|

Hello All-

As investors, it is important to distinguish ourselves from forecasters. We strive to focus on the bigger picture, preparing our portfolios based on what we know, rather than trying to predict what we don’t. Last year was a textbook example of why we do not allow ourselves to be scared out of the market and instead remain invested during downturns.

On one hand, the answer to “where will the market go and when?” is fleeting and unattainable; but, at the same time, the answer is right in front of us. History tells us that over meaningful periods of time, markets appreciate. Strategies dependent on trying to time the best possible entry and exit points based on the myriad of factors at play are plainly unsuccessful.

The S&P 500 gained 24% in 2023 against the backdrop of the most aggressive Fed rate hike cycle in history, a regional bank crisis, persistently sticky inflation, elevated treasury rates, on-going war in Ukraine, a new war between Israel and Hamas, an inverted yield curve, and a slew of leading economic indicators pointing towards a recession – just to name a few.

This time last year, the market resembled something decidedly different than it does now and many investors remained hesitant or were scared out of the market, only to miss out on the gains that followed and were left chasing the market.

As we take a brief look at the investment themes impacting markets, it is always through the lens of the long-term investor as we make observations to help better position our portfolios.

Q4 Takeaways

We ended the previous quarter in stellar fashion as Fed Chair Powell began to look suspiciously like Santa Claus – gifting the market surprisingly dovish commentary during the last FOMC press conference for the year. The market interpreted Powell’s words as a victory speech on inflation, rather than anything resembling a pushback against a potentially overzealous market – a drastic change from his commentary just a month earlier on November 1, when he stated the Fed was not even thinking about cutting rates. The market began the year pricing in six rate cuts for 2024, potentially beginning as early as March.

Mega-cap equities continued their extraordinary dominance, responsible for most of the market’s return. Still, we saw the broader market begin to catch up, as investors found areas of the market offering additional value – particularly in more defensive sectors such as utilities, staples, and healthcare.

On the fixed income front, we saw elevated treasury yields in response to higher rates continuing to pressure bonds and equities alike. With the Fed’s rate hike cycle seemingly ending and highly anticipated rate cuts on the horizon, we have seen some relief as long-dated treasury yields declined from their highs earlier in the year. While we are primarily equity investors, we pay particular attention to yields. Our fixed income strategy balances the benefits of both shorter-duration and longer-duration bonds.

Shorter-duration provides attractive income opportunities as rates remain elevated, with longer-duration bonds positioned to benefit as rates steadily fall – providing capital appreciation.

Economy

On the economic front, inflation and interest rates continue to be the dominant story. Throughout 2023, the resiliency of the consumer and labor markets has played a key role in supporting equity markets as their strength has helped offset higher rates and recessionary fears. Unemployment remains historically low with consumers still spending – partly due to savings built up during the Pandemic. While inflation has declined significantly, core inflation (ex. Food and energy) remains stubbornly high, nearly double the Fed’s 2% target, which will impact rate cuts decisions and challenge the market’s expectations into the new year.

Earnings

A majority of companies have reported earnings for the fourth quarter with most reporting positive surprises. Heading into Q4 earnings season, we had the case of valuations being relatively high and the earnings bar being relatively low. Throughout 2023, resilient earnings have been an important catalyst for equities, but the bar has been relatively low throughout. The rally in equities has largely been due to multiple expansion (P/E) and investor sentiment. In the fourth quarter especially, Prices (P) increased while earnings (E) estimates were lowered.

The market is forward looking – so while it is ideal for companies to have a successful fourth quarter, the key focus for us will center around management’s guidance for the upcoming quarters in 2024. Earnings will continue to be a critical consideration as the broader macro environment will bring more challenges to the soft-landing narrative bolstering equities.

2024 Outlook

As it stands, the market presents two fundamental narratives. The first being that the Fed will be successful in taming inflation and balancing unemployment without pushing the rest of the economy into a recession. The second being the opposite – with the lag effects (and other quantitative tightening efforts) from the most aggressive rate hiking cycle in history causing slower than expected growth and pushing the economy into a recession – which would impact earnings growth and thus equities. For a majority of 2023, the market has assumed the former, which has been helped by enthusiasm for generative AI and the resiliency of mega-cap stocks buoying the markets.

The takeaway is that equity markets seem to be set on the notion that the rate hike cycle is over, with rate cuts firmly priced in, along with the belief for a soft landing. What is has not priced in, is if economic growth slows more than expected or if the Fed decides to keep rates higher-for-longer for whatever reason, such as persistently sticky inflation. Challenges to equities going forward will center on economic data – inflation and unemployment – and monetary policy risk. The market is based on expectations, so any data impacting the market’s expectation for six rate cuts will likely cause investors to reconsider near-term equity valuations. We have already seen it this quarter, as hotter than expected inflation data has given the market cause to dial back its original rate cut expectations.

With all of this in mind, we continue to favor domestic growth as an area of focus. While pockets of the market show value, such as in small-cap and international, we are not entirely out of the woods yet in terms of the Fed and global growth slowdown – particularly due to sticky inflation and China’s delayed economic recovery. While we continue to maintain meaningful allocations to mega-cap, we will also be looking for broader opportunities within technology, discretionary, and healthcare sectors with companies that are well-positioned to benefit from continued advancements in generative AI, e-commerce, and general trends towards digitization. Particular industries of interest include semiconductors, services, and medical devices.

Interesting Charts

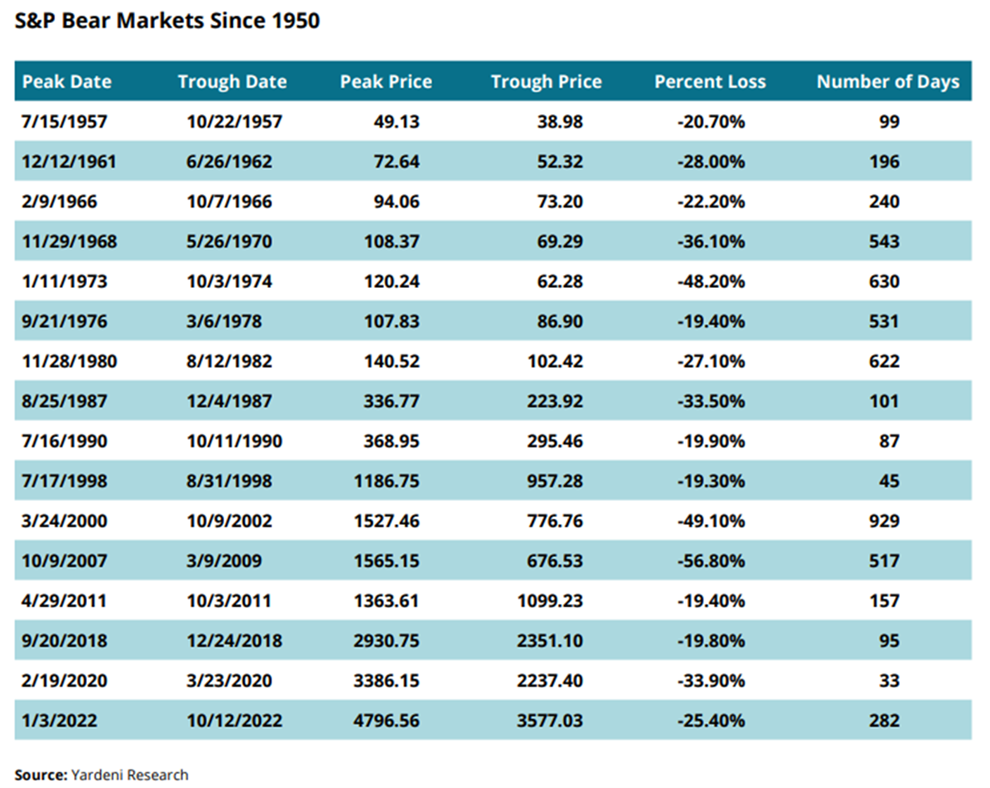

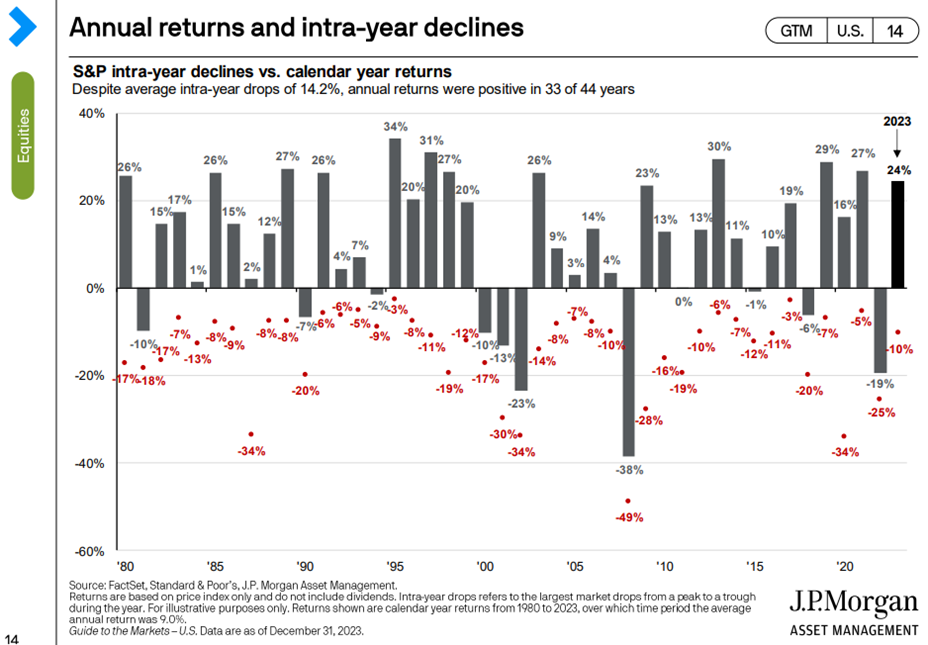

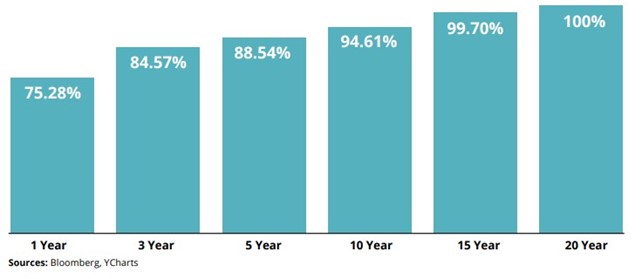

A bear market is convincingly over after the market has reached new highs. As I write this, the market has certainly reached a new high ground – eclipsing the recent bear market in 2022. Despite how terrifying it can feel at the time, the market has always recovered from its relatively infrequent declines. The chart below highlights this idea.

Throughout history, the market has often experienced downturns – only to resume its steadfast advance shortly after. In the multiple decades shown below, the market has declined 20% or more in only 11 instances, with each lasting a relatively short period of time before recovering.

My objective in sharing this with you periodically is simply to share an accurate picture of just how frequently you can expect your faith, patience and discipline to be tested as an investor seeking the long-term permanent advance of the stock market.

|