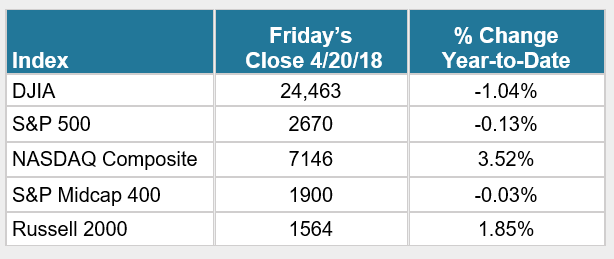

Interpreting The Yield Curve Message

This week the 10-year US Treasury yield broke through the "psychologically important" level of 3.0%, leaving analysts contemplating what it could mean for the future of asset markets and the global economy. The 3 percent level is viewed as a psychological milestone, a wake-up call that interest rates are going higher.

Implications

Rising yields have implications for equity markets; hence the sell-off we witnessed yesterday. Though unclear what the level is, at some point yields will become attractive enough that they will draw money away from other asset classes, like equities. A 3% yield isn't all that much, but it is more attractive than it has been in the past 7 or so years. The rise in yields is happening at the same time Central Banks contemplate additional interest rate hikes. Higher rates mean companies will have higher costs when borrowing money, which leaves them less room to increase salaries, to invest, and to give returns to shareholders - all of which make equities less attractive. And, as the 10-year note is used to set mortgage rates, it can also reduce people's ability to spend on other things.

The Yield Curve

The so-called yield curve, which measures the spread between short- and long-term bond rates, is a key indicator of sentiment about the prospects for economic growth. A flattening yield curve (where the yields of shorter bonds is similar to the yields on longer bonds) is often an economic red flag. The yield curve flattens on its way to inversion, and an inverted yield curve has preceded each of the last nine recessions going back to 1955. While the yield curve has been flattening, market participants remain split on just how ominous the signal is now.

The prospect of Fed rate increases has been driving two-year yields higher, even though the 10-year yield has traded within a narrow range since it last approached 3% in February. That has narrowed the spread between the two yields to about 0.5 percentage point as of Monday, down from 2.65 percentage points at the end of 2013.

Context is important for yield curve conversations because not all types of yield curve flattening are the same. The current flattening has occurred while economic growth continues to be steady, and few analysts see signs of any imminent slowdown. What we have experienced throughout 2017 and year-to-date 2018 is known as a "bear flattener." A bear flattener is an environment in which rates rise across the yield curve, but short-term rates rise more, leading to a flatter yield curve.

While the yield curve certainly warrants ongoing monitoring, a bear flattener has traditionally been a better backdrop for equities and other risk assets. We don't necessarily see it as a warning sign that the economic cycle's end may be imminent.