In This Issue:

- Market Update: Colombia Rice Tariff Rate Quota Unfulfilled

- LA Governor Edwards Attends Rice Mill Groundbreaking

- Sabor USA's Thanksgiving Dinner

- Washington Update: 2021 Wrap Up

|

|

Market Update: Colombia Rice Tariff Rate Quota Unfulfilled |

|

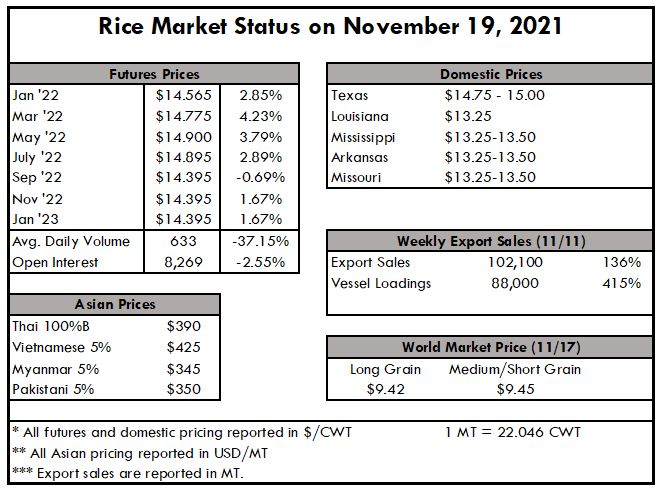

If not before, early 2022 will give farmers some hard numbers as to the reality of the overall supplies resulting from apparent lower-than-hoped milling yields throughout the delta region. Most anticipate a tighter supply going forward. 2022 rice planting decisions are up in the air in light of the high cost of fertilizer and many are shifting more attention to soybeans. The bridge to the new harvest seems to be getting longer and the outlook for farm prices remains positive. The question is if farmers can take advantage of the expected conditions.

Since October 1st, the long grain spot market has been largely sideways throughout most of the delta. Cash prices have appreciated only 2% since harvest whereas futures are up nearly 3.5%. Although the market lacks a little excitement on the export front, domestic millings are up an impressive 13.5% year to date. Sluggish paddy exports are being offset by an increase in milled rice exports.

Argentina recently encroached on a key US market, as the country sold 10,000 MT of paddy to Mexico. Brazil is also proving to be a formidable competitor in the paddy arena with stronger shipments to Costa Rica and Venezuela. The improved milling activity in the US is attributed to greater milled rice shipments to markets in Latin America where Brazil and Argentina appear to be less engaged. Higher domestic use is also thought to be a supporting factor. Fortunately, the export market is propped by the milled market segment, which should begin to have a positive impact on the market if it remains strong.

|

|

Governor Edwards attends groundbreaking ceremony for rice mill in Acadiana |

Posted: Nov 19, 2021 / 08:43 AM

JEFF DAVIS PARISH, La. (KLFY) A new rice mill will soon be up and running in Jeff Davis Parish.

Governor John Bel Edwards attended the groundbreaking ceremony for the new $8.4 million facility Thursday afternoon.

The governor says this will be huge for local rice farmers and says it’s a major agricultural win for the region and for our state.

|

|

The USDA posted a statement this week, alerting the US rice industry that the Colombia Rice TRQ went unfulfilled for the first time. Even with the advantages extended through the US-Colombia Trade Promotion Agreement (TPA), US rice sales to Colombia have slid to roughly $5 million in 2021. Colombians are citing their larger crop and lower domestic prices as the reason for lower US rice imports. However, the US rice traders are quick to rebut that a growing presence of South American rice in Colombia is another key component to the weaker sales. Colombia was the 8th largest market for US rice exporters in 2020 in terms of value, making it a critical market for US long grain.

India’s rice exports tapered off significantly this month as demand in Africa wavered. As prices have eroded for the past few weeks throughout Asia, many buyers are postponing their purchases in hopes of securing more favorable prices later. This is compounding the supply situation, adding further negative pressure to the market. Prices in India were assessed at $359 FOB last week and were moved down to $354 FOB this week; Vietnam saw similar price action. Some traders expect the drop in pricing to precipitate greater demand but believe that has been slow to materialize because of high logistics costs.

|

|

Sabor USA - Thanksgiving Dinner |

|

The US Rice Producers Association and USA Rice participated in Sabor USA's 2021 Thanksgiving Dinner press conference on November 17th. The activity was organized by the U.S. Department of Agriculture to promote American products in Guatemala.

This year, due to COVID-19, the press conference was limited to media representatives and special guests only. Guatevision, TV Ateca, El Periodico, Nuevo mundo, Prensa libre, Revista industria, Revista Forbes, Grupo News among others covered the event.

Agriculture Attache, Andrew Hochhalter, welcomed U.S. Ambassador William Pop.

Roberto Wong attended the event as a USRPA's representative and promotional items were given away to the attendees.

Luis Reyes, Chef of the AC Marriott Hotel, oversaw the preparation of a delicious Christmas rice dish that will be served on the hotel's Thanksgiving menu.

|

|

Washington Update - 2021 Wrap Up |

|

There are still several large items that must be resolved before the new year. Congress is currently focused on the reconciliation bill, Build Back Better Act. The House is scheduled to consider the legislation this week after House progressives agreed to support the Infrastructure Investment and Jobs Act in exchanged for a commitment to consider the Build Back Better Act no later than the week of November 15. Additionally, five moderate House Democrats issued a statement agreeing to vote for the Build Back Better Act as soon as they see a Congressional Budget Office (CBO) fiscal analysis. Timing of Senate consideration will depend on when the House passes the bill and the CBO scores.

In addition to reconciliation, Congress must pass legislation to fund the government and avoid a shutdown. FY 2022 appropriations bill have been written and negotiations are ongoing, but leadership remains far apart on reaching a topline agreement. We are currently operating under a continuing resolution (CR) set to expire on December 3. Congress must pass the 12 appropriations bills, or another continuing resolution, before then. At the moment, the Senate is considering a two-to-three-month CR, punting appropriations to early next year. However, House Appropriations staff are still expecting to see a short-term CR. Some House Democrats are pushing for a shorter, two-week CR that would pressure Congress to come to an agreement before the holidays.

Congress must also raise the debt ceiling. Included in the CR was a $480 billion debt limit extension that would allow the U.S. to avoid a default. Treasury Secretary Janet Yellen estimated the extension would allow the federal government to continue to pay its bills until December 15.

There are also a number of other items Congress must address before the new year, including Temporary Assistance for Needy Families (TANF) benefits, which will expire on December 3, and Coronavirus Relief Fund for States & Localities and approximately twenty tax extenders, which will expire on December 31.

Senate Confirms Bonnie

This week, the Senate voted 76-19 to confirm Robert Bonnie as Under Secretary for Farm Production and Conservation at USDA. Bonnie will oversee disaster, commodities, crop insurance, and conservation programs.

Bonnie is currently deputy chief of staff and a senior climate advisor to Secretary Vilsack.

|

|

Ray Stoesser Memorial Scholarship |

|

|

|

In partnership with the US Rice Producers Association, the Stoesser family is offering a $5,000 scholarship to one deserving high school senior or current college student who is interested in or is currently pursuing a career in an agriculture-related field.

|

|

|

|

Colombia Rice TRQ

Unfilled for the First Time

|

|

|

|

|

|

Food & Ag

Regulatory & Policy Roundup

|

|

|

|

|

Post forecasts MY2021/22 rice production to increase to 21 million metric tons despite flooding. Posts expects Thai rice exports to increase to 5.8 million metric tons in 2021.

|

|

|

|

CLL16 Clearfield®

Long Grain

The Complete Package for Furrow and Paddy Rice

|

|

|

|

|

|

34th Annual Arkansas Agricultural Hall of Fame Induction Luncheon: Embassy Suites, Little Rock, Arkansas – event details and tickets (RESCHEDULED) |

|

25722 Kingsland Blvd.

Suite 203

Katy, TX 77494

p. (713) 974-7423

f. (713) 974-7696

www.usriceproducers.org

|

|

We Value Your Input!

Send us updates, photos, questions or comments!

|

|

USRPA does not discriminate in its programs on the basis of race, color, national origin, gender identity, sexual orientation, religion, age, disability, political beliefs, or marital/family status. Persons who require alternative means for communication of information (such as Braille, large print, sign language interpreter or translation) should contact USRPA at 713-974-7423 |

|

|

|

|

|

|