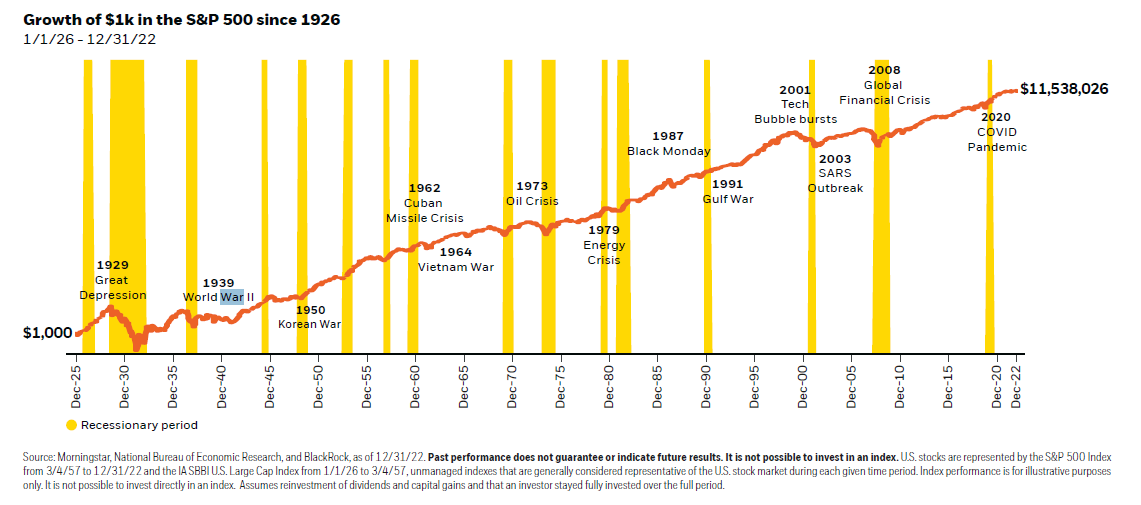

First I’ll say that I am in no position to analyze the situation intellectually nor to predict the outcome here. Instead, I’ll continue to drive home relentlessly the fact that we are not investing in the macroeconomy, nor in the ‘stock market’. We are patient, disciplined long-term owners of consistently successful profit-seeking, capital preserving companies. And we know from long-term experience that those companies—innovating ceaselessly—have prospered mightily through every kind of economic, financial, political and geopolitical nightmare. (The S&P 500 has halved three times in the last 50 years. The Index stands today 35 times higher than it was at the beginning of that gauntlet because that’s how much the earnings have grown.)

I’ll reiterate that the economy is always unknowable. It can never be reliably timed. The only way one has ever been sure to capture equities’ superb permanent returns is to ride out their frequent, sometimes significant but always temporary declines. In a market that’s been compounding at nearly seven percent net of inflation for a century and more, wealth must follow.

Macroeconomic uncertainty, alone, should not be a reason to get out of the market. Take a look at this article/chart from the Visual Capitalist which shows the risk of trying to time the market. By simply missing out on the 10 best days, an investor could lose the majority of their overall return. Really helpful read for anyone even contemplating an exit (or holding onto excessive amounts of cash due to macroeconomic uncertainty and ‘wanting to get the timing right’).

As to the question of whether there should continue to be an emphasis on US businesses in portfolios, this blog post “Is this a great country of what?” tells a good visual story. As does this article ‘The Wonders of Economic Growth’.

For further positive perspective for the long-term outlook, check out ‘The Doomslayer’ a weekly positive news roundup of humanprogress.org. It’s chock full of hopeful science, health, and environmental news and commentary cannot be found in any other single place.

|