|

Compliance Code: 8362062.1

This commentary was authored by the investment team at Summit Financial, LLC., an SEC Registered Investment Adviser (“Summit”), headquartered at 4 Campus Drive, Parsippany, NJ 07054, Tel. 973-285-3600. It is provided for your information and guidance and is not intended as specific advice and does not constitute an offer to sell securities. Summit is an investment adviser and offers asset management and financial planning services. Indices are unmanaged and cannot be invested into directly.

Data in this newsletter is obtained from sources which we, and our suppliers believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. Consult your financial professional before making any investment decision. Past performance is no guarantee of future results. Diversification/asset allocation does not ensure a profit or guarantee against a loss. Economic and market forecasts presented herein reflect our judgment as of the date of this presentation and are subject to change without notice. Any forecasts are subject to high levels of uncertainty that may affect actual performance. Accordingly, forecasts should be viewed as merely representative of a broad range of possible outcomes. Forecasts are estimated, based on assumptions, and are subject to significant revision and may change materially as economic and market conditions change. Forecasts do not take into account the specific investment objectives, restrictions, tax and financial situation or other needs of any specific client.

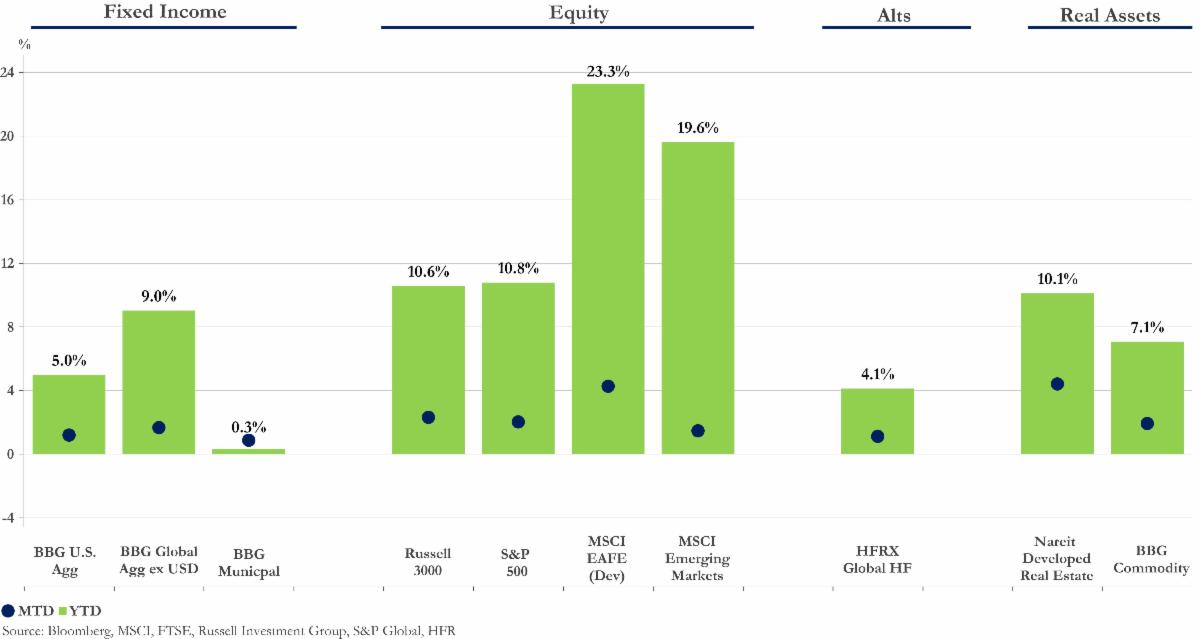

BBG U.S. Agg

Bloomberg U.S. Aggregate Bond Index

The Bloomberg U.S. Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed- rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate pass-throughs), ABS, and CMBS (agency and non-agency).

BBG Global Agg ex USD

Bloomberg Global Aggregate Index

The Bloomberg Global Aggregate Index is a flagship measure of global investment grade debt from twenty-four local currency markets. This multi- currency benchmark includes Treasury, government-related, corporate, and securitized fixed-rate bonds from both developed and emerging markets issuers.

BBG Municipal

Bloomberg Municipal Bond Index

The Bloomberg Municipal Bond Index covers the U.S. dollar-denominated long-term tax-exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds, and pre-refunded bonds.

Russell 3000

Russell 3000 Index

The Russell 3000 Index measures the performance of the largest 3,000 U.S. companies representing approximately 98% of the investable U.S. equity market. It is constructed to provide a comprehensive, unbiased, and stable barometer of the broad market and is completely reconstituted annually to ensure new and growing equities are included.

Russell 2000

Russell 2000 Index

The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe. It is a subset of the Russell 3000 Index repre- senting approximately 10% of the total market capitalization of that index. It includes approximately 2,000 of the smallest securities based on a combi- nation of their market cap and current index membership.

S&P 500

S&P 500 Index

The S&P 500 Index is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. It measures the movement of the largest issues. Standard and Poor’s chooses the member companies for the 500 based on market size, liquidity, and industry group representation. Included are the stocks of eleven different sectors.

MSCI EAFE (Dev)

MSCI EAFE Index

The MSCI EAFE Index (Europe, Australasia, Far East) captures large- and mid-cap representation across developed markets countries around the world, excluding the U.S. and Canada. The index covers approximately 85% of the free float-adjusted market capitalization in each country.

MSCI Emerging Markets

MSCI Emerging Markets Index

The MSCI Emerging Markets Index captures large- and mid-cap representation across emerging markets countries across the world. The index covers approximately 85% of the free float-adjusted market capitalization in each country.

HFRX Global HF

HFRX Global Hedge Fund Index

The HFRX Global Hedge Fund Index is comprised of funds representing the overall hedge fund universe. Constituent funds include but are not limited to convertible arbitrage, distressed securities, equity hedge, equity market neutral, event-driven, macro, merger arbitrage, and relative value arbitrage. The underlying strategies are asset-weighted based on the distribution of assets in the hedge fund industry.

Nareit Developed Real Estate

FTSE EPRA/NAREIT Developed Index

The FTSE EPRA/NAREIT Developed Index is designed to track the performance of listed real estate companies and REITS worldwide. Index constituents are free float-adjusted, subject to liquidity, size, and revenue screening for inclusion.

BBG Commodity

Bloomberg Commodity Index

The Bloomberg Commodity Index reflects commodity futures price movements and is calculated on an excess return basis. The index rebalances annually weighted 2/3 by trading volume and 1/3 by world production, and weight-caps are applied at the commodity, sector, and group level for diversification. The roll period typically occurs from the 6th-10th business day based on the roll schedule.

Consumer Confidence Index

Conference Board Consumer Confidence Index

The Consumer Confidence Index is a measure based on a survey administered by The Conference Board that reflects prevailing business conditions and likely developments for the months ahead. This monthly report details consumer attitude, buying intentions, vacation plans, and consumer expectations for inflation, stock prices, and interest rates.

U.S. Dollar Index (DXY)

U.S. Dollar Index (DXY)

The U.S. Dollar Index (DXY) is an index of the value of the United States dollar relative to a basket of foreign currencies, often referred to as a basket of U.S. trade partners' currencies. The Index goes up when the U.S. dollar gains "strength" (value) when compared to other currencies.

DJIA

Dow Jones Industrial Average

The Dow Jones Industrial Average (DJIA), commonly known as “The Dow”, is a price-weighted measure of 30 U.S. blue-chip companies. The index covers all industries except transportation and utilities.

ISM Manufacturing Index

ISM Manufacturing Index

The ISM Manufacturing Index, also known as the purchasing managers’ index (PMI), is a monthly indicator of U.S. economic activity based on a survey of executives covering all North American Industry Classification System’s businesses in the manufacturing sector.

ISM Non-Manufacturing Index

ISM Non-Manufacturing Index

The ISM Non-Manufacturing Index is a monthly indicator of U.S. economic activity based on a survey of executives covering all North American Industry Classification System’s businesses in the services (or non-manufacturing) sector.

|