|

Quick Hits

1. Stocks Rally in September to Cap Off Strong Third Quarter

Stocks continued to rise in September as improving fundamentals and lower interest rates supported returns.

2. Strong Quarter for Bonds

September capped off a strong quarter for bond investors.

3. Federal Reserve Cuts Interest Rates

The Fed lowered the federal funds rate in September for the first time in more than four years.

4. Healthy Economic Backdrop

Economic updates released during the month showed signs of continued growth.

5. Real Risks Remain

Markets face a variety of risks as we kick off the fourth quarter.

6. Cautious Optimism Warranted

The most likely path forward is for continued market appreciation and economic growth.

Stocks Rally in September

Stocks continued their recent rally in September, with all three major U.S. indices up for the month and quarter. The S&P 500 gained 2.14 percent in September and 5.89 percent for the quarter, while the Dow Jones Industrial Average (DJIA) was up 1.96 percent during the month and 8.72 percent for the quarter. Both the S&P 500 and DJIA hit new record highs in September before falling back modestly to end the month. The technology-heavy Nasdaq Composite gained 2.76 percent for the month and quarter as technology stocks experienced heightened turbulence over the summer compared to the broader market.

These positive results were supported by improving fundamentals. Per Bloomberg Intelligence, the average earnings growth rate for the S&P 500 in the second quarter was nearly 14 percent. This is well above analyst estimates at the start of earnings season for a more modest 8.3 percent increase. Because fundamentals ultimately drive long-term market performance, this was an encouraging development for investors as it showcased the continued health of American businesses.

Technical factors were supportive as well for the month and quarter. All three major indices spent the entire month well above their respective 200-day moving averages. (The 200-day moving average is a widely tracked technical signal, as prolonged breaks above or below this level can indicate shifting investor sentiment for an index.) All three of the major U.S. indices have spent the entire year above their respective trendlines, indicating continued investor support for U.S. stocks.

The story was similar internationally for the month and quarter. The MSCI EAFE Index gained 0.92 percent in September, capping off a 7.26 percent gain for the quarter. The MSCI Emerging Markets Index surged 6.72 percent in September, which contributed to an 8.88 percent gain for the quarter. The announcement of major stimulus policies in China toward the end of the month led to the outperformance for emerging markets in September.

Technical factors were supportive for international stocks during the month. Both indices spent the entire month above trend. This was especially encouraging for the emerging market index, which had previously briefly dipped below its 200-day moving average in early August.

Strong Quarter for Bonds

September was another positive month for bonds, capping off a strong quarter for fixed income investors. Falling interest rates over the month and quarter helped support bond returns throughout the summer. The 10-year Treasury yield fell from 4.48 percent at the start of July to 3.81 percent by the end of September. Short-term rates fell notably as well during the quarter due to heightened expectations for

Fed rate cuts. The Bloomberg Aggregate Bond Index gained 1.34 percent during the month and an impressive 5.20 percent in the third quarter.

High-yield fixed income, which is typically less driven by interest rate movements, also had a strong month and quarter. The Bloomberg US Corporate High Yield Index gained 1.62 percent in September and 5.28 percent for the quarter. High-yield credit spreads compressed from 3.21 percent at the start of the quarter to 3.03 percent at quarter-end. Tighter credit spreads indicate increased investor appetite for high-yield investments.

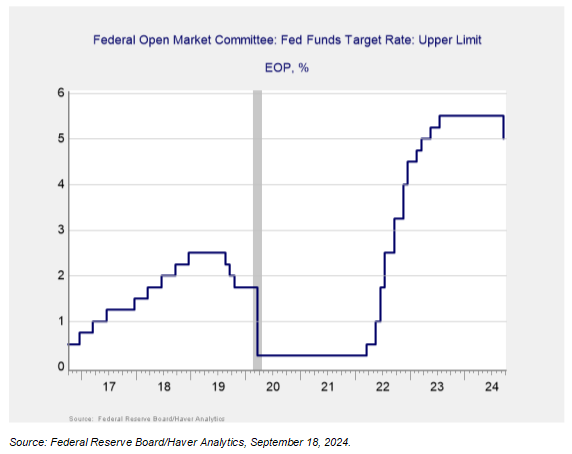

Federal Reserve Cuts Interest Rates

The Fed cut the upper target of the federal funds rate by 50 basis points at the conclusion of its September meeting. This brought the upper limit from 5.50 percent down to 5.0 percent. As you can see in Figure 1, this marked the first interest rate cut in more than four years and indicates that the Fed is shifting away from the restrictive monetary policy that we’ve recently experienced in favor of more supportive policy ahead.

Figure 1: Federal Open Market Committee Federal Funds Target Rate Upper Limit, October 2016–Present

|