|

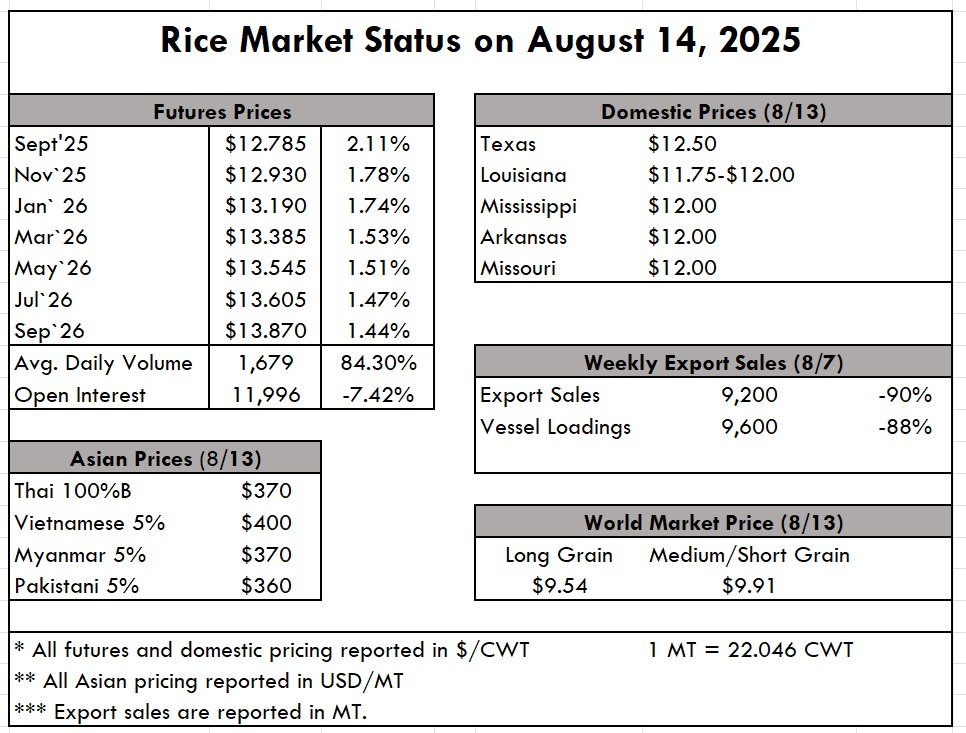

After weeks of what has been a quiet market, the pressure of new crop deliveries is finally shaking some news loose. Reports we are receiving, while not positive, are shining a spotlight on the final dark corners of old crop. Lines of trucks are extremely long at rice mills in Arkansas as farmers have to make room in their bins for new, and are therefore shipping sold old crop to the mills. The problem is 3-fold: the first is that the lack of demand on the milling side is creating a logjam for paddy deliveries. The second is that loads are being rejected due to bugs, and the third is that rejected loads are being rejected due to quality. We say the spotlight is being shone on the dark corners here because whispers of these problems have been noted for weeks, but there is no hiding it at this point. Farmers are draining fields early due to heat, and Mother Nature is forcing these concerns to the forefront. Farmers are anxious about field yields in Northeast Arkansas, along with quality results. With such a difficult year, good yields would take a little of the edge off, hopefully, while the price outlook continues to be worrisome.

The WASDE report just came out this week, casting another bearish factor into the rice market, largely on account of increased ending stocks by 700,000cwt (of which much is poor quality), and an increase in harvested acres by 52,000 acres from the June report. The last thing farmers or millers need right now is more supply popping up. To add a layer of complexity to the matter, some are deliberating if Arkansas base acres might need to be adjusted given that the state has announced production of appx 1.2million acres this year, with appx 500,000 acres in Prevent Plant. On a broader scale, the U.S has just over 5 million base acres of rice, and only 2.8 million acres in production. While there is no clear solution, it is certainly food for thought and perhaps a battle for another day.

The FAO Rice Price Index declined by 1.8% in July, down to an average of 103.5 points. This is 22.3% below its value at this time last year, and the lowest level since March of 2022. We have consistently been reporting the price drop in Thailand, Vietnam, and India, all of which have led to the index weakening. Unfortunately, this oversupply is also being met with a weak demand complex, further exacerbating the problem. The largest price drop in the last 45 days has been in Thailand, and the hope is that their price will snap back to Viet/India levels, as opposed to the Viet/India prices sinking down to Thai prices. Mercosur, primarily Brazil and Uruguay, has registered recent rough rice sales to Mexico, Guatemala, and Costa Rica, with milled rice in containers to numerous markets. Brazilian paddy rice is dipping below $290/ton FOB, while milled rice is around $480/ton FOB in bulk, close to $100 lower than the U.S.

The price chart below shows the global downtrend in rice prices. The U.S. is the red line, which is holding the highest and has dropped the least; however, this doesn’t tell the whole story. Exports have also slowed significantly, thereby stagnating what the price movements may actually be. Overall, the global rice complex is in a tough spot, and will take time to revolve back into a more positive place

|