|

**Disclamier: The views expressed in this interview do not represent or imply endorsement of the University of Arkansas System Division of Agriculture toward any commercial entity, service, or product.

Historically low commodity prices, high input costs and expensive financing have been some of the most significant issues farmers have faced in the last few years. Luckily, some financial relief may come in the form of lower interest rates from the Fed reducing COVID-era rate increases (Wright, 2024). The Fed aggressively moved in September to cut 50 basis points, bringing the target Federal Funds rate to 4.75 – 5%, with indications for at least another 50 basis points before the end of 2024 (Fannie Mae, 2024). This article explores a hypothetical situation of a producer leveraging lower interest rates to consolidate debt to improve short-term liquidity.

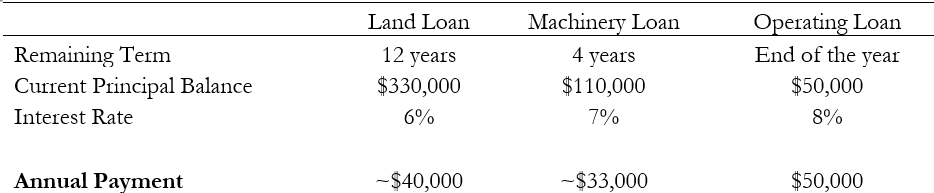

Consider a farmer’s debt obligation for 2024 (Table 1). In this scenario, the farmer holds a land loan with an original principal balance of $450,000 at a fixed interest rate over 20 years. As of 2024, the remaining principal stands at $330,000, with 12 years left in the repayment period. Additionally, the farmer has a machinery loan with an original principal balance of $180,000, structured over a 7-year term. The outstanding balance on this loan is currently $110,000, with 4 years left until maturity.

The farmer also faces a $50,000 operating loan, due at the end of this year. Unfortunately, this year has not been profitable, and he cannot cashflow all his debt obligations.

|