Hello All-

Wow. It’s June. How did that happen? I hope you had a wonderful Memorial Day Weekend. This week we honor and remember all United States military members who have died in service of our country, protecting our freedoms. We salute our clients and their loved ones who are veterans or active military members. Thank you for your brave service.

I’m going to begin by sharing five questions we fielded in the past couple of weeks, and answers. After that, I’ll summarize our current market outlook in bullet point form, share some helpful ‘big picture’ thoughts on how to think about and better come to terms with volatility and overcome emotions/human nature in our quest to be successful long-term investors. Then, I’ll conclude by sharing a number of helpful articles I’ve compiled over the past month+.

|

|

Q. What’s your take on the impact of the debt ceiling drama?

A. By now, we all know the US Treasury is about to run out of ways to pay its bills, but we have seen this movie many times before. While, theoretically, there has been a threat of default, we certainly don’t recommend planning our lives around it. The script is very predictable: political posturing and grandstanding will go on until the 11th hour, and then a deal is hastily put together to avoid a default. And that’s exactly what has happened.

- While no common citizen wants to be in this situation, it is the type of situation politicians clamor for and fawn over, because each side has the ability to project strength while positioning to their voting blocks that they are “fighting hard to get their way.”

- In our view, politicians hijacking the credit rating of the United States is highly problematic and could have real consequences. Fitch, one of the major credit rating agencies, has put the US credit AAA rating “on watch,” or at risk of a downgrade.

- Ultimately, while we do not assign a high probability to a default, the consequences of one could spark stock market volatility in the short run. We believe the well-diversified mix of stocks we own provide the ballast that is needed to buoy against potential market turbulence.

Q. Interest rates on auto loans, etc. are higher now-so would it make sense that I should redirect the cash I’m otherwise putting into the market, toward paying this debt down faster?

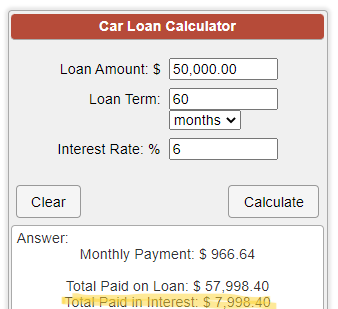

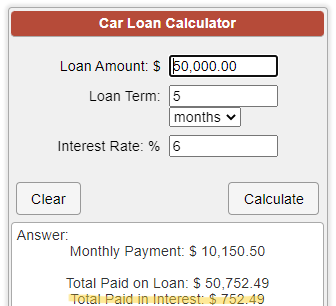

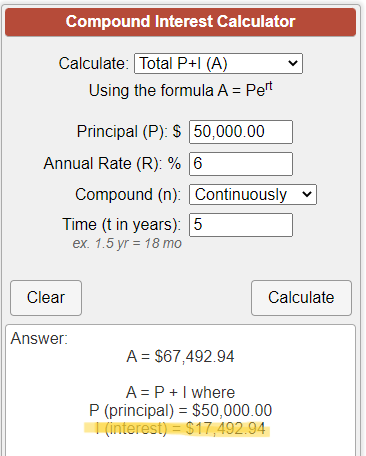

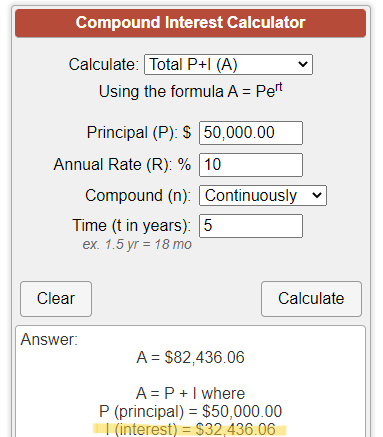

A. Short answer—in most cases, no. Especially if you’re still accumulating assets and several years away from retirement, and/or you can otherwise afford the monthly payment from your ongoing cashflow. Because of a beautiful thing called compound interest, dollars invested today/earlier on can have an exponential impact on asset growth over time. Because of the ‘concentrated leadership’ in the stock market this year (most gains being driven by ~20 companies), most of the stock market is still ‘on sale’ right now, so that’s an important factor (investing now could mean you get better than average returns—and the average annual return on the S&P 500 is 10%, for example). I ran some calculations below, based on a scenario in which a client is saving/investing $10k/month in their brokerage account, and wondering if they should, for the next 5 months, take that same $10k/month and pay down their $50k auto loan.

- Calculation #1 shows how much interest is paid on a car loan of $50,000 @ 6% interest, for 60 months (5 years). Total interest paid ends up ~$7,998.40 over life of the loan.

- Calculation #2 shows how much interest is paid if they pay off the $50k loan @ $10k/month for the next 5 months. The amount of interest paid is obviously significantly lower ($752.49 vs. $7,998.40), so the question is clearly quite logical if we’re just looking at the interest saved.

- Calculation #3, however, shows how much that $50,000 would have earned over the next 5 years if we had otherwise invested and got an average annual return of 6%. Interest earned is $17,492.94.

- Calculation #4 shows how much that $50,000 would have earned over the next 5 years if we had otherwise invested and got an average annual return of 10%. Interest earned is $32,436.06

- Key points in closing:

- Compound interest via investing usually wins out, especially as we consider the fact that amount of loan interest paid on the loan actually decreases each year, as the balance amortizes. Whereas, as you invest, the balance grows/compounds each year, building off prior year’s growth.

- I did the math, and you would only need to get an average annual return of 2.97% on investments to beat interest paid on this loan @ 6%, over the 5 year period.

- I did some additional math, and if we let this $50k ‘run’ (compound) for 20 years @ average annual return of 6%, interest earned over that time period is $116,005.85. To put it simply, there is a meaningful ‘opportunity cost’ in terms of long-term compound interest ‘missed out on’ by accelerating loan repayment versus investing.

|

|

Q. Yields/interest rates on bond investments are higher these days—should I be buying more bonds instead of stocks? Similarly, should I be holding more cash?

A: While bonds certainly play an important role as a ballast for any plan that requires current income and/or near-term liquidity, stocks are really our only hope as we seek to create an income stream we can’t outlive. I’ll first say as a disclaimer that stocks are too volatile over short periods, therefore you must only invest money in stocks that you won’t need for at least 5 years, and that is the approach we take when advising on how to weight stocks versus bonds for retirees and near-retirees. But 100 years of history have shown us that it has been far more profitable to be an ‘owner’ (of stocks) than a ‘loaner’ (when you invest in bonds, you lend money to a company or government). As a loaner, you get a fixed or floatable interest and/or your capital gets appreciated by a little if kept until maturity. Over the last 100 years, the real returns (net of inflation) to stock owners have been upwards of 3x what the loaner (bond investor) got. Lending money has limited upside, owning business has unlimited upside via dividends and appreciation of the business/stock value over time, but you have to accept the idea of unknowability of the future, and be very well diversified (as of course not all businesses ultimately succeed). People tend to overestimate the long-term risk of owning stocks and underestimate the long-term risk of NOT owning stocks. In our opinion, the greatest long-term financial risk we all face isn’t loss of principal, but rather, erosion of purchasing power (via inflation). Right now, for example, we can go out and buy bonds in the 5-7%+ realm, which initially seems like an attractive and more reliable alternative to stock investing, but what we need to keep in mind is that the reason we can get these higher rates on bonds is because the Fed is still battling inflation, which is @ 5% as of this writing. We may be able to lock in these rates for a while, and with any luck, inflation will continue to decline and make these rates more meaningful, but the reality is that eventually rates will fall and the real yields on bonds will struggle to even keep pace with the inflation rate. Similarly, with ‘high yield’ online savings banks, we have gotten so accustomed to near-zero rates for so long, that 4.5% is tantalizing—but due to the inflation rate (@ 5%), the real return is still negative. And basically the moment rates decline, so does the interest rate/yield you earn on your money in these types of accounts. Bottom line---we need to be very thoughtful about not holding too much cash or fixed income, too soon in retirement because this will ultimately impact portfolio longevity. And deciding to own more stocks doesn’t necessarily mean we’re looking to heavily pursue ‘aggressive’ growth (which can be extremely volatile). In fact, for retirees we LOVE what some might consider more ‘boring’ dividend-paying value stocks, because they tend to produce a reliable income stream, appreciate meaningfully, and in times of uncertainty, they can often be less volatile (2022 as example). And we can also strategically write covered calls on these stocks to generate additional portfolio income, at the right moments.

Q. How are you guys thinking about and to what extent are portfolios exposed to AI (Artificial Intelligence) opportunities?\

A. While our portfolios are customized to fit our clients risk tolerance and time horizon (and other individual preferences to exclude/include certain industries, sectors, etc.), you may not see all of these names in your specific portfolio, but here’s an outline of some of the stocks we have selected that are both direct and indirect beneficiaries to the artificial intelligence ‘wave’ that has been ‘brewing out at sea’ and is now landing on beaches across every industry.

- Nvidia is the most straightforward expression of AI, as they create the most advance A.I. chips in the world, from advanced autonomous-driving vehicles (think Tesla), to supercomputers powering all sorts of industries.

- AMD is another direct play on artificial intelligence.

- Microsoft, which is one of the largest holdings for many clients, will be a direct beneficiary of A.I. Through their purchase of ChatGPT, they will monetize A.I. through subscription fees charged to ChaptGPT4 customers, but they will also benefit indirectly as they have incorporated ChatGPT into their Edge Browser functionality, making the web browser a smarter version of Google.

- Google, itself, just launched an A.I. based search engine, and has been one of the most active investors and inventors in the A.I. space for many years.

- Amazon has been an early adopter of natural language processing, a type of A.I. which understands human speech and can respond to questions. Its usage of this technology via its Alexa interface it truly remarkable to witness, and has hundreds of business applications and use cases, such as making the AmazonPrime membership more useful to customers.

- Tesla also utilizes A.I. through its self-driving functionality (in which they have a very large lead over their competitors.)

- Taiwan Semiconductor Manufacturing manufactures the high end A.I. chips that are designed by the likes of AMD and Nvidia.

- A list of other companies many of our clients own, which either tangentially touch or are directly related to A.I., includes but is not limited to: Onto Innovation, Vishay Intertechnology, Intuit, Synopsis, Photronics, Rambus.

In short, we think A.I. could be one of the most influential innovations since the internet or the iPhone, and we will continue to look for opportunities as it develops.

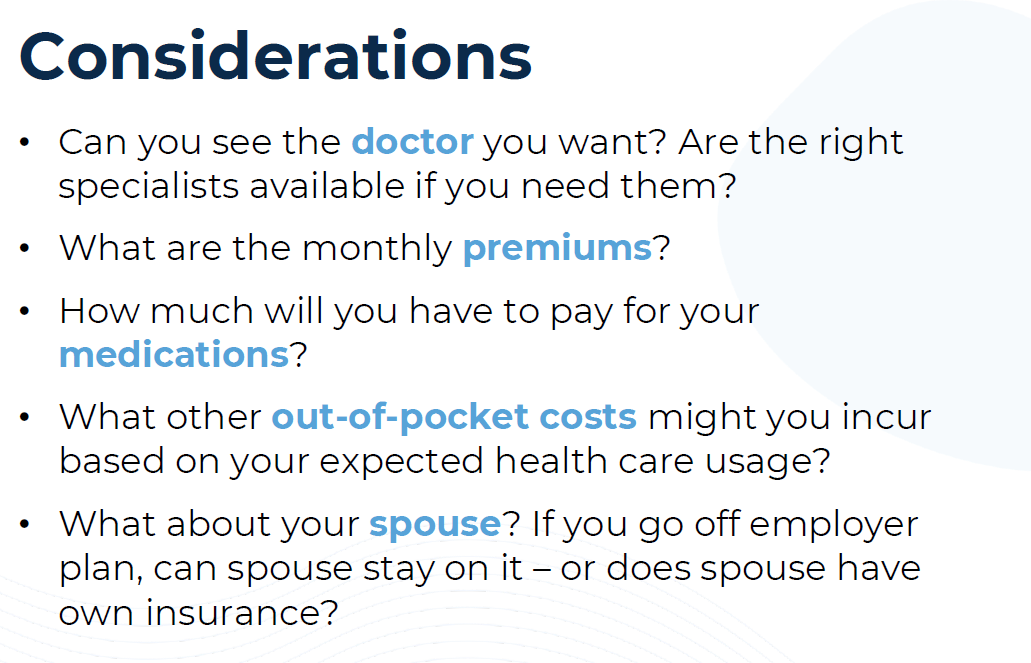

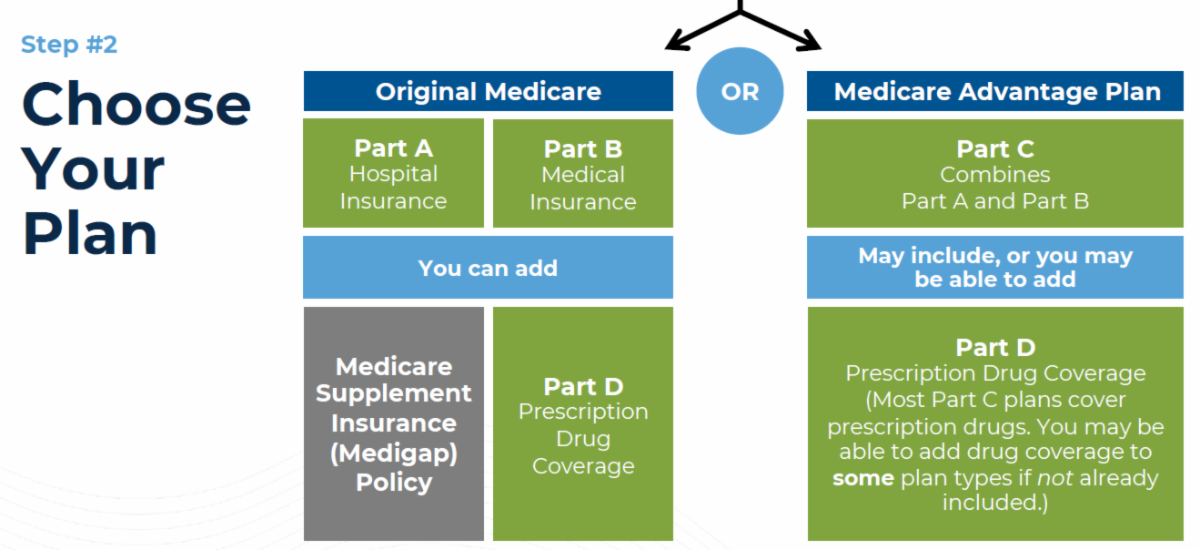

Q. I’m turning 65 and/or planning on retiring soon. What are the key considerations around Medicare?

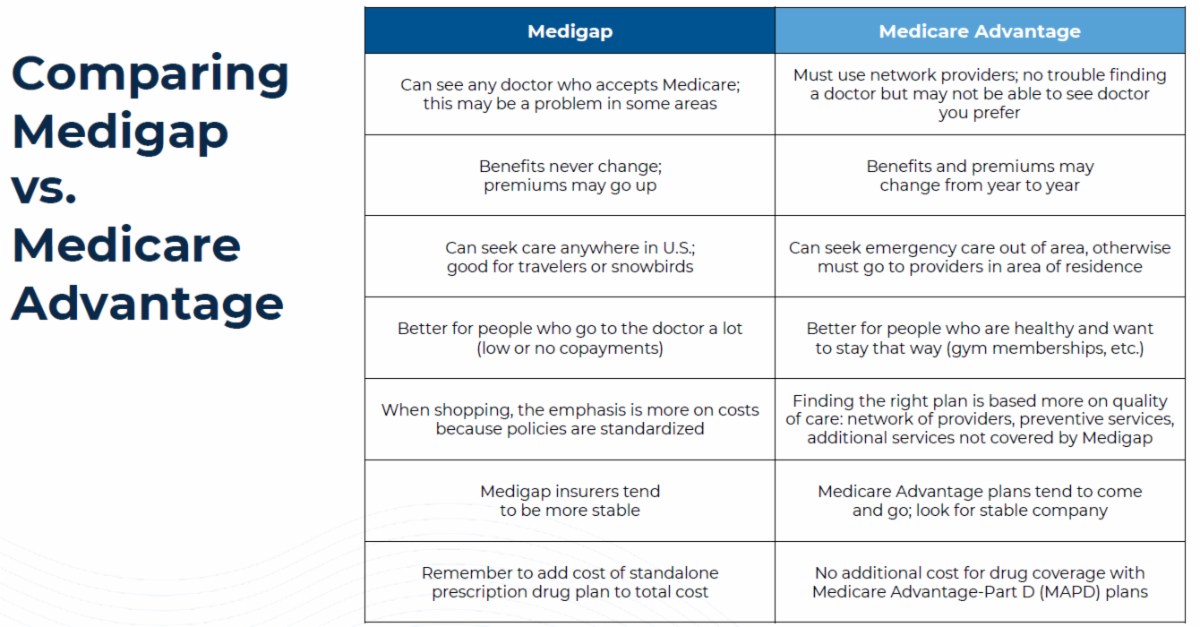

A. First, some quick basic points. You will absolutely need supplemental insurance to go with Medicare. The choice is between 1) original Medicare + Medigap + Part D plan, and 2) Medicare Advantage. You should shop supplemental insurance 5 months before enrolling in Medicare, and we can refer you to a licensed agent or State Health Insurance Program (SHIP). Some other helpful websites are BOOMERBENEFITS.COM & MEDICARE.GOV/FIND-A-PLAN. If you do not buy a Medigap policy within 6 months of enrolling in Part B (guaranteed issue period), you may be denied a policy based on health status in the future (although, some states, like MA, have an override). You can always get a Medicare Advantage plan, but Medigap tends to be more stable (benefits stay the same from year-to-year). |

|

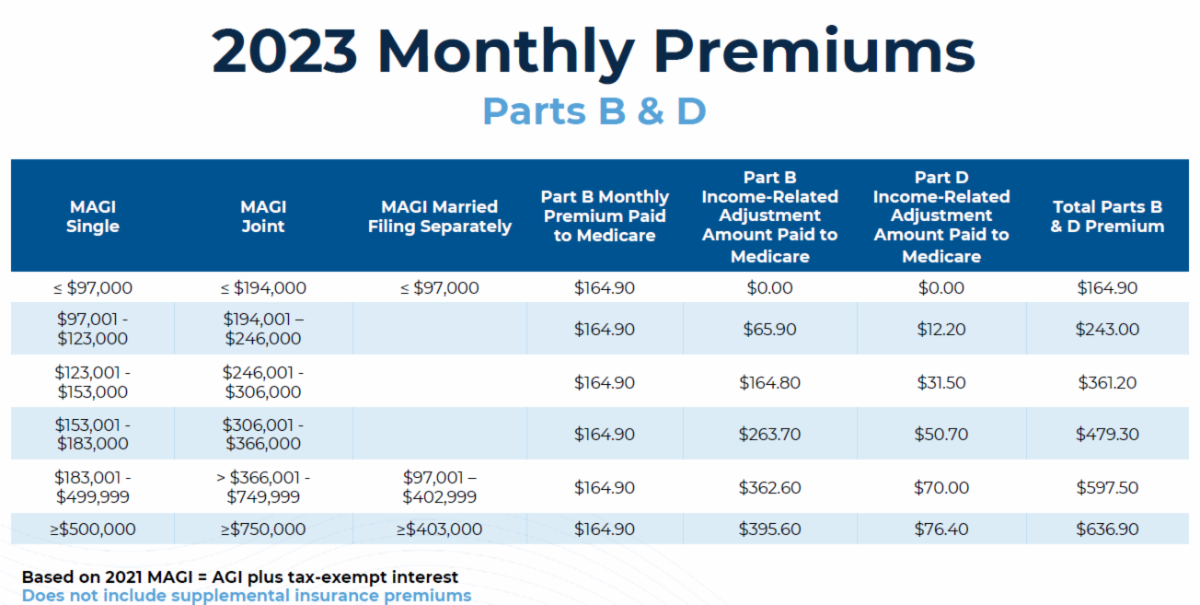

In the early years of being enrolled in Medicare, it might cost more due to the Income-Related Monthly Adjustment Amount (IRMAA), as the monthly payment for each year is calculated by your income from the two years prior, which can often be at or near peak as they reach the ‘home stretch’ before retiring. However, once retired, you can appeal the IRMAA. To do so, wait until you get the Medicare premium notice. Then use Form SSA-44, and show income for this year and next year due to life changing event (which includes simply reducing or stopping work). Chart below shows premiums—ex. If you’re married and earned $375k in 2021, but then retire in 2023, your total premiums would be $597.50/month/spouse. Whereas, if your income needs are lower in retirement, and AGI is only, say, $175k/year, you could appeal IRMAA and potentially get premiums reduced to $164.90/month/spouse.

|

|

Drug plans and Medicare Advantage plans change every year. Review during annual enrollment period, Oct. 15-Dec. 7. At that time:

- Check for higher premiums, reduced benefits, changes in provider network

- Look at new markets—might save money!

- Appeal the IRMAA again if necessary

- Continue regular tax/IRMAA management: know how much income you can have before jumping into the next IRMAA bracket

Now here’s a summary of our latest take on market outlook. In a sentence, the vast majority of the key data we see continues to look quite positive and we expect more solid gains from stocks the rest of this year. Here are bullet points:

- First quarter U.S. GDP growth was just revised up to 1.3%--hardly recessionary

- U.S. consumer spending increased more than expected in April, boosting the economy’s growth prospects for the second quarter

- Data from the Commerce Department today showed a surprise rebound last month in orders of manufactured capital goods (this is a closely watched proxy for business spending plans)

- U.S. business activity increased to a 13-month high in May, lifted by strong growth in services

- U.S. job growth accelerated in April (253,000 jobs) and the unemployment rate ticked down from 3.5% to 3.4% (still in historically low range)

- Average hourly earnings rose 0.5%, up 4.4% year-on-year

- Despite the strong labor market & wage gains, the inflation rate in the U.S. unexpectedly edged lower to 4.9% in April, the lowest since April 2021. It was 8.5% a year ago. With the sustained cooling trend in the inflation rate, the Fed is now likely to pause its rate hikes, and we even may a pivot at some point later this year. It is our belief that the Fed’s ‘High-Wire Act’ is almost over.

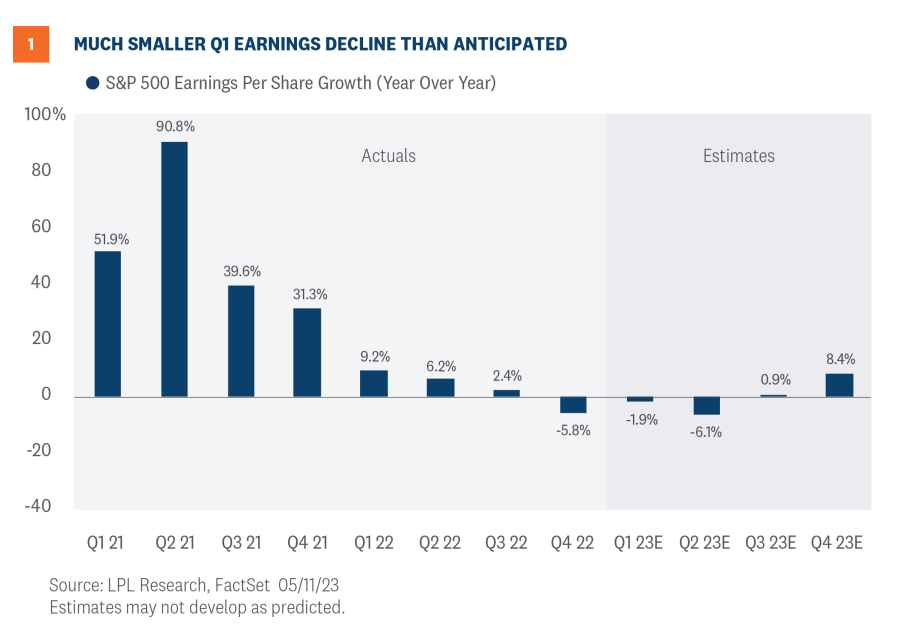

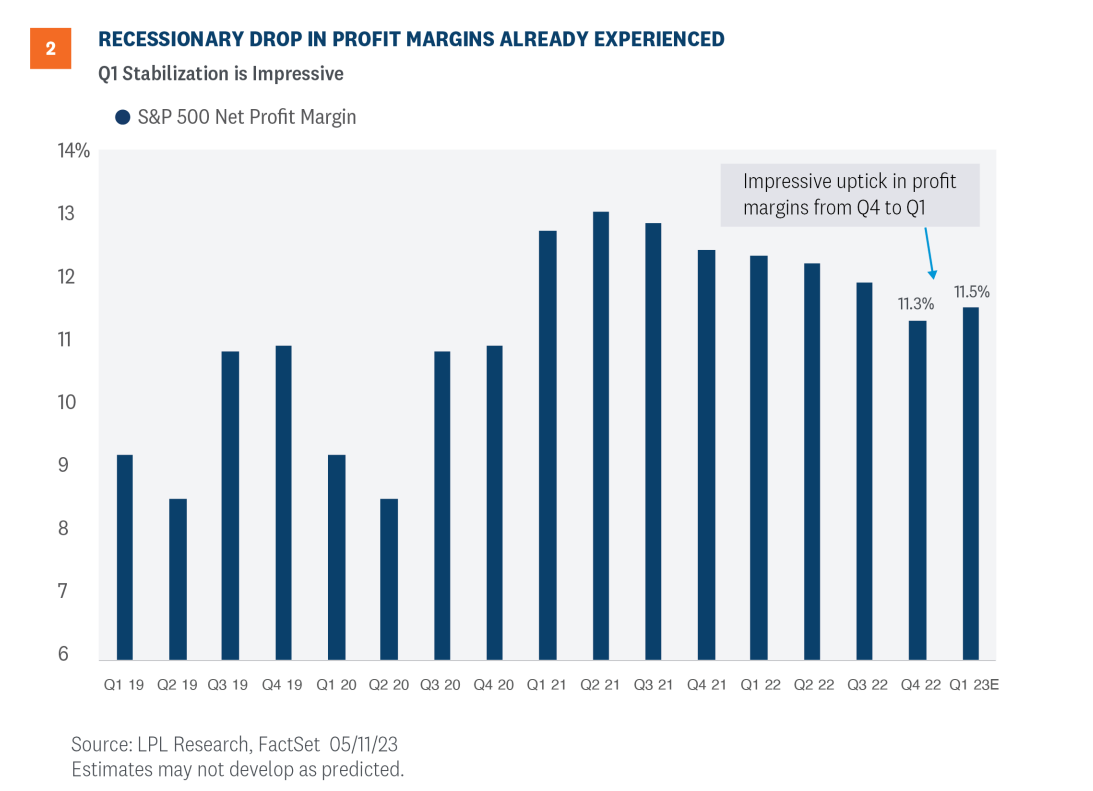

- We had a huge upside surprise with U.S. corporate earnings for Q1, and it appears we have already experienced/gotten past the recessionary drop in profit margins that were most feared. Q1 stabilization was quite impressive.

|

|

While we still feel a recession is far from inevitable, the great lesson of the last 3+ years since the onset of the COVID plague is that, in the short run, anything is possible. Events that might have previously been considered unthinkable—or extreme outliers, at the very least—have become the norm. Consider:

- A hundred-year global health crisis

- A decline of 1/3 in the S&P 500 in a month

- A helicopter-money monetary/fiscal response that propelled the S&P 500 back to its previous peak in five more months

- A 19% contraction in the U.S. GDP- the largest postwar recession by far-that began and ended in 3 months

- A 40% increase in the M2 money supply over 2 years

- A 40-year explosion in inflation

- The sharpest, fastest Fed interest rate spike ever

- A 25% equity market decline in 10 months last year

- Russia and China—two huge, bellicose autocracies experiencing demographic collapse—essentially opted out of the world community

- Iran has moved inexorably closer to developing nuclear weapons

The list goes on. We long-term owners of mainstream American and global businesses are safeguarded, to the greatest extent possible, by the rationality of our managements. When a global pandemic strikes, Marriott will close its hotels and furlough their staffs. When Russia invades Ukraine, McDonald’s will abandon that country. This speaks to the comforting reality that rational business enterprises will always move to preserve their owners’ capital for the long run. That’s the only thing our managers have any real control over, and it’s the only thing we should care about. But it isn’t, is it? Being only human—and subject 24/7 to the depredations of catastrophist financial journalism- it’s all too easy for our focus to get lost to the utterly random ‘stock market’. We start to experience ‘stock market’ declines as ‘losses’ instead of temporary setbacks in the long upward march of shareholder capitalism.

These ‘losses’ can too easily cause us human beings to feel totally self-generated ‘pain’ that feels twice as bad as advances feel good. Finally—and most weirdly—we tend to think the more the market declines, the greater becomes the risk of even worse decline.

Though this is the diametric opposite of all history and logic, it often prompts liquidation of stockholdings at panic prices, which dooms those investors to substandard returns for the rest of their lives. But people who manage to stay strapped in at -20% are gone at -30%. And damn near everybody is gone at -50%--which, has happened three times in the life of an American 50-year-old. But my primary purpose is to help break this vicious psychological cycle once and for all, for those precious few who will allow me to do so! While I am most certainly NOT forecasting a 50% market decline (nor that the sun will come up tomorrow, nor that either you or I will be here to see it even if it does)—as a financial planner, I don’t forecast anything- I prepare for everything. The question is never ‘Is such a decline coming?’ It isn’t even ‘Is such a decline still possible?’ It’s ‘If such a decline were to happen-in response to whatever ‘crisis’—is my client totally prepared to ride it out, as we go through it together?’

Some interesting articles I’ve compiled over the past month:

As always, please don’t hesitate to reach out with questions. Have a great weekend.

Charlie

|

|

Charles G. Brown

Chief Executive Officer, Financial Advisor

|

|

REQUIRED DISCLOSURE:

Investment advisory services provided by NewEdge Advisors, LLC doing business as Marathon Financial Group, as a registered investment adviser. Securities offered through NewEdge Securities, Inc., Member FINRA/SIPC. NewEdge Advisors, LLC and NewEdge Securities, Inc. are wholly owned subsidiaries of NewEdge Capital Group, LLC.

The information contained in this email message is being transmitted to and is intended for the use of only the individual(s) to whom it is addressed. If the reader of this message is not the intended recipient, you are hereby advised that any dissemination, distribution or copying to this message is strictly prohibited. If you have received this message in error, please immediately delete.

|

Marathon Financial Group | 857-201-34320 | 131 Dartmouth St 3rd Floor Boston, MA 02116 | meetmarathon.com

|

|

|

|

|

|

|