|

Ryan Statz, Merchant

BARLEY

There remains a lot of interest from producers in malting barley acres for next year’s campaign. Because of the interest, maltsters have been quick to cover a good portion of their needs. In short, buyers are doing everything they can to avoid what happened to their supply chains the last few years. Early AOG coverage was not adequately put on by buyers and when poor growing conditions led to smaller crops, they were forced to operate in very tight supply environments. To procure supply, prices firmed throughout the last few marketing years as they pushed aggressively for coverage. Now, with the past few years and rising prices freshly in buyers’ minds, maltsters came out of the gates early with strong prices to try and buy in AOG acres for ‘23/24 crop. Since the early strength, markets have cooled off as coverage is assessed. We are hearing a lot of ‘23/24 was bought from suppliers early on which will give maltsters a chance to taper interest back some. This is a concern that needs to be watched albeit it is early with a full growing (and weather) season in front of us. Do note, Montana really is the last piece to getting overall barley supply chains back to comfortable levels – Idaho and ND are coming off of very good crops in ‘22/23. If Montana pushes overall supply back to adequate levels - the $7.00-8.00/bu price environment may be in the rearview mirrors.

Please stay in touch with your local CGI buyer about options and what can be done for you.

| |

|

DURUM

Durum markets have been hit with a flurry of fireworks the last few days with some additional international business that has popped into the market. We are a few months away from harvest activity in other parts of the world and most market participants anticipated international demand to wait until this tonnage was harvested and filtered through to soften up world demand. The international interest was a surprise to most and provided short-term life into North American markets that were otherwise grinding lower on a lack of perceived demand left for the remainder of the crop year. Details on the international business have yet to come out and it is still possible that the demand was a head-fake all along in an effort by buyers to draw out offers that would be used as a backstop….we will see.

Going forward, the international interest from North American markets will fade as we get closer to other origins' harvest, and markets at home will be solely dependent on domestic milling demand which in large part remains open and unfilled for Q2 (April, May, June). However, the end of upcoming international business, combined with domestic millers knowing that marketable bushels remain on-farm, has the US market in an uneasy feeling and prices likely grind lower as we approach next year’s crop campaign. Weather providing…

| |

|

BEANS & PULSES

Sean Ferguson, Merchant

PEAS

Market continues to hold a firm tendency due to tight stocks despite the decrease in domestic demand. USDA tenders have slowed in recent weeks but the budget continues to get approval for a continued program. Yellow pea acres are expected to increase while we expect a decrease in green pea acres.

LENTILS

Hottest of all specialty markets with demand leading the way. India, Turkey and Algeria sitting tight on the sidelines watching closely for an opportunity to buy; all needing to pull large volumes.

CHICKPEAS

Demand has been hit hard with currency and USD availability within Pakistan and surrounding areas. Acres are not expected to recover and stocks will likely stay tight into new crop. European buyers begin to look toward new crop coverage but are still early in the process.

DRY BEANS

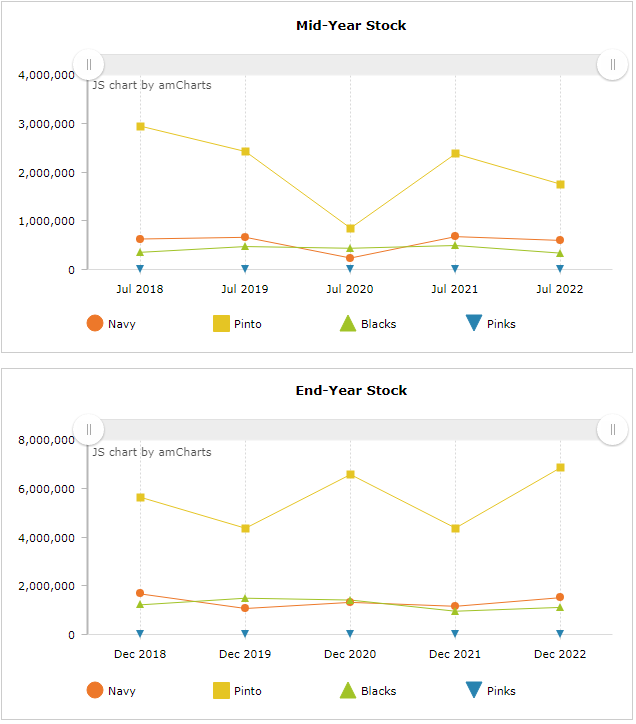

Dry Bean markets are steady nearby with ample demand for both Pintos and Black Beans. NDSU released their estimates for 12/31/2022 North Dakota Dry Bean stocks (below). Pinto Bean stocks are up 58% year-on-year, Black Bean stocks are up 11%, and Navy Beans +31%. Mexico will continue to be a steady buyer of both US pinto and black beans this Spring/Summer due to the drought they experienced. Columbia Grain is now offering new crop contracts and interest is gaining.

| |

|

SPRING WHEAT

Rudy Weitz, Merchant

Spring wheat futures are struggling to find support and continue to bleed lower. In the past 30 days, the front Minneapolis contract has fallen nearly 70 cents and the charts are making spring wheat look oversold. Bullish news has been absent, farmers are disengaged, and the market is desperately searching for any news to bring it back to life. The only two storylines taking center stage in spring wheat are southern plains dryness and how acres will look this spring. Early expectations feel like spring wheat acres are unchanged to down a bit. Still early to tell but projections should become clearer in the coming weeks.

With the drop in the board, we have seen the domestic market begin to wake up a bit. Millers have been bogged down and overrun by wheat but the drop off in futures has encouraged flour sales. While they are cautiously looking for some wheat, the milling market is relatively covered, and no one is looking to book volume. Exports remain slow less typical business, as US spring wheat rates itself globally uncompetitive. I’d stress that with the drop in the board, it’s still important to be an active marketer. A few timely rains in the southern plains can still tank the whole wheat complex and a small jump in futures could continue to tank the basis. $8 cash is still very solid, and if you can sell that today you’re taking risk off the table at a historically good price. Be proactive, not reactive.

| |

|

Joe Foley, Merchant

CORN

Corn futures have really been struggling of late, down .50/bu. over the last two weeks. The market’s focus has been on the demand side of the U.S. balance sheet, specifically the very poor pace of exports. Indeed, the USDA today reduced exports further by 75mln bu., down to 1,850mln bu. This is in sharp contrast to last yr’s 2,471mln and the previous yr’s 2,747mln bu. It’s all about China’s absence from our export market (4.5mmt U.S. purchases vs 12.1mmt a yr ago this time), as well as Brazil’s increases in both production and exports. This is the first year that Brazil is forecast to be the world’s largest corn exporter, supplanting the U.S. ...Brazil is expected to harvest 125mmt (116mmt last yr), which comes at the expense of our exports. That said, some 75% of Brazil’s corn crop is their winter corn (safrinha) which comes off later this summer, and as such that crop has not yet been made. But early conditions are good, although late planted which increases the odds of adverse weather during pollination. Market will continue to monitor that, as well as whether U.S. export sales can pick up some steam over the next few weeks, as seasonally April to June shipments are our most competitive positions.

| |

|

SOYBEANS

Soybean prices remain rangebound from 14.80 to 15.30, basis CBOT May futures. The U.S. balance sheet remains tight, even more so with today’s WASDE report that lowered our carryout estimate to 210mln bu., from 225mln last month. Exports were increased by 25mln bu, which more than offset a 10mln bu reduction in domestic crush. All eyes were on the international numbers though, especially the sharp reduction in Argentina’s crop over the last few weeks. Indeed, the USDA lowered their production estimate by 8mmt down to 33mmt (vs. 44mmt ly), but market estimates are still another 5-7mmt less than that. The dwindling size of Argentina’s crop remains the most bullish element for future price direction. Brazil and the U.S. will need to export more soybean meal to make up for Argentina’s shortfall. Recall Argentina is the world’s largest exporter of meal so crush margins will stay firm as a result. Tempering this bullishness is Brazil’s massive crop which is still estimated at 153mmt (vs. 130mmt ly) as well as questionable demand going forward, especially from China. Look for continuing S. America production estimates and the March 31 stocks and planting intentions report for further price direction.

| |

|

OILSEED MARKET

Sean Ferguson, Merchant

The USDA WASDE was released today. The USDA pegged the Argentinian soybean crop at 33MMT (down from 41MMT last month). Despite this recent drop, the USDA is still rich in its estimates compared to private counterparties hovering in the mid-to-high 20MMT range. Funds remain record long meal futures, although meal prices will continue to be supported by the Argentinian crop situation until funds begin to unwind their long positions. Matif rapeseed is lower over reported imports of 5.7MMT of rapeseed (39% YoY increase), mostly coming from Ukraine. Palm oil is down with the record Brazilian soybean crop along with a lower crude. May Canola futures are down roughly 20 CAD/MT from an 826.30 CAD/MT high of a week ago on the heels of lower Matif rapeseed.

It has been a wild week on the forex front, with the USD taking center stage following Chairman Powell’s recent testimony on Capitol Hill. Powell explained there is a “long way to go and is [fight against inflation] likely to be bumpy”. Powell’s hawkish comments have driven the USD upward against all its G10 peers. The CAD does not share the same story of its greenback cousin. With good employment numbers coming out of Canada and inflation continuing to stay low, the Bank of Canada ultimately has less pressure to veer from its original intentions of pausing future interest rate hikes. The mix of a dovish central bank and lower crude values puts the CAD in a marginally lower position.

| |

|

BULLISH:

- Strong export demand (especially to China)

- South American crop issues/logistics

- Small North American carryout

| |

|

BEARISH:

- Funds long canola, soy oil, and soy meal futures

- Chinese demand ration or import from alternate origin

| |

COLUMBIA GRAIN PRODUCER SOLUTIONS

Phil Symons

Well, the March USDA Supply and Demand report has come and gone, now onto watch the fight for acreage between corn and beans as the next major report on tap will be the March 31st planting intentions report along with the March 1 quarterly stocks report. This report gets a lot of attention year in and year out as it gives the trade targeted numbers to base their overall expected U.S. production on. Weather is always an influencing factor on market trends and overall price direction, as we move further into the calendar this year weather events will begin to have much more of an impact on the overall price direction and potential knee-jerk reactions to the market prices. Be sure to get your orders out there and working so you are prepared for when the knee-jerk reactions happen. Explore all of the marketing tools that we have to offer. Remember, there is no one silver bullet tool, the market will dictate what we should be doing and the marketing tools we should be using.

We are excited to announce that we have officially launched the Columbia Grain Bushel App. Be sure to visit the App Store to download the Columbia Grain Bushel App on your Smartphone of choice. The accompanying picture has a QR code that you can scan with your phone to open the Columbia Grain Bushel App. If you have any questions on any of these new aspects, please feel free to contact your local Columbia Grain Merchandiser.

| |

|

SOFT WHITE WHEAT

Steve Yorke, Merchant

White wheat markets are trending lower along with futures as traders continue to wait on information out of the Black Sea on a new corridor agreement. Weather also playing a major role as conditions remain dry in key wheat-producing states. Kansas wheat conditions declined this week which helped stabilize futures a touch after last week’s pounding. At this writing, white wheat is trying to stay above $8.00 which is off about 30c from two weeks ago. Export demand has been light, but grower selling has also been light, so we were able to stay above $8.00 for the time being. The latest USDA report had no surprises for wheat. The Aussie crop was pegged at 39.0MMT as expected after ABARES reported their number at 39.2. White wheat exports remained at 190MBU for the marketing year which keeps carry out tight moving forward. All in all, the report did not provide any bullish factors to improve old or new crop cash prices. On the bright side basis has improved for new crop, currently at .40-.50c range. Weather and the Black Sea region will continue to be the driving forces as we move into springtime. Watch for futures rallies to provide HTA and accumulator opportunities and place your orders with our buyers to ensure your orders are executed if targets are reached.

| |

|

INTERNATIONAL

Tatsuya Segawa, Merchant

WHEAT

USDA has increased its 22/23 global crop production forecast, especially for Australian and Indian, while Russia unchanged at 92MMT. New global production forecast is 788.9MMT which is a 5.1MMT increase from last month. There is not much new news in the US export mkt though, some buyers in the Philippines keep buying Soft White wheat in combination with CWRS. CWRS FOB price is still more than half a dollar per bushel cheaper than NS. Very little wheat tender business left in March. Hopefully, demand will come back soon in response to the recent futures drop.

CORN

USDA has lowered its 22/23 crop export numbers. US corn exports for 22/23 crop are now projected at 1.85 billion bushels, which is down from 1.925 billion bushels in last month’s report. Accumulated US corn exports are down by 42% at the same point of last year. The overseas buyers in Asia have continuously moved to cover their demand week by week but PNW corn is no longer competitive to Asia. Korea has moved at least 5 cargoes for eta July position in this week, but it is said that these origins would be SAF, SAM or US GULF. Taiwan has also bought 1 cargo from SAF. Current PNW corn is at least .10/bu higher than other origins.

| | | | |