NONPROFIT

CONNECTION

Newsletter by Hawkins Ash CPAs

|

|

In this edition

August 2018

What You Need to Know About the New Expense Reporting Requirements

Nonprofit Tax Tidbits:

Form 990 Schedule G

Fundraising Event Considerations: Part II

DHS Audit Requirement Update

Client Feature and Executive Direct Q&A:

Home and Community Options

|

|

|

What You Need to Know About the New Expense Reporting Requirements

|

|

The countdown is on for the implementation of the new FASB Accounting Standards Update 2016-14 (the standard). The standard will take affect for years beginning after December 15, 2017. One of the biggest changes in the standard is the reporting of expenses. Having discussions now gives management time to gather the information needed to implement these changes.

What Are the Changes?

- All nonprofits will be required to present their expenses by both their natural and functional classifications in one location. This can be done either on the statement of activities, as a separate schedule or in the notes to the financial statements.

- All nonprofits will be required to disclose the methods used to allocate costs among program and supporting functions.

What You Should Do To Prepare

- Decide where you would like to present the expenses by natural and functional classifications. Our recommendation is to have a separate statement of functional expenses.

- Develop a cost allocation plan. Organizations should carefully review their expenses to determine if they need to be allocated to more than one function, while others will be direct expenses to just one function. This may require organizations to update methods they have previously used or create a whole new methodology. Organizations should document the methods used to allocate expenses to more than one function.

What Expenses Should Be Allocated

Before you can determine what costs should be allocated, you need to understand the functional expense categories.

- Program services are activities carried out in fulfilling an organization's mission or purpose and are the major purpose for, and output of, the organization. Program service expenses are the direct and indirect costs related to providing program services.

- Supporting services are activities other than program services. While organizations may have various kinds of supporting services, they typically relate to the following activities: management and general (M&G) activities, fundraising activities, and membership development activities.

The new standard clearly defines M&G activities to include the following:

- Oversight

- Business management

- General record keeping and payroll

- Budgeting

- Financing, including unallocated interest costs

- Soliciting funds other than contributions and membership dues (for example, the costs associated with promoting the sale of goods or services to customers, including advertising costs; administering government, foundation, and similar customer-sponsored contracts, including billing and collecting fees)

- Disseminating information to inform the public about the organization's stewardship of contributions, making announcements about appointments, and producing the annual report

- Employee benefits management and oversight (Human Resources)

- All other management and administration except for direct conduct of program services, fund-raising activities, or membership development activities

Some common expenses that need to be allocated are salaries/wages, benefits, occupancy costs including rent, utilities, insurance, repairs and maintenance and deprecation. There are a few different methodologies you can use to allocate costs. One methodology is based on employee time which may require a time study be done. Time studies can be as elaborate as having each individual track their time daily through a time management system or hire an outside contractor to conduct a time study for each functional category. Less elaborate time studies can be as simple as picking a “representative” one week to one month in the year and having each employee track their time daily to each functional category. A “representative” period of time is one that is similar to what is done year-round. A common method for allocating expenses pertaining to space/occupancy would be to allocate based on square footage.

The key is to ensure you document the methodologies that you use and that there is some basis behind your methodologies. You should also review your cost allocation plan annually at a minimum.

If you have any questions in regards to the new expense reporting requirements, please contact your Hawkins Ash CPAs representative.

|

|

|

|

Author:

Briana Peters, CPA

Direct: 920.337.4549

|

|

Nonprofit Tax Tidbits:

Form 990 Schedule G

|

|

Preparing Schedule G is something I would not advise working on during a late Friday afternoon. A morning early in the week would be better. I also strongly recommend drinking a cup of black coffee or better yet, a 5-hour Energy drink to get you through it. All joking aside, Schedule G is one of the most challenging schedules for our clients to prepare. However, it does not have to be difficult if you properly track events during the year.

Schedule G is used to report professional fundraising services, fundraising events, and gaming. Organizations that report more than $15,000 of expenses for professional fundraising services are required to complete Part I of Schedule G (Note: Form 990-EZ filers are not required to complete Part I). Organizations that report more than $15,000 of gross revenue from fundraising events are required to complete Part II of Schedule G. Organizations should complete Part III of Schedule G if they reported more than $15,000 of gross income from gaming activities.

Part I

The IRS defines professional fundraising services as services performed for the organization requiring the exercise of professional judgement or discretion consisting of planning, management, preparation of materials, and/or provision of advice and consulting regarding solicitation of contributions. Professional fundraising does not include services provided by the organization’s employees or board members in their capacity as employees and board members nor does it include purely ministerial tasks such as printing, mailing services, or receiving and depositing contributions to a charity. If the organization has an agreement, whether written or oral, with a professional fundraiser under which the fundraiser will be compensated at least $5,000 by the organization, it will be required to report the details of the agreement. Details include the name and address of the fundraiser, the activity, if the fundraiser has custody or control of contributions, gross receipts from the activity, the amount paid to the fundraiser, and the net amount received by the organization.

Part II

The two largest fundraising events with gross receipts greater than $5,000 will be broken out and the remaining fundraising events with gross receipts greater than $5,000 will be combined and entered under other events. Organizations need to ensure they track the gross receipts from a fundraising event as well as the contributions received by the organization for the fundraising events. This is one area organizations struggle because they don’t keep the detail of the gross receipts from the fundraising event. Therefore, they have a hard time determining the amount attributable to contributions. Contributions included in gross receipts are the total amounts received where there is no adequate consideration or exchange transaction taking place.

The other area of Part II that organizations struggle with is the reporting of expenses related to fundraising events. Organizations are required to report the direct expenses incurred by the organization to host the event. Line items on Schedule G include cash prizes, noncash prizes, rent/facility costs, food and beverages, entertainment, and other direct expenses.

Contributions are subtracted from the gross receipts and often times the net income summary on Part II will show a loss from fundraising events due to the IRS reporting requirements. However, this does not mean that the event generated a net loss. Organizations have to look at the amount of contributions received because of the event. A good question to ask is: if that event was discontinued, would we have received these contributions?

Part III

For this section of Schedule G, treat all bingo as a single event and all pull tabs as a single event. The organization will need to report the gross revenue from bingo, pull tabs/instant bingo/progressive bingo and other gaming. Expenses will need to be broken out by cash prizes, noncash prizes, rent/facility costs, and other direct expenses. Organizations should also track if these activities are done by volunteers and the percentage of time volunteers spend conducting the activity.

In Conclusion

In order for the organization to properly complete Schedule G, it is important that the organization tracks the detail of their fundraising events to know the amount of contributions received as well as the detail of the expenses. It may be beneficial to create a different general ledger account for each fundraising activity to properly segregate the revenues and expenses. Schedule G can be a good resource for nonprofits to see a summary of their fundraising events, making it important to have the Schedule completed accurately.

If you have any questions in regards to Schedule G of Form 990, please contact your Hawkins Ash CPAs representative.

|

|

Authors:

Briana Peters, CPA and Jeff Markwardt

Contact: 920.337.4549

|

|

Fundraising Event Considerations:

Part II

|

|

Quid Pro Quo

Quid pro quo in relation to special events is a payment of more than $75 that a donor makes to a charity that is part contribution and part purchase of goods or services. The best example of this is the purchase of a dinner ticket. A donor pays $100 for a ticket but the dinner is valued at $30. The tax deductible contribution part of the ticket is $70. This is considered a quid pro quo contribution.

The organization must provide the donor a disclosure statement because the donor’s payment is more than $75. Usually this statement is included on the dinner ticket. Although the deductible contribution is only $70, disclosure is required because the full payment made is more than $75. IRS imposes a penalty on an organization if this disclosure is not made. The penalty is $10 per contribution, not to exceed $5,000 per fundraising event or mailing.

Auction Items

It is important to develop a method for tracking auction items as they are collected. An inventory list can guard against theft of auction items, provide good records for sending donor acknowledgement letters, and provide a history of donors for future fundraising events. The list should include the following: item description, item value (if supplied by the donor), who gave the item, and who received the item. After the event, update the list with the amount received for each item during the auction. Proceeds on the list should be reconciled to the accounting records.

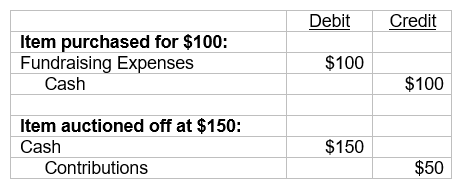

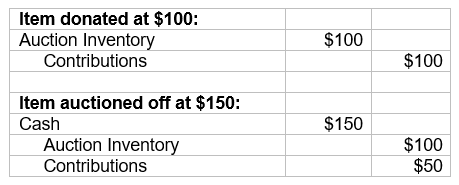

Accounting for auction items is commonly done incorrectly. This is the proper accounting for auction items under two different scenarios.

Scenario #1: Item was purchased by the organization.

|

|

Scenario #2: Item was donated to the organization for auction.

|

|

Scenario #2 is the preferred method for recording items donated for auction. Consider the size of your auction and how long items are held before deciding to switch to this method.

Raffles

Requirements for raffles vary by state. During the planning phase of your event, you should gather information on the license requirements, the types of raffles allowed, and who can participate. The license requirements for Wisconsin and Minnesota are as follows.

In Wisconsin, any organization conducting a raffle must obtain a license through the Division of Gaming’s Office of Charitable Gaming. There are two types of licenses – Class A and Class B. The Class A raffle license is needed when tickets are sold in advance and the day of the raffle. The Class B raffle license is needed when tickets are only sold the day of the raffle. Bucket raffles and 50/50 raffles are common examples of a Class B raffle. An organization conducting both Class A and Class B raffles must obtain both license types. Applications and more information can found at:

https://doa.wi.gov/Pages/LicensesHearings/RaffleLicense.aspx.

In Minnesota, an exemption from gambling activity such as raffles may be obtained from the Minnesota Gambling Control Board if the organization qualifies. An exempt permit is required when the following applies: 1) the total value of all prizes donated and purchased is less than $50,000 for the year, and 2) gambling activity is limited to five days during the year. An application for the exempt permit must be filed for each year. Organizations that don’t meet these two requirements must obtain a lawful gambling license. Applications and more information can found at:

https://mn.gov/gcb/raffles.html.

There are also federal requirements regarding raffles. If the organization generated over $15,000 in raffle and other gambling proceeds, it must complete Part III of Form 990, Schedule G. Revenue and expenses related to the raffles or other gambling activities are reported on this schedule. If a single donated prize is valued at more than $5,000, it must be reported on Schedule B of Form 990. Prize winners of cash or gifts valued at over $600 should be issued a 1099-MISC (included in Box 3). Also, winners from wagering activities that receive winnings over $600 should be issued a Form W-2G.

Other Items

Lastly, consider these other items when planning your next event:

- Creating a budget for event expenses

- Obtaining event insurance

- Obtaining a liquor license or event permit, if either are applicable

- Training volunteers before the event

- Reconciling revenue and expenses to supporting schedules and auction inventory listing

- Scheduling a debriefing meeting shortly after the event to discuss and make note of possible improvements

|

|

|

|

Author:

Lora Vandevoorde, CPA

Direct: 920.337.4528

|

|

DHS Audit Requirement Update

|

|

During 2017, Wisconsin State Statute 46.036 (4)( c ) and 49.34(4)( c ) were amended to increase the threshold for the requirement to provide a purchaser with a certified financial and compliance audit report from $25,000 to $100,000 for care and services purchased. Effective January 1, 2018, both the Department of Health Services (DHS Audit Guide) and the Department of Children and Families (Provider Agency Audit Guide) implemented this audit requirement increasing the threshold from $25,000 to $100,000. The increase to the audit threshold is in effect for contract periods that began on or after January 1, 2018.

|

|

|

|

Author:

Matt Neu, CPA

Direct: 920.684.2549

|

|

Client Feature and Executive Director Q&A

Home and Community Options

|

|

Home and Community Options (HCO) is a nonprofit organization that serves children and adults with developmental disabilities who are in need of residential and support services in order to live happily in Winona, MN, and area communities. Its mission is to help people with disabilities to become part of the community, providing engagement and personal growth opportunities.

HCO hosts an annual musical that serves as the nonprofit’s largest fundraiser and provides a way for individuals with developmental disabilities to become involved in the performing arts. Each year, the production raises nearly $100,000. HCO’s productions draw sell-out crowds and have the ability to pull in nearly 300 volunteers annually. It is estimated that these community volunteers donate $16,000 worth of volunteer hours each year.

This year’s production of

The Little Mermaid involved more individuals with disabilities than ever, and casted more than 90 people. While some were part of the cast, many individuals who HCO serves helped create the set and served as emcees, vending, and backstage help during the productions. This year marked HCO’s 21

st musical.

Funding for disability services often does not cover all the various needs of those the organization serves. Money raised from the annual musical assists HCO in providing accessible equipment, medications, or other basic necessities for its clients who otherwise wouldn’t receive these supports as a result of budget shortfalls.

|

|

Suzanne Horstman serves as the organization’s Executive Director. Suzie began her career with HCO while in college 27 years ago. After discovering a personal connection with the organization’s mission and values, she turned her part-time gig into her life’s work. She has served in various roles at HCO. She became Executive Director in 2013. We had a chance to talk with Suzie about being a nonprofit leader. Here’s what she had to say.

1. What are some things you know now that you wish you knew when you first started as a nonprofit leader? When I first started as an Executive Director, I didn’t realize the knowledge and support that other nonprofit leaders would offer me. We live in an amazing community and the nonprofit leaders have been a wonderful resource. I would definitely encourage new nonprofit leaders to start out their new role by reaching out and developing relationships with their nonprofit colleagues.

2. What has been you biggest source of pride as executive director? My greatest joy has been watching the individuals with developmental disabilities that we serve gain independence and confidence as they become strong self-advocates. What an amazing sight to see a previously shy individual speak to three of her legislators in a room filled with more than 40 constituents!

3. What are your three biggest accomplishments in your career as a nonprofit leader? I would never want to take credit away from the two previous executive directors or the amazing leadership team that really moves HCO forward. With that being said, three of the biggest accomplishments of HCO have been:

- Moving individuals out of institutions.

- Providing innovative solutions (such as using smart home technology) to support our individuals so they can become more independent.

- Providing opportunities for the individuals we serve to learn how to become strong self-advocates so they have a voice to change their world.

One of the most enjoyable parts of my career has been being a part of the HCO musicals.

4. What are the dominant challenges that you see nonprofit organizations facing, and what do you think would be viable solutions? For any health and human service agency in Minnesota, the biggest challenge is finding qualified employees with a limited available workforce. Securing nurses, social workers, and skilled direct care professionals is difficult with the current workforce shortage and unemployment at an all-time low. One solution that we have identified is reaching out to the ever-increasing number of retirees that are looking for a way to give back to the community. We believe that this population has a great deal to offer those we serve.

5. What aspects of nonprofit accounting do you find most challenging? Most of HCO’s funding comes from the state and federal government through Medicaid dollars. During the past month, we have seen a 7% reduction that will be passed on to providers. The most challenging part of our nonprofit accounting is the uncertainty of whether these funds will be available in the future.

6. How do you see the organization changing in the next two years, and how do you see yourself creating that change? As our main funding stream is going through significant changes and demographic research shows a continued decline in the workforce, we know that our agency will look very different two years from now. To maintain quality services for the individuals we support, we will need to continue to engage our community by offering opportunities for them to become more involved in the services that we provide.

More information about HCO and its annual musical can be found at www.HCO.org.

|

|

More Resources from CPA-HQ

|

|

Write Off Bad Debt in QuickBooks Online

Unfortunately, there may be a time when a customer does not pay you for your services and you need to write off their outstanding invoice.

|

|

Tax Reform Podcast

In these lively interviews, Jeff Dvorachek, CPA, provides guidance on the new tax laws to help businesses and individuals understand how their individual tax situation will be affected.

|

|

Defining Retirement Plan Compensation

Determining proper compensation for each participant is crucial to proper administration of any qualified retirement plan.

|

|

|

|

|

|

|