MONTH-2-MONTH is intended to provide you with updates on AFP and timely financial planning and investment information on a variety of topics.

If you find our content useful, please forward this e-mail to a friend.

|

|

November always brings cool, crisp air and memories of days gone by. It can provide a quiet moment between the back to school rush and the holiday rush. What are your plans for Thanksgiving? Will you be a hospitable host or a gracious guest? Remember to savor the company of friends and family as equally as the feast. If you do, you will be able to have your cake (or pie!) and eat it too! Happy Thanksgiving from our homes to yours!

|

|

|

- Teri, Tracey, and Maria attended the Orion Launch conference in Omaha, NE last week. The trip was worth the time away from the office. We had the opportunity to meet with program experts one-on-one, learning many efficiencies of the Orion program. The conference ended with a city block power outage, allowing us time to explore downtown Omaha.

- Sudden Money - The Sudden Money Annual Conference is attended by a small, but growing body of seasoned CFPs around the world looking to take financial planning to a more meaningful level. As a Certified Financial Transitionist® (CeFT®), Teri finds value in attending this conference. It helps to enhance our process when we are working with individuals and families going through significant life transitions.

- E-Money - Bob, Teri and Maria attended a one-day workshop in Cincinnati to sharpen our skills and knowledge of this software program. This is our main financial planning program and even though we have been using it for a few years, there are always more layers of complexity to explore and learn. The workshop was well worth the time and very insightful. It helped us identify areas that we should be utilizing to increase our efficiency and better communicate outcomes to our financial planning clients.

|

|

Tracey, Teri, and Maria in disguise at the Old Market in Omaha, NE.

|

|

FYI

- We have received some inquiries regarding the Morningstar Portal. The Morningstar Portal is no longer available due to the transition to Orion. We are working to launch the new Orion Client Portal for eligible clients in December. We apologize for any confusion and appreciate your patience. Watch for details in the coming weeks.

- News broke on 11/21/2019 regarding merger negotiations between Schwab and TD Ameritrade. No official public announcement has been made as of the time of distribution of this newsletter. Please stay tuned.

|

|

|

|

November is turning out to be a busy month! Very little on the personal side and a great deal of focus on work related items. Teri started the month by celebrating her birthday in Florida at the Sudden Money conference. As fun as this may sound, Teri would prefer to be with family vs. attending a conference, even though this is an amazing group of close financial planning friends. From this conference she went to Atlanta, GA for an all-day study session and to sit for the Accredited Investment Fiduciary (AIF) exam. This was the culmination of a year of study. She passed and this will now open some additional access to investment research she has been wanting to include in our investment management process. The following week Teri attended the Orion conference in Omaha, NE for new users with Tracey and Maria. This week Teri attended a one day program on our financial planning program with Bob and Maria in Cincinnati. Next week she is hoping to turn her attention to some quality time with friends and family.

|

|

|

|

|

Bob and Christine have had a good November. Bob attended his daughter Ashley’s annual Halloween/Pumpkin carving party early in November. The carved pumpkins were quite amazing! Christine spent a Sunday in London Correctional Institution cooking meals for Kairos Prison Ministry. She really enjoys it and finds it extremely rewarding.

Their fall yard clean up and final grass cutting got completed. Bob actually had to cut portions of the yard that still had snow. That was a first.

Bob & Christine plan on spending the morning of Thanksgiving in the Hocking Hills hiking with Ashley. Then off to a good Amish breakfast in Logan. The afternoon will most likely be spent recovering from the food coma. The only shopping they will do on Black Friday is getting their Christmas tree.

|

|

|

|

|

Weekends have been devoted to outdoor tasks demanded by home ownership and falling leaves. Andy enjoys hanging Christmas lights in advance of Thanksgiving and when weather presents an opportunity. He then powers them up as dusk falls on Thanksgiving.

A traditional Thanksgiving dinner is always served at home and we are happy to say that our independent, adult children are still able to attend. We maintain flexibility based upon their other commitments. Each year that this tradition continues, we share thanks by writing down what we are thankful for and placing notes in a special jar. After dinner, we read the notes and try to guess who wrote what. A good laugh is shared during this time. Then we have pie!

|

|

|

|

|

November was a busy month for Maria! Her sister got engaged, she ventured to Omaha with Tracey and Teri for the Orion Conference, and will be heading to a cabin in Hocking Hills with her family for Thanksgiving. Maria is extremely excited to celebrate her favorite holiday by eating turkey and mashed potatoes surrounded by family, and spending time hiking around Hocking Hills.

Maria will be applying for graduation in the spring at the end of November, and is looking forward to getting a little break from school before starting her final semester at Ohio Dominican University.

|

|

|

Current Economic and Investment Information

|

|

RECESSIONS - The last official recession in the United States lasted from the end of December 2007 to the end of June 2009, i.e., 18 months in duration. The official declaration that a recession was underway nationwide was made on 12/01/08 or 11 months after the recession began. The official declaration that the recession had ended was made on 9/20/10 or nearly 15 months after the recession’s official end date (source: National Bureau of Economic Research).

GLOBAL GROWTH -90% of the world’s economies are projected to grow more slowly in calendar year 2019 than they did in calendar year 2018. The US economy grew by +2.9% in 2018 and to date has grown by an annualized +2.3% in 2019(source: International Monetary Fund).

CONSUMER SPENDING TO ECONOMY - Consumer spending by Americans makes up an estimated 70% of our $21.5 trillion economy. Consumer spending by Chinese citizens makes up an estimated 40% of their $14.2 trillion economy (source: Department of Commerce).

FED & INTEREST RATES - The probability of a Fed rate cut following its 2-day meeting on December 10-11 is just 1% as of last Friday (11/15/19) after reaching a high of 66% in August 2019 (source: CME Group).

CAREERS - 30% of 1,019 working adults surveyed in September 2019 believe their career advancement has been stunted because “Baby Boomers” continue to work later in life and are delaying their retirement. “Baby Boomers” are the 78 million Americans born between 1946-1964 (source: LinkedIn).

NET WORTH - After adjusting for the impact of inflation, an average millennial in 2019 has a net worth 41% less than the net worth of a similarly aged adult 30 years earlier in 1989. Millennials were born between 1981-97 and are age 22-38 in 2019(source: Federal Reserve Bank of St. Louis).

ENERGY - The number of operating oil rigs in the United States fell to 806 as of last Friday 11/15/19, the 12th weekly decline in the last 13 weeks. The number of operating oil rigs in the United States was 1,083 as of the end of calendar year 2018 (source: Baker Hughes).

HEALTH INSURANCE - American private health insurance companies spend on average 12.2% of premiums collected on administrative costs, i.e., if the private health insurers pay out benefits of less than 87.8% of premiums, they will be profitable(source: Donald Berwick, Obama administration health care official).

HOUSEHOLDS - Of the 123 million households in the United States as of 9/30/19, an estimated 30 million are homeowners with no mortgage, 50 million are homeowners with a mortgage and 43 million are renters(source: Census Bureau).

STUDENT LOAN DEBT - Just 6% of the 45 million Americans that have student loans hold 33% of the nation’s $1.50 trillion of outstanding student loans. This group is comprised of borrowers with at least $100,000 of outstanding student loan debt (source: Brookings Institute).

HOMELESS - 23.5% of the homeless population in the United States live in California(source: U.S. Department of Housing and Urban Development).

|

|

Cause for Alarm?

By Bob Veres

Inside Information

|

|

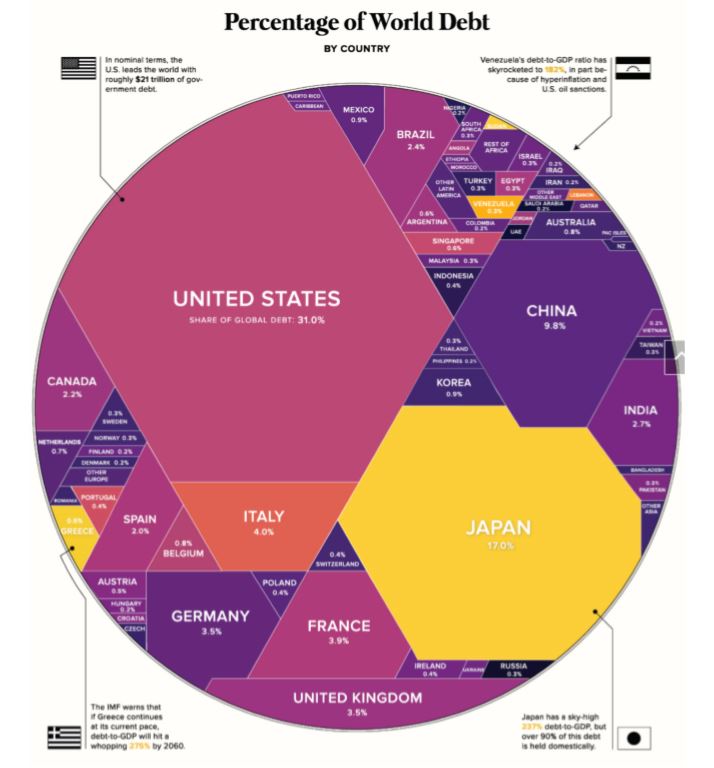

Global government debt is growing. Twenty years ago, the estimate for government debt for all countries was estimated to be around $20 trillion. Today, that number has ballooned to $69.3 trillion, and we are now at the highest debt-to-GDP ratio in human history: 81.8%.

You can see from the graphic which countries have the highest debt—and of course, the U.S. leads the way in this dubious statistic, with $21.5 trillion, and a debt-to-GDP ratio (dividing how much the country owes its bondholders by the total amount of economic activity in a recent year) over 100%. The graphic is also color-coded to show the countries that seem to be in a danger zone as far as their ability to repay what they’ve borrowed. Japan leads the world with a 237.1% debt-to-GDP ratio, but Greece, Venezuela and the Sudan are not far behind. Italy’s debt levels are also worrisome; the debt-to-GDP ratio there is 132.2%.

At the other end of the spectrum, you have the Republic of Korea, with just 0.9% of all the world’s government debt, and a debt-to-GDP ratio of a comfortable 37.9%, better than Australia (41.4%), China (50.6%) or Mexico (53.6%).

The first thing you think when you see those figures is that the world may be coming to an end. But surprisingly, most global economists are not worried by the growing levels of government debt. When you add the government debt to private debt around the world, the total borrowing reaches $164 trillion, a figure calculated by the International Monetary Fund. But the IMF’s most recent warning, in issuing those figures, was that high levels of debt might make it harder for the world economy to climb out of a recession, but that trade wars and protectionism are currently the greatest threat to global growth.

The most likely scenario: higher taxes in the future to pay down what has become a (long-term) unsustainable debt load, not just in the U.S., but in the other high-debt countries as well.

|

|

New Limits & Rates for Calendar Year 2020

|

|

’Tis the season for the U.S. Internal Revenue Service to make its annual Cost-of-Living Adjusted Limits for 2020. Here are a few inflation adjustments that may impact your planning decisions moving into 2020.

Social Security

•

For Individuals receiving benefits - The Social Security Administration announced a 1.6%

cost-of-living adjustment for

2020, meaning the average retiree will get $24 more each month, or about $1,503. In 2019, the

COLA was 2.8%, an

increase of about $40 a month for retirees.

•

For Individuals paying into Social Security - The maximum amount of earnings subject to the Social Security tax (taxable maximum) will

increase to $137,700.

Estate & Gifting

Not that this change will impact too many individuals, they have increased the federal estate tax limits for 2020 to a total of

$11.58 million—up from $11.4 million in 2019. There is no change in the annual gift tax exclusion from 2019. The amount you can give to heirs each year without reporting a gift—remains at

$15,000 for 2020.

Retirement Plan Contributions

•The IRS also lifted the annual limit that can be contributed to a defined contribution plan

(401(k), 403-B, 457 or similar plan) from $19,000 to

$19,500.

- For people 50 or older, they can make an additional catch-up contributions of $6,500—up from 2019’s $6,000. Therefore, if you are over 50, the maximum contribution for 2020 is $26,000, up from $25,000 in 2019.

- If you are under 50, the maximum contribution for 2020 is $19,500.

•The amount you can contribute to an

Individual Retirement Account (IRA) is unchanged at

$6,000, with a

$1,000 catchup limit for people 50 and older. This includes traditional IRAs and Roth IRAs.

- For people 50 or older, $7,000.

If you are under 50, $6,000.

•The limitation under § 408(p)(2)(E) regarding SIMPLE retirement accounts is increased from $13,000 to

$13,500.

•If an employer allows after-tax contributions, or if you’re self-employed, the overall defined contribution plan limit was raised from $56,000 to

$57,000.

The IRS also changed the tax brackets for working Americans, raising slightly the thresholds for the 10%, 12%, 22%, 24%, 32%, 35% and 37% rates, and raised the standard deduction to $12,400 for individuals and to $24,800 for married people filing jointly in 2020.

Sources:

|

|

How to Use the HSA, for Medical or Retirement Savings

By Julia Carpenter

The Wall Street Journal

|

|

The health savings account, or HSA, can be a powerful savings tool—if you approach it the right way.

These accounts, which Congress authorized in 2003, are more than just a simple savings tool for medical emergencies. Retirement planners laud the HSA’s triple tax advantage and its use as a complementary savings vehicle to 401(k) plans.

Oftentimes when people first hear of HSAs, it is during this time of year. For companies with policies that start in January, open enrollment typically happens in the fall. During this period, many employees are already stressed about choosing and selecting other benefits.

“I don’t think most people understand HSAs from the get-go,” said Roy Ramthun, a consultant who specializes in HSAs. “From my experience, the HSA gets 30 seconds of the health benefit presentation. It’s all about the insurance, and then ‘Oh, you have this.’”

HSAs are unique in the triple tax advantage they offer: If you opt for a high deductible health plan, you can contribute to an HSA by setting aside pretax earnings without paying federal or state income tax. From there, that money can be invested and grows tax-free. Additionally, if used for medical expenses, this money can be withdrawn tax-free before retirement, which can’t be done with a 401(k) or an individual retirement account.

Eric Remjeske , president of Devenir Group LLC, said since Congress authorized these accounts in 2003, the number of accounts and the average account balance have both grown over time. By 2011, there were 6.2 million HSAs, according to Devenir Research; this past June, that number had grown to 26.3 million.

More money is flowing into HSAs every year. Devenir Research data show that $43.5 billion was deposited in HSAs in 2018, with $10.2 billion invested, a sharp increase from the year before when $31.5 billion was deposited and $5.5 billion invested. By 2021, Devenir estimates that number will rise to $67 billion deposited with $21.2 billion invested.

While the 401(k) remains the predominant retirement savings vehicle, Mr. Ramthun recommends contributing to both a 401(k) and HSA, especially if your employer offers a match for either.

“Advisers are now asking the question: Where do you put the money, 401(k) or HSA?” said Steve Christenson, executive vice president at Ascensus, a retirement and college savings service provider. “They’re seeing more of a balance amongst consumers.”

To make the most of both, research if your employer offers matches. If your employer also offers an HSA match, Mr. Ramthun recommends prioritizing that contribution, as you’ll eventually be able to reap greater benefits from the HSA’s triple tax advantages. From there, contribute to your 401(k), and if your employer also offers a match there and you’re taking advantage of it, you’ll be benefiting from both savings plans.

The HSA contribution limits for 2020 are $3,550 for an individual with a high deductible health plan and $7,100 for an individual with family coverage. The catch-up contribution amount for those 55 years old or above is an additional $1,000. The amount contributed to an HSA doesn’t affect the contribution limits for 401(k) plans or IRAs, which are $19,500 and $6,000 respectively for 2020.

One approach to the HSA is to consider paying for current medical expenses out-of-pocket after establishing the HSA; you can then file for reimbursement in retirement. This way, you can supplement your retirement income—entirely tax-free.

If you’re taking this approach, you should make sure you invest your HSA balance in a diversified portfolio, so you can maximize its potential return. According to 2019 data from Ascensus, less than a third of HSA account holders eligible to invest their funds actually did so.

Meanwhile, keep track of the medical expenses you pay out of pocket. Keeping these receipts on hand means you can then file during retirement to have them reimbursed. But remember: You have to keep the receipts from any medical expenses you paid for out-of-pocket before retirement, just in case the IRS ever comes knocking for an audit.

An HSA can also be considered as a “rainy day” medical fund that works in tandem with your 401(k) to help offset the cost of out-of-network care, over-the-counter medicines or other things your insurance may not cover. Even if you’re healthy now, studies show you could still be spending much more on medical expenses once you enter retirement.

Remember: You can’t keep contributing to your HSA once you’re enrolled in Medicare. So maximizing contributions now will allow the miracle of compounding to work, growing that money in your HSA over time.

“Everything about retirement planning says, ‘Start young, be regular and invest,’” Mr. Ramthun said. “That’s what we want people to hear about HSAs.”

|

|

There were a Lot of HSA Questions.

Here Are Some Answers.

A growing number of people are letting their health savings accounts grow

tax-free for retirement

By Anne Tergesen & Julia Carpenter

The Wall Street Journal

|

|

Health savings accounts, or HSAs, allow individuals to set aside money in tax-advantaged accounts to pay for medical expenses tax-free.

While many use the money they contribute to these accounts to cover current medical bills, a growing number are paying those bills out-of-pocket to let their HSAs grow tax-free for retirement, when medical costs can be high.

Following our recent article on HSAs, we received dozens of questions from readers. Here are responses.

The HSA vs. the 401(k)

What are the tax advantages of HSAs, and when do you risk losing them?

With an HSA, you can generally contribute money without paying federal or state income or payroll taxes. The money grows tax-free and, if used for medical expenses, can be withdrawn tax-free. With a traditional 401(k) or IRA, in contrast, withdrawals are subject to income tax.

Some states don’t honor all the HSA’s tax advantages. For California and New Jersey residents, contributions aren’t deductible from state income taxes. New Hampshire and Tennessee may tax some earnings.

You can use your HSA for nonmedical expenses, but you will owe income tax on those withdrawals—and a 20% penalty if you are younger than 65.

The Fine Print

Are HSAs available only to those in high-deductible plans?

Yes. But “not all high deductible plans are HSA-qualified,” said Roy Ramthun, a consultant who specializes in high-deductible plans and HSAs. He recommends asking your employer or insurer.

What qualified medical expenses can I use my HSA money for?

To withdraw money tax-free from an HSA, you have to use it for qualified expenses incurred by you or your spouse or dependents. Those can include not just medical bills but also dental and vision-care expenses and premiums under Cobra and for all types of Medicare coverage (except Medigap). It also includes a portion of long-term-care insurance premiums and over-the-counter medications you have a prescription for. To check on allowed expenses, see IRS Publication 502.

Can retirees contribute to an HSA before they qualify for Medicare?

If you have an HSA-qualified high deductible health plan, you can contribute to an HSA whether you are working or not, Mr. Ramthun said. (Be sure your spouse doesn’t have an account, such as a flexible-spending account, or FSA, that might disqualify you from contributing to an HSA.)

Do medical expenses have to be reimbursed in the year they are incurred?

No. The biggest payoff with an HSA comes when the money isn’t used for current medical bills and instead compounds over time.

HSA owners with receipts for unreimbursed medical expenses can tap their accounts tax-free— up to the total on the receipts—to supplement income in years in which taking withdrawals from other accounts would push them into a higher tax bracket or expose them to higher Medicare premiums.

Do I have to save my receipts?

If the Internal Revenue Service audits you, you will need receipts to prove HSA withdrawals covered medical expenses. Without proof, the IRS may impose income tax on distributions— and a 20% penalty if you are younger than 65.

Can you reimburse yourself from an HSA for medical expenditures that were deducted on a tax return?

No. “That’s double dipping,” said Ed Slott, an IRA specialist who runs his own consulting company in Rockville Centre, N.Y.

Managing the Account

Our bank doesn’t offer investment options. Can you provide a list of companies that do?

If you don’t like your options, you can transfer your HSA’s balance tax-free to a new account. Morningstar’s 2019 report on HSAs and Devenir Group LLC’s hsasearch.com can help you research offerings. Most HSAs impose account maintenance fees. (Some employers cover them.) Account owners must also pay mutual-fund expenses, so shop for low cost options.

How do I transfer an HSA from a former job?

If you leave a job, you can leave your HSA behind. If you want to continue to contribute, you can do so on an after-tax basis and claim a deduction on your tax returns. But if your new employer makes a contribution to its workers’ HSAs or you want to make pretax payroll contributions, you’ll have to establish a new account.

Transferring money from an old to a new HSA can make sense if you want to keep all the money in one place or the new account’s fees or investment options are better. Contact the administrators of the old and new accounts and set up a “trustee-to-trustee transfer.”

How do I track down an HSA from former job?

First, search for statements or try to access the account online. If that doesn’t work, contact your former employer to find the administrator it used or check your past tax returns for either a 1099-SA or a 5498-SA.

With HSAs, whatever is left at year-end is retained by the account owner. But this has never been the case for me. What am I missing?

You may have had either an FSA or a health reimbursement account (HRA), but not an HSA. As with an HSA, the FSA allows you to contribute pretax money for health-care expenses. But you generally have to spend the money by a set annual deadline or forfeit the remaining balance. (Some employers allow workers to carry over as much as $500 from one year to the next.) With an HRA, the employer is the account owner and decides whether employees can roll money over from year to year or take the account with them when they leave.

For All the Couples Out There Can one spouse choose a high deductible plan with an HSA while the other selects conventional coverage?

Yes, but it’s important to “make sure the two plans don’t create a conflict that disqualifies” the spouse with the HSA from contributing to it, Mr. Ramthun said. That can happen if one spouse has conventional coverage that covers the other spouse or signs up for an FSA or HRA. Like an HSA, both offer tax benefits.

“If I have an HSA and my spouse signs up at her job for an FSA, in virtually 100% of the cases, that FSA is going to cancel the whole family’s HSA eligibility,” said Mr. Ramthun. Why? “The IRS assumes the FSA is available to all family members unless the employer’s plan documents specifically state otherwise.”

Is $7,100 the total a household can contribute next year?

For 2020, the annual contribution limit to an HSA is $3,550 for individuals and $7,100 for a family. People age 55 or older are permitted to kick in an extra $1,000 each.

For dual-income households, dividing the family’s $7,100 contribution limit can be complicated. If both spouses have individual insurance coverage at work, each must set up and fund a separate HSA, up to the $3,550 limit, Mr. Ramthun said.

However, if one spouse has family coverage, that person can contribute up to $7,100, even if the second spouse has separate HSA-eligible health insurance. (The second spouse must refrain from making HSA contributions that take the family above the $7,100 limit.)

What if my spouse and I have an HSA and divorce?

HSAs are similar to IRAs in that there can only be one account holder. Depending on the divorce agreement, the assets in each former spouse’s HSA could potentially be divided. “That’s up to the court or whoever is handling the divorce,” Mr. Ramthun said.

Can beneficiaries inherit an HSA tax-free?

If you name your spouse as your HSA beneficiary, he or she can inherit the account tax-free. If your beneficiary isn’t your spouse, he or she may have to pay income tax on the account’s value as of the date of death, said Sarah Brenner, director of retirement education at Ed Slott & Co. Within a year of death, the beneficiary should claim tax-free reimbursement from the account for any unreimbursed medical bills the account owner accrued, Ms. Brenner said. That will reduce the balance the beneficiary must pay tax on.

|

|

"Gratitude can transform common days into thanksgivings, turn routine jobs into joy,

and change ordinary opportunities into blessings."

- William Arthur Ward

|

|

|

|

Alexander Financial Planning

|

1621 W. First Avenue

Grandview Heights, OH 43212

614-538-1600

Registered Investment Advisor

|

|

|

This material is distributed by Alexander Financial Planning, Inc., (AFPI) and is for information purposes only. Although information has been obtained from sources to be reliable, we do not guarantee its accuracy. It is provided with the understanding that no fiduciary relationship exists because of this report. Opinions expressed in this report are not necessarily the opinions of AFPI and are subject to change without notice. AFPI assumes no liability for the interpretation or use of this report. Financial planning, investment conclusions and strategies suggested in this report may not be suitable for all investors and consultation with a qualified advisor is recommended prior to executing any investment strategy. All rights reserved.

|

|

© Alexander Financial Planning, Inc.

|

|

|

|

|

|

|

|