June 24, 2022

Please always note the dates of the articles in the options commentary stream that follows this article. We hope you find this format helpful. Performance is hypothetical and no trading is taking place.

By The Valuentum Team

Hi everyone:

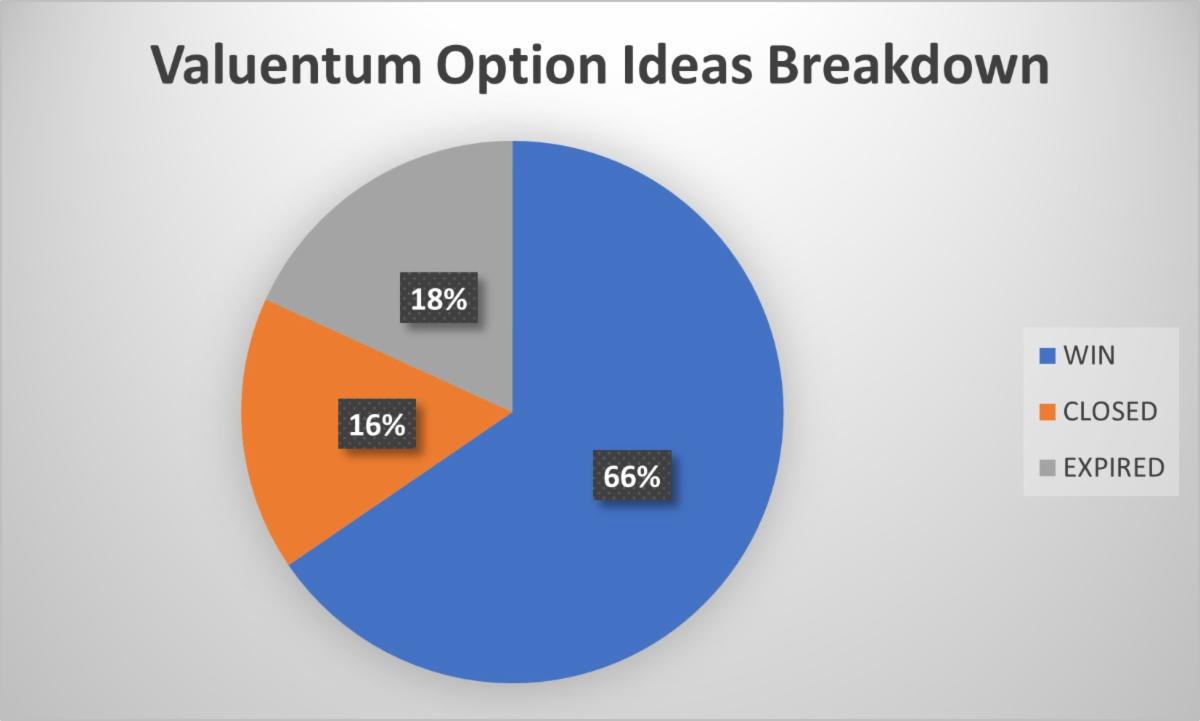

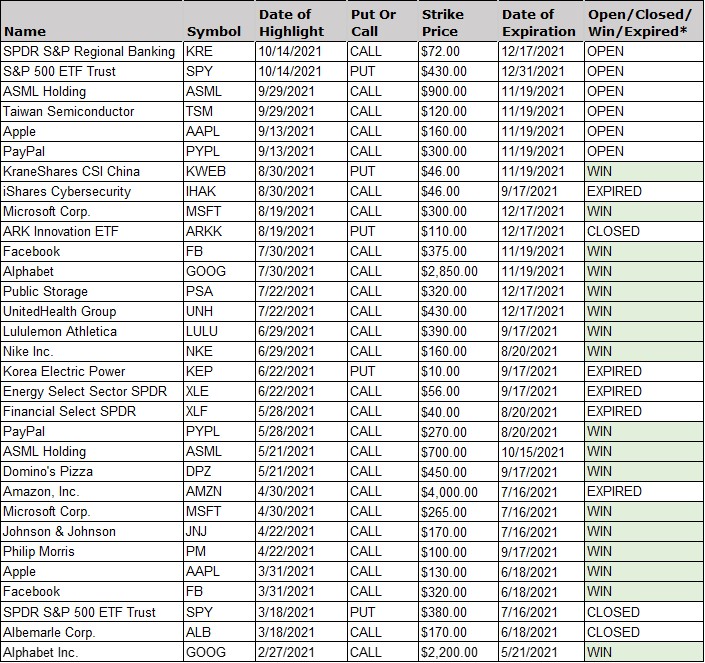

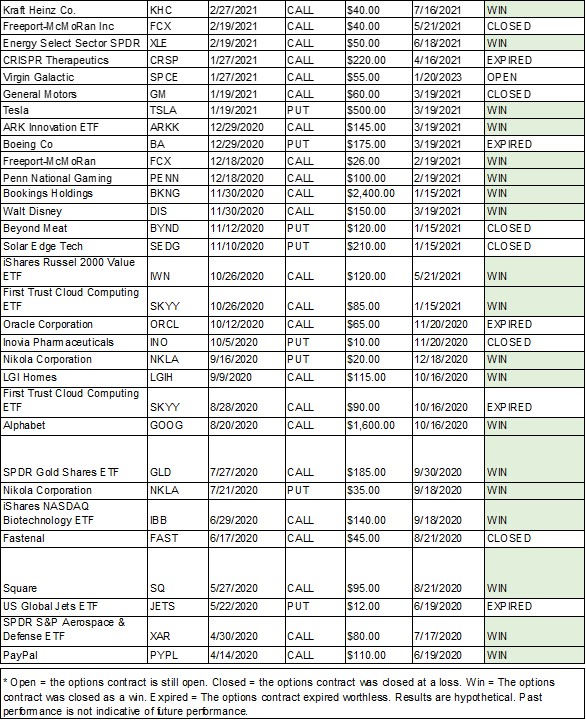

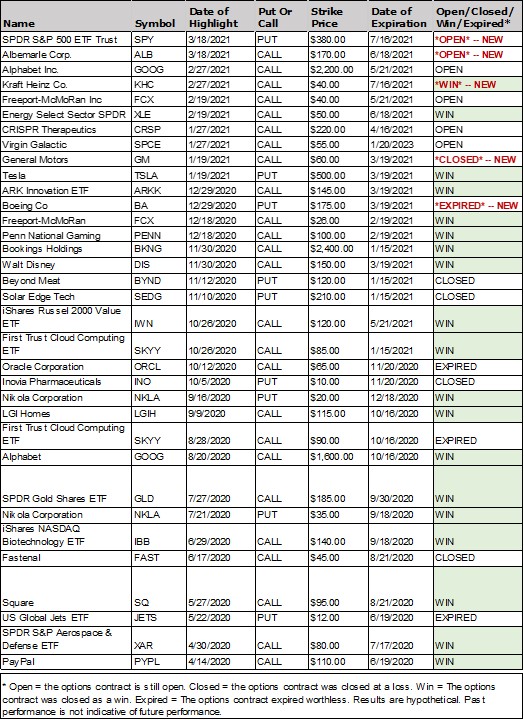

With the half year mark to 2022 nearing, we wanted to provide an update on "performance" tracking across a variety of our publications. In case you missed them, please find the year-to-date evaluations of the simulated Best Ideas Newsletter portfolio, the Exclusive capital appreciation and short idea considerations, as well as the simulated High Yield Dividend Newsletter portfolio for your convenience.

We've also updated the "performance" tracking of the options ideas generation for your review in the table above, and we'll be releasing "results-oriented" commentary on the simulated Dividend Growth Newsletter portfolio and ESG Newsletter portfolio in the coming days.

Today, we're releasing the first two options ideas for the month of June 2022 and closing the April 2022 put idea Tesla (TSLA) for a very nice "win." Based on data from YahooFinance, the bid/ask spread upon opening of the Tesla puts in April was $99.35/$101.10; today the bid ask spread is $150.45/$152.55, good for a near-50% hypothetical "gain." We're very pleased with this "winner."

|

|

Image Shown: Shares of Vertex Pharmaceuticals Inc (blue line) have been on a powerful upward climb year-to-date and we are huge fans of the biotech firm. Pivoting to the Health Care Select Sector SPDR Fund ETF (orange line), shares of the XLV ETF have significantly outperformed the S&P 500 on a price-only basis year-to-date. We view the capital appreciation upside of both Vertex Pharma and the XLV ETF quite favorably.

With that said, we’re highlighting the first and second options ideas for the month of June 2022. The first is long call options on Vertex Pharmaceuticals Inc (VRTX) with a $310 strike price that expire October 21, 2022. We caution that while these options have seen significant trading activity of late, relatively speaking, there is a large bid-ask spread and liquidity concerns could potentially arise in the future.

Vertex Pharma is one of our favorite biotech firms as its portfolio of treatments for cystic fibrosis (‘CF’), which have been approved by regulators across the world, generate substantial cash flows that the company utilizes to invest in innovative new medications. That includes a potential non-opioid pain treatment (the NaV1.8 inhibitor VX-548) which is currently undergoing clinical trials. Additionally, Vertex Pharma and its partners are pursuing several gene editing therapies via cutting edge CRISPR technologies that we covered in detail in this August 2021 article (link here).

Beyond Vertex Pharma’s stellar drug development pipeline, which we appreciate, the biotech firm is also a cash flow generating powerhouse courtesy of its CF drug portfolio. From 2019-2021, the firm’s average annual free cash flows came in at ~$2.3 billion. The company does not pay out a common dividend at this time though it has historically repurchased a meaningful amount of its stock, a capital allocation policy management intends to continue going forward after approving a $1.5 billion buyback program in June 2021 that lasts through December 2022.

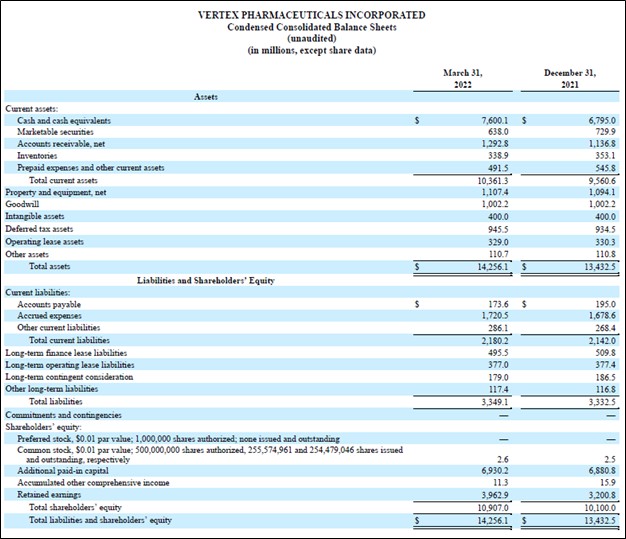

Furthermore, Vertex Pharma has a pristine balance sheet. At the end of March 2022, the firm had $8.2 billion in cash, cash equivalents, and current marketable securities on hand with no short-term debt and $0.5 billion in noncurrent finance lease liabilities on the books. The rock-solid financial position provides Vertex Pharma with ample firepower to repurchase “gobs” of its stock while still being able to invest heavily in the business.

|

|

Image Shown: Vertex Pharma has a fortress-like balance sheet. Image Source: Vertex Pharma – 10-Q SEC filing covering the First Quarter of 2022

Vertex Pharma’s GAAP revenues were up 22% year-over-year, and its GAAP operating income was up 17% year-over-year in the first quarter of this year due to strong demand for its CF portfolio and its pricing power, though the biotech company has been steadily stepping up its investments in the business to commercialize its drug development pipeline. Its potential VX-147 treatment for APOL1-mediated kidney disease is the farthest along the clinical trial process and we have been monitoring events closely on this front.

Our fair value estimate for Vertex Pharma currently stands at $271 per share though please note that the top end of our fair value estimate range sits at $366 per share. Additionally, we are currently in the process of updating our coverage of the health care sector, and there is a very good chance Vertex Pharma’s fair value estimate, and the top end of its fair value estimate range, will get revised higher.

Shares of VRTX have been on a powerful upward climb of late after rising ~26% year-to-date as of this writing. We view Vertex Pharma’s capital appreciation upside potential quite favorably. To read more about Vertex Pharma, please check out our June 2022 article covering our latest thoughts on the biotech firm (link here).

Pivoting to our second options idea for the month of June 2022, we are highlighting long call options on the Health Care Select Sector SPDR Fund ETF (XLV) with a $132 strike price that expire December 16, 2022. We will stress here that while these options have seen significant trading activity of late and the bid-ask spread is moderate but not reasonable, liquidity concerns could arise in the future should market activity shift elsewhere.

We have consistently stated that our view on the U.S. economy, keeping myriad headwinds in mind, is bullish. As things stand today, U.S. GDP in real terms will likely post positive growth in 2022. With that in mind, during times of economic turbulence, the health care sector is an attractive place to look for high-quality ideas with strong economic moats (patented drug portfolios represented by essential therapeutics) and stellar cash flow generating abilities. On a price-only basis, the XLV ETF is down ~9% year-to-date while the S&P 500 (SPY) is down ~21% year-to-date as of this writing.

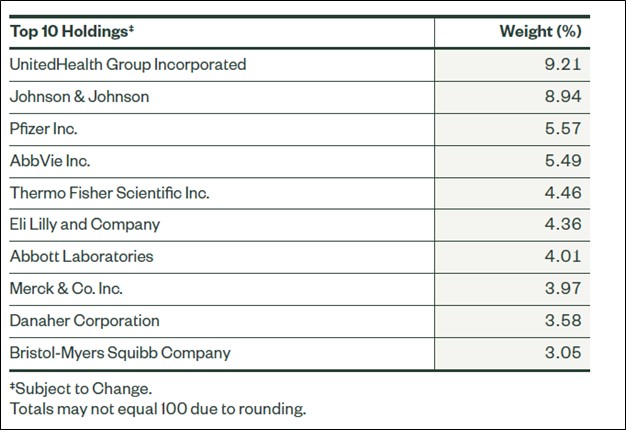

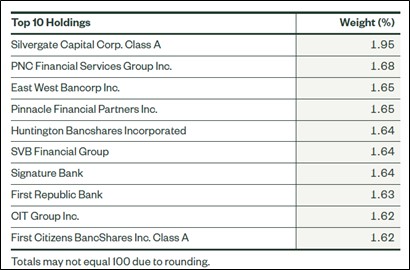

The top ten holdings within the XLV ETF as of the end of March 2022 can be viewed in the upcoming graphic down below. Please note that the top two holdings, UnitedHealth Group Inc (UNH) and Johnson & Johnson (JNJ), are two of our favorite ideas in the health care sector and represented ~18% of the XLV ETF’s total holdings at the end of the first quarter of this year. Additionally, the XLV ETF also had a modest amount of exposure to Vertex Pharma as of June 22, 2022.

|

|

Image Shown: The XLV ETF has a meaningful amount of exposure to our favorite ideas within the health care sector. Image Source: XLV ETF – Website

Recently, the “panic selling” seen in U.S. equity markets has started to calm down and trading activity appears to be stabilizing. There is ample room for capital appreciation upside potential in the health care sector, and the XLV ETF is a solid way to capitalize on that. We hope you enjoy the two new options idea considerations for the month of June 2022, as well as our latest "performance" update in table format. We're available for any questions, and thank you for your membership to our additional options commentary.

Please always note the dates of the articles in the options commentary stream that follows this article.

Always our very best,

The Valuentum Team

www.valuentum.com

Please note that with options trading, investors can lose their entire premium. Don't ever trade with money that you can't afford to lose. Valuentum is an investment research publisher and accepts no liability for how readers may choose to utilize the content. By continuing with your additional options commentary membership, you accept our Terms and Conditions. If you do not agree with the Terms and Conditions, you must stop using this service and cancel your additional options commentary membership.

|

|

May 27, 2022

Please always note the dates of the articles in the options commentary stream that follows this article. We hope you find this format helpful. Performance is hypothetical and no trading is taking place.

Good morning everyone!

Today, we’re highlighting the second set of options ideas for the month of May. We think the markets may be getting back on track as investors grow more comfortable with expectations regarding the trajectory of interest rates, inflation, and the global economy. In case you missed our latest take on the markets, it can be accessed here.

What this means, in our view, is that the markets may be due for a huge rally, and one of the best ways to trade around this theme for risk-seeking traders is via long calls on ultra-leveraged long ETFs. Though these are very, very risky and “wasting” assets—volatility generally erodes their price over long periods of time—for short-term traders, opportunities can sometimes present themselves, and these ultra-risky ETFs may offer a positive risk/reward at this time.

Again, it’s worth reiterating, the third and fourth option ideas for the month of May are very speculative ones and only may be considerations for the ultra-aggressive trader that is willing to take tremendous risks. Warren Buffett has noted in the past that derivatives are “financial weapons of mass destruction,” so derivatives on ultra-leveraged ETFs means that extreme caution with these financial instruments should be in order.

With that said, our third option idea consideration for the month of May is long call options on the ProShares UltraPro S&P500 (UPRO) with a strike price of $47.50 and expiration date of June 17, 2022. Along the same lines, our fourth option idea consideration for the month of May is long call options on the ProShares Ultra Dow30 (DDM) with a strike price of $66 and an expiration date of June 17, 2022. Interested readers should watch the price of these options contracts like a hawk, as they are sure to be volatile as the market whipsaws and as their expiration date nears.

In our latest market update to investors, we noted that market pessimism has seemed to have reached extreme levels by some measures, and we’re thinking this may present a near-term opportunity for the ultra-speculative options trader that is willing to take big risks. Options on ultra-leveraged ETFs are definitely not for everyone, but we think long call options on the UPRO and the DDM could make sense from a risk/reward standpoint at this time. Once again, please be careful dabbling with “financial weapons of mass destruction” on ultra-leveraged investment vehicles.

We’re available for any questions and have a wonderful Memorial Day Weekend!

Please always note the dates of the articles in the options commentary stream that follows this article.

Always our very best,

The Valuentum Team

www.valuentum.com

Please note that with options trading, investors can lose their entire premium. Don't ever trade with money that you can't afford to lose. Valuentum is an investment research publisher and accepts no liability for how readers may choose to utilize the content. By continuing with your additional options commentary membership, you accept our Terms and Conditions. If you do not agree with the Terms and Conditions, you must stop using this service and cancel your additional options commentary membership.

|

|

Image Shown: Shares of Netflix Inc (blue line) have performed poorly during the past three months, and we see some room for downside in the near term. On the other hand, shares of Paramount Global (orange line) have been on a nice upward climb of late, and we view its near term capital appreciation upside potential quite favorably.

May 25, 2022

Please always note the dates of the articles in the options commentary stream that follows this article. We hope you find this format helpful. Performance is hypothetical and no trading is taking place.

Dear members:

In case you missed our prior email today, it can be accessed here.

Today, we're highlighting the first and second options ideas for the month of May 2022. The first is long put options on Netflix Inc (NFLX) with a $180 strike price that expire September 16, 2022. Shares of Netflix have been pummeled since April 19, when the video streaming firm posted its first-quarter 2022 earnings report that saw its global paid subscribers drop by 0.2 million on a sequential basis.

Even worse, Netflix guided for its global paid subscriber base to drop by another 2 million on a sequential basis in the second quarter of this year. After years and years of strong paid subscriber growth, Netflix's growth is now slowing as many of its core markets mature while the firm contends with rising competitive threats. The company’s operating income and operating margin are also expected to shift lower this quarter on a sequential basis as its revenue growth slows, even as the need to invest heavily in original content remains. Netflix has responded by attempting to keep a lid on original content investments, where possible, while also rationalizing the size of its workforce.

|

|

Image Shown: Netflix’s guidance for the second quarter of 2022 was incredibly weak, which saw shares of NFLX tank on the news. Image Source: Netflix – First Quarter of 2022 Letter to Shareholders

Historically, Netflix’s cash flow performance has been inconsistent (it generated negative free cash flows in 2019 and 2021, and positive free cash flows in 2020). The firm exited March 2022 with a net debt load of $8.5 billion with no short-term debt on the books (though it has ample liquidity with $6.0 billion in cash and cash equivalents on hand at the end of this period). The company has its work cut out for it, however, as it attempts to limit “password sharing” activities in a bid to grow its paid subscriber base.

Though we generally like the area of large cap growth in the long run, ongoing pressure on shares of NFLX may be probable in the coming months, in our view, as management attempts to right the ship and investors continue to evaluate their thesis on the company. NFLX may ebb and flow with the market, but shares may find it difficult to establish any meaningful and sustained upward momentum until management can get things back on track.

Our second options idea for May 2022 is long call options on Paramount Global (PARA) with a $35 strike price that expire September 16, 2022. Paramount is pushing into the video streaming space with its Paramount+ and Pluto TV services, and the company also stands to benefit from households returning to the movie theaters in droves as the worst of the coronavirus (‘COVID-19’) pandemic fades. The company’s next big movie is Top Gun Maverick, a sequel to the popular 1986 flick Top Gun.

In the first quarter of 2022, Paramount+ added 6.8 million subscribers, which brought its total subscriber base up to ~40 million. Paramount+ is a paid video streaming service while Pluto TV is a free ad-supported video streaming service. Both have performed well of late, though the level of success that Paramount+ is able to achieve will have a larger impact on the company’s financial performance.

Paramount had a net debt load of $11.5 billion at the end of March 2022 (inclusive of a negligible amount of short-term debt), which is a concern, though its $5.3 billion in cash and cash equivalents on hand provides it with ample liquidity to continue scaling up the business. Unlike Netflix, Paramount is a consistent cash flow generator. From 2019-2021, Paramount generated ~$1.2 billion in free cash flow per year on average, making managing its net debt load while investing in original content and expanding its video streaming services an easier task financially.

Furthermore, a recent SEC filing noted that Warren Buffett’s Berkshire Hathaway Inc (BRK.A) (BRK.B) had taken a sizable equity stake in Paramount. We are inclined to agree with Berkshire Hathaway on this front and view Paramount’s near-term capital appreciation upside quite favorably.

Please let us know if you have any questions.

Please always note the dates of the articles in the options commentary stream that follows this article.

Always our very best,

The Valuentum Team

www.valuentum.com

Please note that with options trading, investors can lose their entire premium. Don't ever trade with money that you can't afford to lose. Valuentum is an investment research publisher and accepts no liability for how readers may choose to utilize the content. By continuing with your additional options commentary membership, you accept our Terms and Conditions. If you do not agree with the Terms and Conditions, you must stop using this service and cancel your additional options commentary membership.

|

|

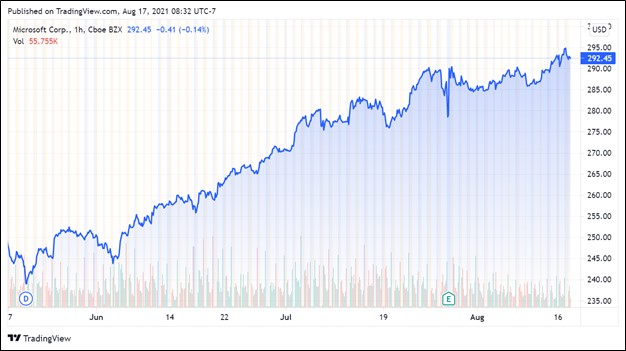

Image Shown: Shares of Microsoft Corporation (blue line) have regained their upward momentum over the past week while shares of Tesla Inc (orange line) have seen their technical performance deteriorate significantly of late.

April 29, 2022

Please always note the dates of the articles in the options commentary stream that follows this article. We hope you find this format helpful. Performance is hypothetical and no trading is taking place.

Dear members:

Today, we're highlighting our third and fourth options ideas for the month of April 2022. The first is long call options on Microsoft Corporation (MSFT) with a $300 strike price that expire August 19, 2022. On April 26, the tech giant put up a rock-solid earnings report for the period ended March 31, 2022, which beat both consensus top- and bottom-line estimates. During the related earnings call, management issued favorable guidance for the final quarter of Microsoft’s current fiscal year and guided for the company’s strong performance to continue into fiscal 2023.

Microsoft’s cloud-oriented operations remained a bright spot last fiscal quarter, which helped drive its GAAP revenues 18% higher on a year-over-year basis, while its significant pricing power helped the firm stay ahead of inflationary pressures. The company’s GAAP operating margin was up almost 40 basis points year-over-year last fiscal quarter, reaching ~41.3%, while its GAAP operating income climbed higher 19% year-over-year. Microsoft generated $47.4 billion in free cash flow during the first three quarters of fiscal 2022 and exited March 2022 with a $54.8 billion net cash position (inclusive of short-term debt).

We covered Microsoft’s latest earnings update and outlook in our April 27 article Microsoft Soars, Strong Revenue Growth Continues Unabated, which we strongly encourage our members to check out (link here). Here is a key excerpt from that article (the following four paragraphs):

[During Microsoft’s fiscal third quarter earnings call, management issued favorable guidance for the company’s fiscal fourth quarter performance. More importantly, Microsoft communicated to investors that its growth story should continue in earnest heading into fiscal 2023 (emphasis added):

“With that context in place, let’s turn to our Q4 outlook. In our largest quarter of the year, we expect our differentiated market position, customer demand across the solution portfolio, and consistent execution to drive another strong quarter of revenue growth. In commercial bookings, a growing Q4 expiry base, strong execution across our core annuity sales motions, and increased commitment to our platform should drive healthy growth against a strong prior year comparable…

We expect to close FY22, even in a more complex macro environment, with the same consistency we have delivered throughout the year. With strong revenue growth, share gains, and improved operating margins as we invest in the areas that are key to sustaining that growth. As we look toward FY23, our track record of delivering high value to our customers across many diverse and durable growth markets gives us confidence that we will drive continued healthy double-digit revenue and operating income growth.” --- Amy Hood, CFO of Microsoft

We appreciate that Microsoft has been and expects to continue firing on all cylinders.]

Our fair value estimate for shares of MSFT, under valuation assumptions we deem reasonable, sits at ~$330 per share, which is well above where Microsoft’s stock price is trading at as of this writing. The top end of our fair value estimate range sits at $398 per share of Microsoft. Shares of MSFT have regained their upward momentum of late, and we view its near-term capital appreciation upside potential quite favorably.

Our fourth options idea for the month of April 2022 is long put options on Tesla Inc (TSLA) with a $850 strike price that expire August 19, 2022. There is a lot to like about Tesla, though its strong financial performance and bright growth outlook is already reflected in its share price, and the technicals of its stock have deteriorated meaningfully of late. Elon Musk, a major Tesla shareholder as well as its CEO, is in the process of acquiring Twitter Inc (TWTR) through an all-cash deal worth ~$44 billion. Part of the financing scheme reportedly involves pledging $12.5 billion of his Tesla stock to secure a margin loan. Additionally, Musk has been selling a modest portion of his Tesla holdings of late.

The deal to acquire Twitter is clearly a distraction for someone already running two large enterprises (Tesla, SpaceX) and either running or playing an active role at other enterprises (The Boring Company, Neuralink, OpenAI). Additionally, Tesla is operating in an environment where traditional automakers are increasingly betting the barn on electric vehicles (‘EVs’), raising the competitive stakes. Tesla is also contending with headwinds at its Gigafactory Shanghai operations in the wake of lockdowns due to China’s zero coronavirus (‘COVID-19’) strategy.

We see room for shares of TSLA to continue drifting lower in the near term with our fair value estimate sitting at $816 per share and the lower end of our fair value estimate range sitting at $530 per share of Tesla.

These represent the second set of options ideas for the month of April 2022. Please let us know if you have any questions.

Be sure to note the dates of the articles in the options commentary stream that follows this article.

Our very best,

The Valuentum Team

www.valuentum.com

Please note that with options trading, investors can lose their entire premium. Don't ever trade with money that you can't afford to lose. Valuentum is an investment research publisher and accepts no liability for how readers may choose to utilize the content. By continuing with your additional options commentary membership, you accept our Terms and Conditions. If you do not agree with the Terms and Conditions, you must stop using this service and cancel your additional options commentary membership.

|

|

Image Shown: Shares of iShares US Home Construction ETF have fallen sharply in recent months, and we see room for additional downside.

April 27, 2022

Please always note the dates of the articles in the options commentary stream that follows this article. We hope you find this format helpful. Performance is hypothetical and no trading is taking place.

Dear members:

Today, we're highlighting the first and second options ideas for the month of April 2022. The first is long call options on the Dutch semiconductor equipment company ASML Holding NV (ASML) with a $700 strike price that expire October 21, 2022. ASML Holding makes the photolithography systems used to produce cutting edge chips, and the company has exposure to numerous secular tailwinds, which underpins its bright outlook.

We covered our thoughts on ASML Holding in our recent note ESG Newsletter Portfolio Idea ASML Holding May Further Boost Longer Term Guidance that we strongly encourage our members to check out (link here). The company has a pristine balance sheet (nice net cash position), stellar free cash flow generating abilities, a large backlog, and ample pricing power. According to its latest earnings update, ASML Holding may further increase its longer-term growth guidance in the wake of strong demand for its offerings (demand has been vastly stripping supply of late, a dynamic that is not expected to abate anytime soon).

Here is what we had to say on ASML Holding in our April 2022 article covering the name:

What really stood out in ASML Holding’s latest earnings update is management’s commentary regarding the longer-term guidance the firm put out during its September 2021 Investor Day event. For reference, the firm guided to generate annual revenues of approximately €24-€30 billion and a gross margin of approximately 54%-56% by (likely fiscal) 2025 and noted that there would be substantial growth opportunities after this period as well. In fiscal 2021, ASML Holding generated €18.6 billion in GAAP net sales and a GAAP gross margin of 52.7%. ASML Holding sees room for 11% annual revenue growth from (likely fiscal) 2020-2030.

ASML Holding is now “looking at [the] feasibility of further increasing (its) capacity beyond what (it) presented during (its) September 2021 Investor Day” event according to its latest earnings presentation. This is primarily due to strong demand for its offerings and the various secular tailwinds supporting demand growth for high-end chips and thus its most advanced photolithography systems (along with mature chips and its older offerings as well). Again, we would like to stress that at the high-end of the photolithography systems market, ASML Holding has a virtual monopoly.

Furthermore, the company noted “in light of the demand and (its) plans to increase capacity, (it) expect(s) to revisit (its) scenarios for 2025 and growth opportunities beyond. (It) plan(s) to communicate updates in the second half of the year” according to ASML Holding’s latest earnings presentation. We are excited by the potential that the firm will announce an upward revision to its longer-term guidance.

All things considered, a potential positive catalyst for shares of ASML is the pending update of its longer-term growth guidance, which could have an incredibly powerful impact on its stock price. We are bullish on ASML Holding and view both its near and longer term capital appreciation upside favorably. The company is quite shareholder friendly and utilizes its strong financial position to return cash to shareholders via a modest dividend program and sizable share repurchases.

Our second options idea for the month of April 2022 is long put options on iShares U.S. Home Construction ETF (ITB) with a $55 strike price that expire October 21, 2022. Surging 30-year mortgage rates and skyrocketing home prices are making it difficult for many US households to afford purchasing either a new or existing home. In turn, that is pressuring the holdings included in the ITB ETF.

According to Bankrate, the average 30-year US mortgage stands north of 5% on a nationwide basis which is up sharply from the ~3% rate seen at the end of 2021. The National Association of Realtors (‘NAR’) notes that in March 2022, the median existing home price in the US hit its highest level ever, coming in north of $375,000. Sales of existing homes dropped in March 2022 on a year-over-year basis according to NAR as a combination of rising home prices and mortgage rates took their toll.

The three largest holdings in the ITB ETF at the end of March 2022 were the homebuilders D.R. Horton Inc (DHI), Lennar Corporation (LEN), and NVR Inc (NVR) which combined represented about 35% of the ETF’s total holdings at the end of this period. Shares of DHI and LEN are down 30%+ year-to-date and shares of NVR are down 25%+ year-to-date as of this writing as investors are pricing in headwinds from inflationary pressures, labor shortages, supply chain hurdles, and most importantly, a decline in new home sales. We see room for the ITB ETF, and its various holdings, to fall further as mortgage rates are unlikely to fall significantly for at least the foreseeable future.

These are the first two ideas for the month of April 2022. Please let us know if you have any questions.

Please always note the dates of the articles in the options commentary stream that follows this article.

Always our very best,

The Valuentum Team

www.valuentum.com

Please note that with options trading, investors can lose their entire premium. Don't ever trade with money that you can't afford to lose. Valuentum is an investment research publisher and accepts no liability for how readers may choose to utilize the content. By continuing with your additional options commentary membership, you accept our Terms and Conditions. If you do not agree with the Terms and Conditions, you must stop using this service and cancel your additional options commentary membership.

|

|

April 11, 2022

Please always note the dates of the articles in the options commentary stream that follows this article. We hope you find this format helpful. Performance is hypothetical and no trading is taking place.

Dear options commentary members:

Trust you all are doing great!

Many of our options commentary ideas continue to be long call options ideas, as we seek to capitalize on what we believe will be continued strength in the equity markets during the back half of this year and into 2023. There are myriad headwinds to this bullish underlying thesis, but big-cap company fundamentals remain strong, and we think this will become evident during first-quarter 2022 earnings season, which will be here before we know it.

The latest Valuentum Weekly, released last night, has a plethora of fundamental information and commentary related to several of our open option idea considerations, not the least of which is long call options on Meta Platforms (FB) with a $250 strike price that expire June 17, 2022, long call options on PayPal Holdings (PYPL) with a $130 strike price that expire September 16, 2022, and long call options on the ProShares UltraPro QQQ ETF (TQQQ) with a $65 strike price that expire June 17, 2022.

The long call options on Meta Platforms and the ProShares UltraPro QQQ ETF were released February 11 (the theses on these ideas can be found in the commentary stream below related to that date), and the long call option idea on PayPal was released a couple weeks ago, as shown in the article that immediately follows this one. We believe that Meta Platforms and PayPal remain very attractive considerations, and we recently dug into the details in our latest work.

We think the market is paying attention to all of the wrong things. Certainly, interest rates are important and Fed rate hikes could dampen growth, but the reality is that interest rates are still at all-time lows, and we doubt that the Fed will do anything to impact the wealth effect it fought so hard to preserve during the depths of the COVID-19 pandemic. The Fed is helping guide these markets, and we think people are overreacting to their "corrective" measures to ensure long-term market health.

Broad market indexes that are top-heavy ("overweight") some of the strongest, big-cap tech names has been surfaced as another concern, but the reality is that we're okay with some of the indexes overweighting some of the best ideas. There's a reason why the S&P 500 (SPY) is down a modest ~6% this year, while some of the more speculative names such as in the ARK Innovation ETF (ARKK) are down almost 40% year-to-date. One ETF is overweight great companies with huge net cash positions and strong free cash flow generating abilities, while the other is overweight speculative names that are built on "castles in the air."

Stocks such as Apple (AAPL), Microsoft (MSFT), Alphabet (GOOG) (GOOGL), Amazon (AMZN), and Meta Platforms are huge companies with large market capitalizations for a tangible reason, too: They aren't overpriced bid up by speculators that have hope as a strategy, but rather they have excellent net cash rich, free cash generating, moaty business models tied to long-term secular growth trends, all of which offer fundamental support to their prices! We'd go so far as to say that we're huge fans of the overweighting of large cap growth in most broad market indexes, as it has and will likely continue to benefit investors tremendously!

The inflation fear-mongers are out in full force. When it comes to inflation, however, it could be a positive or negative depending on the company. Strong large cap growth entities are in a great position to price their products ahead of the rate of inflation, while some consumer staples entities with large net debt positions may struggle given possible consumer trade-down impacts. Within the context of enterprise valuation, we view the concept of inflation as practically equivalent to "pricing power" for companies that have it. That can be a good thing.

|

|

Image: "Gross domestic product (GDP), the featured measure of U.S. output, is the market value of the goods and services produced by labor and property located in the United States." Image Source: BEA.

|

|

Above is a long-term chart of the gross domestic product (GDP) of the United States in the post-World War II period. The shaded areas are recessions. You can see how far we have come from the depths of the Great Financial Crisis in 2008-2009, and how far we've come from the COVID-19 shutdowns. The United States' economy is roaring, and while nominal GDP may be impacted by stronger levels of inflation, again, that is not necessarily a bad thing for companies that can manage their cost structure effectively to drive real earnings expansion.

We're not expecting a recession anytime soon, but one thing is clear: The United States' economy has emerged stronger from the worst economic collapse since the Great Depression in the Great Financial Crisis, and the United States' economy has emerged stronger from the worst health crisis since the Flu Pandemic of 1917-1918 in the COVID-19 outbreak. We doubt a recession in the United States is on the horizon, but if it is, the United States' economy will bounce back and bounce back stronger. Any impact from a modest recession is also largely captured within the fair value estimate ranges of many of our valuation models, too, so we're not panicking at all.

With all this said, we're making a number of housekeeping moves with respect to our previously-released options ideas. We have a number of options ideas that will expire April 14, 2022, including long calls on Laredo Petroleum (LPI), Callon Petroleum Company (CPE), Qualcomm (QCOM), and Republic Services (RSG). Though these ideas have at times looked like they might work out, we've ran out of time, and we're going to 'close' them to preserve any residual value that may be remaining. These 'closes' will be reflected in the updated table that tracks our options ideas generation in a coming update.

Stay tuned for the first two options ideas for the month of April in the coming days. We hope you are enjoying your additional options commentary membership, and if we can be of any assistance, please just let us know. Always our very best!

Kind regards,

The Valuentum Team

www.valuentum.com

Please note that with options trading, investors can lose their entire premium. Don't ever trade with money that you can't afford to lose. Valuentum is an investment research publisher and accepts no liability for how readers may choose to utilize the content. By continuing with your additional options commentary membership, you accept our Terms and Conditions. If you do not agree with the Terms and Conditions, you must stop using this service and cancel your additional options commentary membership.

|

|

Image Shown: Shares of Apple Inc (blue line) and PayPal Holdings Inc (orange line) have been on a nice upward trend in recent weeks.

March 31, 2022

Please always note the dates of the articles in the options commentary stream that follows this article. We hope you find this format helpful. Performance is hypothetical and no trading is taking place.

Dear members:

Today, we're highlighting our third and fourth options ideas for the month of March 2022. In case you missed the first two option idea considerations this month, they can be found in the article that immediately follows this one.

The third idea is long call options on Apple Inc (AAPL) with a $185 strike price that expire September 16, 2022. Granted, Apple is not a hidden opportunity, but sometimes the best ideas can be right under our noses. The company's fundamentals remain rock-solid, and we think it will be a prime beneficiary of the rotation back into large cap growth and big cap tech names in the coming months and during the back half of this year.

We continue to be enormous fans of Apple given its fortress-like balance sheet, immense free cash flow generation, and bright earnings growth outlook. Shares of AAPL have shot higher during the past few weeks, and we see room for additional upside potential. Our fair value estimate for Apple sits at $170 per share, but we think the high end of our fair value estimate range north of $200 per share is within reach under the right market conditions. As of this writing, the company’s stock price is converging towards the upper end of that range.

We expect shares of Apple will continue shifting higher in the near term.

Apple announced the launch of a new edition of its iPhone SE, which is a budget version of its smartphone lineup, that is still 5G-capable and powered by its new A15 chip (designed by Apple) during a product event held this month. In the wake of inflationary pressures and concerns regarding purchasing power, Apple is making sure that its iPhone lineup is catering to consumers across the income spectrum.

Apple also announced new colors for its iPhone 13 and iPhone 13 Pro along with the news that it would air some MLB games, even for those without an Apple TV+ subscription, during the March 2022 product event. In January 2022, we covered our thoughts on Apple’s recent financial performance in an article that can be viewed here.

Our fourth options idea for the month of March 2022 is long call options on PayPal Holdings Inc (PYPL) with a $130 strike price that expire September 16, 2022. Shares of the fintech company have plummeted during the past six months, though in recent weeks its stock price has staged a recovery, and we see room for further capital appreciation upside potential in the near term.

The sell-off in shares of PYPL during the past few months is overdone, in our view. PayPal has a pristine balance sheet with a nice growth trajectory and substantial free cash flow generation. Our fair value estimate for PayPal sits at $152 per share and the top end of our fair value estimate range sits at $182 per share. We covered our thoughts on PayPal in a February 2022 article that can be viewed here, which we strongly encourage members to check out.

That's it for now. Please let us know if you have any questions.

Please always note the dates of the articles in the options commentary stream that follows this article.

Always our very best,

The Valuentum Team

www.valuentum.com

Please note that with options trading, investors can lose their entire premium. Don't ever trade with money that you can't afford to lose. Valuentum is an investment research publisher and accepts no liability for how readers may choose to utilize the content. By continuing with your additional options commentary membership, you accept our Terms and Conditions. If you do not agree with the Terms and Conditions, you must stop using this service and cancel your additional options commentary membership.

|

|

Image Shown: The surge in raw energy resources pricing seen of late has been a boon for Occidental Petroleum Corporation (orange line) but a major drag on the US Global Jets ETF (blue line).

March 25, 2022

Please always note the dates of the articles in the options commentary stream that follows this article. We hope you find this format helpful. Performance is hypothetical and no trading is taking place.

Dear members:

Our first options idea for the month of March 2022 is put options on the US Global Jets ETF (JETS) with a $20 strike price that expire June 17, 2022. The commercial passenger airliner business is not conducive to economic value creation through the course of the economic cycle, and only in a few rare instances since deregulation has the industry come close to capturing its cost of capital.

Airliners are troubled with hefty fixed costs from labor to expensive aircraft and are exposed to major inflationary headwinds. Recent increases in kerosene (jet fuel) prices as a result of surging crude oil prices combined with significant nominal labor/wage increases are aggressively eroding away the bottom line of the companies included in the JETS ETF. Additionally, many of these firms have bloated balance sheets and have limited financial flexibility to navigate these turbulent times.

Though the commercial passenger airliner industry is turning to pricing increases to offset the worst of ongoing inflationary pressures, in a highly commoditized space, it is difficult to push through large price increases without losing potential customers to other airliners that offer a similar service at a lower rate. The uplift from large parts of the world putting the worst of the coronavirus (‘COVID-19’) pandemic behind us was supposed to provide a major tailwind for the industry, though the Ukraine-Russia crisis may weigh quite negatively on international travel activity going forward, as will rising ticket prices.

In our view, the JETS ETF will face sizable selling pressures in the near term.

Our second idea for the month of March 2022 is call options on Occidental Petroleum Corporation (OXY) with a $60 strike price that expire June 17, 2022. Raw energy resources prices are surging, and Occidental Petroleum has no direct exposure to Russia. Occidental Petroleum operates a large exploration & production (‘E&P’) business alongside a moderate amount of energy infrastructure (midstream assets) and petrochemical plants. Its domestic E&P operations are focused on the Permian Basin, the DJ Basin, the Powder River Basin, and the Gulf of Mexico while its international E&P operations are focused on opportunities in Oman, Algeria, and Abu Dhabi in the UAE.

Currently, Occidental Petroleum is focused on paying down debt and returning cash to shareholders via share buybacks and dividend increases as its free cash flows should swell higher in the current environment. We see room for shares of OXY to run higher still, after rallying in recent weeks, as the top end of our fair value estimate range sits at $70 per share. Warren Buffett’s Berkshire Hathaway Inc (BRK.A) (BRK.B) has been steadily buying up Occidental Petroleum’s common stock in recent weeks. Berkshire also owns warrants and preferred equity in Occidental Petroleum.

In our view, Occidental Petroleum’s near term capital appreciation upside potential is significant.

Please let us know if you have any questions.

Please always note the dates of the articles in the options commentary stream that follows this article.

Always our very best,

The Valuentum Team

www.valuentum.com

Please note that with options trading, investors can lose their entire premium. Don't ever trade with money that you can't afford to lose. Valuentum is an investment research publisher and accepts no liability for how readers may choose to utilize the content. By continuing with your additional options commentary membership, you accept our Terms and Conditions. If you do not agree with the Terms and Conditions, you must stop using this service and cancel your additional options commentary membership.

|

|

Image Shown: Shares of the SPDR S&P Aerospace & Defense ETF (XAR) are breaking out of their downtrend on news of increased military spending across Europe. The uncertainty caused by Russia's invasion of Ukraine and the resulting economic sanctions by the West on Russia could result in increased defense budgets across continental Europe for years to come.

February 28, 2022

Please always note the dates of the articles in the options commentary stream that follows this article. We hope you find this format helpful. Performance is hypothetical and no trading is taking place.

Dear members:

With a conflict raging in Ukraine, we understand that it may be hard to focus on the stock market with so much suffering going on. In case you missed it, our latest work on the Ukraine/Russia crisis can be accessed here. We hope to see peace in Ukraine soon.

Today, we are highlighting the third and fourth options ideas for the month of February. As a response to Russia's invasion of Ukraine, we are witnessing a re-militarization of Europe. Just yesterday, for example, Germany announced that it would raise its defense budget to "100 billion euros" in 2022 -- more than double that of 2021. Other countries may follow with higher spending, too.

It is too early to say whether the world has entered into a new 21st century "Cold War," but it is clear that national defense has become a much more important priority around the world. Not only will militaries in Europe likely need to modernize much of their equipment, but spending to guard against cyber attacks will also become a necessity, especially in an age of military warfare that includes the cyberspace. It is with this view that we are highlighting the SPDR S&P Aerospace & Defense ETF (XAR) and the ETFMG Prime Cyber Security ETF (HACK) as our second set of options idea considerations for the month of February.

Increased spending in Europe and across the globe in the areas of national defense/security and to prevent cyber attacks will be the rising tide that lifts many boats in these ETFs, in our view. When it comes to defense, we generally prefer the XAR over other defense ETFs, including the iShares U.S. Aerospace & Defense ETF (ITA), because the XAR has strong exposure to the major defense contractors but a lower weighting in Boeing (BA), a stock we view as less attractive from a financial/fundamental basis than other pure-play defense contractors [for example, the BA weighting in XAR is ~4%, while the BA weighting in ITA is ~17%]. Boeing continues to struggle to right its own ship, and its financials aren't nearly as attractive as they once were prior to the 737 MAX debacle and COVID-19 outbreak.

Specifically, as it relates to the two new ideas, we are highlighting "in-the-money" long call options on the XAR with a $120 strike price that expire July 15, 2022. Though we like this ETF, please note that trading is thin across the XAR options chain, so keep bid/ask spreads in mind. We are also highlighting long call options on the HACK with a $60 strike price that expire June 17, 2022. Though the prices of these ETFs are bouncing today on expectations for increased defense/cyber spending around the world as a result of Russia's aggression, we think expectations have yet to be fully reset to higher levels.

With the rest of the world, we continue to monitor the events unfolding in Ukraine, and members should expect ongoing updates from us in the coming days and weeks. We're available for any questions, and may there be peace in Ukraine soon. Stay safe.

Always note the dates of the articles in the options commentary stream that follows this article.

Kind regards,

The Valuentum Team

www.valuentum.com

Please note that with options trading, investors can lose their entire premium. Don't ever trade with money that you can't afford to lose. Valuentum is an investment research publisher and accepts no liability for how readers may choose to utilize the content. By continuing with your additional options commentary membership, you accept our Terms and Conditions. If you do not agree with the Terms and Conditions, you must stop using this service and cancel your additional options commentary membership.

|

|

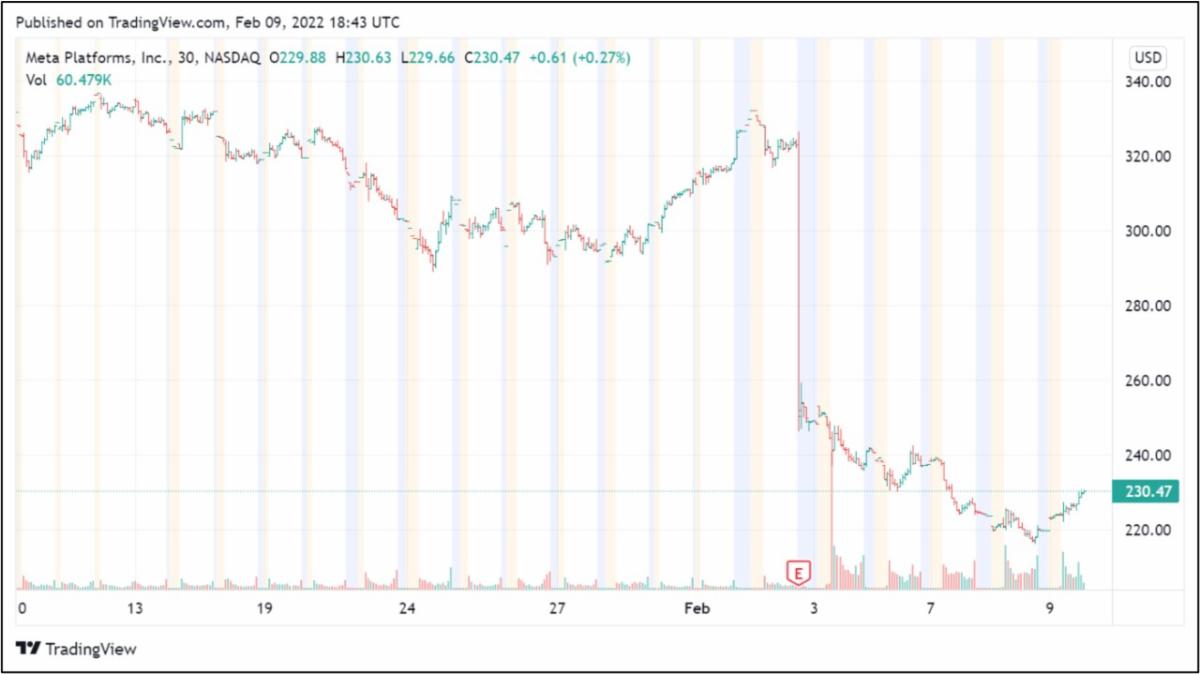

Image Shown: Shares of Meta Platforms Inc tanked after the owner of Facebook and Instagram posted its latest earnings report in early February 2022. More recently, shares of FB have started to firm up. After fine-tuning our valuation model in the wake of its latest earnings report, we continue to view Meta Platforms as one of the most undervalued companies out there. Bigger picture, large cap US growth equities remain the place to be, in our view.

February 11, 2022

Please always note the dates of the articles in the options commentary stream that follows this article. We hope you find this format helpful. Performance is hypothetical and no trading is taking place.

Dear members:

Today, we are highlighting the first and second options ideas for the month of February 2022, but before we do, we are "closing" a number of previously-highlighted ideas. They are as follows (data according to YahooFinance):

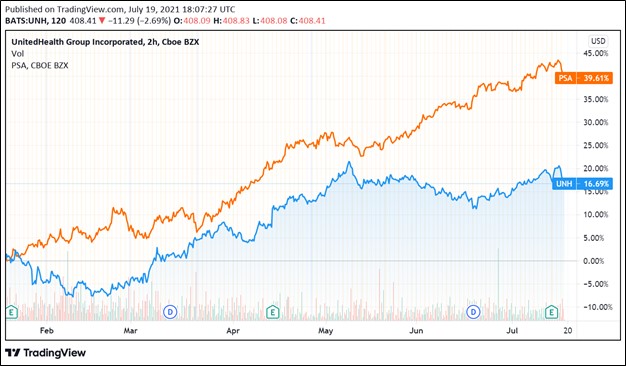

January 21 Idea: Long call options on the health insurance and health care provider giant UnitedHealth Group Inc (UNH) with a $490 strike price that expire June 17, 2022. Highlight bid/ask spread: $20.65/$22.00. "Close" bid/ask spread: $28.75/$30.10. Winner.

January 21 Idea: Long call options on one of our favorite industrial firms, Lockheed Martin Corp (LMT), with a strike price of $400 that expire June 17, 2022. Highlight bid/ask spread: $10.40/$11.00. "Close" bid/ask spread: $12.90/$13.60. Winner.

December 19 idea: Long call options on Vertex Pharmaceuticals Inc (VRTX) with a $250 strike price that expire April 14, 2022. Highlight bid/ask spread: $5.70/$9.50. "Close" bid/ask spread: $7.40/$9.90. Close.

December 15 idea: Long call options on Dick’s Sporting Goods Inc (DKS) with a $120 strike price that expire March 18, 2022. Highlight bid/ask spread: $5.00/$5.90. "Close" bid/ask spread: $5.00/$5.20. Close.

Our first idea for the month of February is long call options on Meta Platforms Inc (FB), formerly known as Facebook, with a $250 strike price that expire June 17, 2022. Shares of FB have faced an immense amount of selling pressure after it posted its fourth quarter earnings update on February 2.

We've fine-tuned our valuation model accordingly, factoring in the company's (self-imposed, discretionary) increased expense headwinds and making a variety of other tweaks (as Meta Platforms is investing heavily in data centers and its big “metaverse” strategy), and we believe our top-line growth forecasts remain conservative.

Over the past year, shares of Facebook are down about 15%-20%, while the ARKK has been halved, so even though we're disappointed by the sell-off in FB, we like the relative strength versus "junk" tech.

After fine-tuning our valuation model, we continue to believe Meta Platforms is one of the most undervalued companies out there. Our updated fair value estimate sits at $413 per share of FB. We published an article on V.com on February 4 (link here) covering our thoughts on Meta Platforms (lightly edited):

"For starters, we think the market is getting Meta wrong, as the company's cash-based sources of intrinsic value continue to be phenomenal. Let's put what we're saying into context. Meta's market capitalization now stands at [just over $600 billion]. Last fiscal year, it generated nearly $40 billion in free cash flow as it held about $50 billion in net cash on the balance sheet.

Hypothetically, for valuation context, assuming no growth, on average, in free cash flow the next three years, and that Meta allocates the sum of those next three year's future free cash flow generation plus its current net cash to share repurchases, Meta could buy back ~25% of itself (in 3 years!), if it does nothing operationally but hold the line, on average (while still spending vigorously on capex and buybacks).

We think Meta's stock sell off may have more to do with people disliking Facebook, the company, than the stock, itself. With what we believe to be a very, very conservative updated valuation, we still value FB shares north of $400 per share, and we reiterate that we're using very modest future expected revenue growth rates, hardly any operating leverage improvements, and incorporating massive capital spending for the investments in the metaverse, data centers, and the like."

As of this writing, Meta Platforms is trading near $225 per share.

Though its technicals have yet to form what could be considered a "bottom," we see ample room for shares of FB to rebound over the coming weeks and months as Meta Platforms’ equity is incredibly undervalued. To read more about our thoughts on Meta Platforms, please check out this article here, and to learn more about why we are still pounding the table for Meta Platforms, please check out our video here.

Pivoting to our second options idea for February 2022, we are highlighting long call options on the ProShares UltraPro QQQ ETF (TQQQ) with a $65 strike price that expire June 17, 2022. According to the ETF’s website, the TQQQ ETF “seeks daily investment results, before fees and expenses, that correspond to three times (3x) the daily performance of the Nasdaq-100 Index.”

As of this writing, ten-year US Treasuries are yielding just over 2.05% after moving higher in recent months. However, that is not a level that would single-handedly justify the recent selloff seen in the stock prices of large cap U.S. tech firms, a sell off in our view that is well overdone.

Large cap U.S. tech companies, collectively, are a rather defensive place to be, too, in our view, given their huge net cash positions and strong free cash flow profiles. The Federal Reserve is steadily winding down its monthly asset purchase program, dubbed Quantitative Easing (‘QE’), and numerous Fed officials have communicated that interest rate increases are likely in the near term to combat inflationary headwinds.

Rising interest rates may pressure the intrinsic value of equities, by themselves, especially companies with long growth tails (particularly some money-losing technology firms) -- but as the relative comparison between a company such as FB and those in the ARKK during the past 52 weeks has revealed, not all tech firms are created equally. Large cap growth tech, even when faced with difficulty as in the case of FB, for example, is much more defensive.

The largest companies included in the NASDAQ 100 index are stellar free cash flow generators with ample pricing power and promising growth outlooks that often have relatively strong balance sheets as well. We expect that the NASDAQ 100 index to perk up over the coming weeks and months and view long call options on the TQQQ ETF as a great way to play this potential rebound. Note that this idea may be the most speculative one we've ever highlighted.

Please let us know if you have any questions.

Always note the dates of the articles in the options commentary stream that follows this article.

Our very best,

The Valuentum Team

www.valuentum.com

Please note that with options trading, investors can lose their entire premium. Don't ever trade with money that you can't afford to lose. Valuentum is an investment research publisher and accepts no liability for how readers may choose to utilize the content. By continuing with your additional options commentary membership, you accept our Terms and Conditions. If you do not agree with the Terms and Conditions, you must stop using this service and cancel your additional options commentary membership.

|

|

Image Shown: Shares of Lockheed Martin Corporation (blue line) and UnitedHealth Group Inc (orange line) appear well-positioned to shift higher over the coming weeks and months, in our view, as the market grows more defensive in nature.

|

|

January 21, 2022

Please always note the dates of the articles in the options commentary stream that follows this article. We hope you find this format helpful. Performance is hypothetical and no trading is taking place.

Dear members:

With the markets selling off Friday, January 21, we think the time is ripe to highlight a few long call ideas.

First, however, we're closing the November options idea consideration, the long call options on the SPDR Gold Trust ETF (GLD) with a $170 strike price that expire today, January 21. Though the current residual options premium bid/ask spread in the GLD is below the highlight price premium's bid/ask spread, we think it makes sense to be prudent and "close" this one to preserve any residual value in this now in-the-money play.

We're also "closing" another November options idea consideration, the long put options idea on the SPDR Dow Jones Industrial Average ETF Trust (DIA) with a $340 strike price that expires today as well, January 21. Though the latest selling in the markets speaks to our being "correct" in looking for puts, the Dow Jones Industrial Average just didn't fall enough to make this a "winning" idea, so we'll be "closing" it to preserve any residual premium.

Without any delay, let's now cover our third and fourth options idea considerations for the month of January 2022. The third idea for the month of January is long call options on one of our favorite industrial firms, Lockheed Martin Corp (LMT), with a strike price of $400 that expire June 17, 2022. The defense contractor is scheduled to report its fourth-quarter 2021 earnings before the market open on January 25.

Lockheed Martin is getting closer to completing its all-cash acquisition of Aerojet Rocketdyne Holdings Inc (AJRD), which has a total transaction value of ~$4.4 billion when including the assumption of net cash. The deal will add Aerojet Rocketdyne's propulsion systems to Lockheed Martin’s portfolio and is expected to strengthen its ‘Aeronautics,’ ‘Missiles and Fire Control,’ and ‘Space’ business segments.

Lockheed Martin has included Aerojet Rocketdyne as part of its supply chain for some time. Reportedly, the US Federal Trade Commission (‘FTC’) should soon vote on whether to approve the deal, which was first announced back in December 2020.

We view Lockheed Martin’s capital appreciation upside quite favorably as shares of LMT have steadily moved higher of late. The top end of our fair value estimate range stands at ~$450 per share of Lockheed Martin.

Readers interested in learning more about Lockheed Martin are encouraged to check out our September 2021 article covering its extensive growth runway in the realm of commercial, government, and military space activities (link here). We also encourage readers to pay attention to news regarding the risks to its future free cash flow trajectory, as outlined in this note here.

Our fourth options idea for the month of January is long call options on the health insurance and health care provider giant UnitedHealth Group Inc (UNH) with a $490 strike price that expire June 17, 2022. The company recently reported a solid fourth-quarter 2021 earnings update, which we covered in this article here. Shares of UNH moved higher after its latest earnings report, and the company reaffirmed its promising 2022 guidance in conjunction with the report.

Here is what we had to say in our article covering the event:

"Looking ahead, UnitedHealth forecasts that it will generate $317-$320 billion in revenue this year, which represents 11% annual growth at the midpoint. Additionally, UnitedHealth expects to generate $21.10-$21.60 in non-GAAP adjusted EPS (up 12% year-over-year at the midpoint) and $23.0-$24.0 billion in operating cash flow (up 5% year-over-year at the midpoint) this year. UnitedHealth’s growth trajectory is expected to continue in earnest in 2022, which we appreciate."

The top end of our fair value estimate range sits at ~$510 per share of UnitedHealth, and we view its near-term capital appreciation upside potential quite favorably. We strongly encourage readers to check out our earnings note covering UnitedHealth. Here is where you can find UNH's stock page >>

We're available for any questions.

Please always note the dates of the articles in the options commentary stream that follows this article.

Always our very best,

The Valuentum Team

www.valuentum.com

Please note that with options trading, investors can lose their entire premium. Don't ever trade with money that you can't afford to lose. Valuentum is an investment research publisher and accepts no liability for how readers may choose to utilize the content. By continuing with your additional options commentary membership, you accept our Terms and Conditions. If you do not agree with the Terms and Conditions, you must stop using this service and cancel your additional options commentary membership.

|

|

Image Shown: Shares of Callon Petroleum Company (blue line) and Laredo Petroleum Inc (orange line) have surged higher over the past year, with room for additional upside potential going forward as raw energy resources pricing has been marching higher of late.

January 19, 2022

Please always note the dates of the articles in the options commentary stream that follows this article. We hope you find this format helpful. Performance is hypothetical and no trading is taking place.

Dear members:

Today, we're highlighting the first two options idea considerations for the month of January 2022, specifically long call option ideas on some high-quality exploration and production (‘E&P’) companies focused on oil-rich “fracking” opportunities in the U.S.

Fracking opportunities are short-cycle endeavors that can churn out cash flows relatively quickly (within months instead of years for other oil & gas projects), making it easier for these firms to capitalize on favorable movements in raw energy resources pricing. Crude oil prices have been shifting higher of late as the Omicron variant of the coronavirus (‘COVID-19’) pandemic is proving to be more manageable than first feared while the OPEC+ oil cartel is staying the course as it concerns slowly unwinding their supply curtailment agreement.

Our first idea is long call options on Callon Petroleum Company (CPE) with a $65 strike price that expire April 14, 2022. Callon Petroleum primarily focuses on upstream opportunities in the Permian Basin in West Texas and to a lesser extent, the Eagle Ford play in South Texas. In October 2021, Callon Petroleum completed its acquisition of Primexx Energy Partners through a ~$0.8 billion cash-and-stock deal that significantly grew its presence in the Permian Basin. Callon Petroleum also recently announced the sale of non-core assets in the Eagle Ford as part of its portfolio optimization process.

We like Callon Petroleum as greater scale in the Permian Basin should provide the firm with ample oil-rich development opportunities to capitalize on. The company generated ~$0.2 billion in free cash flow during the first nine months of 2021 as it benefited immensely from the ongoing recovery in the global energy complex. Callon Petroleum does not pay out a common dividend at this time and did not repurchase a significant amount, or any, of its common stock during this period as the firm instead repaired its balance sheet.

Going forward, Callon Petroleum is focused on deleveraging efforts and integrating its acquisition of Primexx Energy Partners. Callon Petroleum’s net debt load (inclusive of short-term debt, though it had none on the books at the end of both periods) fell by over $0.5 billion from the end of the second quarter of 2020 to the end of the third quarter of 2021. By the end of fiscal 2022, Callon Petroleum aims to bring its net debt to adjusted EBITDA ratio down below 2.0x, versus 4.2x at the end of fiscal 2020. We expect Callon Petroleum’s newfound fiscal discipline will continue to win over investors and view the company’s capital appreciation upside quite favorably.

Our second idea is long call options on Laredo Petroleum Inc (LPI) with an $85 strike price that expire April 14, 2022. Laredo Petroleum primarily focuses on developing upstream opportunities in the Permian Basin play. Just like Callon Petroleum, Laredo Petroleum is focused on improving its free cash flow generating abilities and paying down debt after making some big changes to its asset base.

In May 2021, Laredo Petroleum announced a ~$0.7 billion cash-and-stock deal to acquire the assets of Sabalo Energy and a non-operating partner, bolstering its position in the Permian Basin (particularly in regions of the Permian Basin where Laredo Petroleum is actively pursuing growth opportunities). Additionally, Laredo Petroleum also announced it was divesting a sizable stake in some of its operated legacy assets in the Permian Basin for ~$0.4 billion to raise cash for the acquisition. These deals closed in July 2021. In September 2021, Laredo Petroleum announced it was acquiring leaseholds from Pioneer Natural Resources Company (PXD) in the Permian Basin through a bolt-on acquisition for ~$0.2 billion, and that deal closed in October 2021.

During the first nine months of 2021, Laredo Petroleum generated a modest amount of positive free cash flows, which was an improvement from the negative free cash flows the firm generated in the same period the prior year. As it works towards integrating its recently acquired assets, Laredo Petroleum should be able to improve its free cash flow performance. Rising raw energy resources pricing will help out on this front.

Laredo Petroleum aims to reduce its leverage ratio (net debt to adjusted EBITDA) down to 1.5x by the end of fiscal 2022, and possibly even lower by fiscal 2023 according to recent management commentary. The company does not have any major tranches of its debt coming due until 2025 at the earliest, providing it with ample time to complete its asset integration work while improving its free cash flow generating performance.

We see room for ample capital appreciation upside potential in the near term at both Callon Petroleum and Laredo Petroleum as the outlook for the global energy complex continues to improve. The increase in crude oil prices seen of late will go a long way in enabling both companies to repair their balance sheets, which took a beating from the coronavirus (‘COVID-19’) pandemic. In our view, investors will appreciate the pivot towards fiscal discipline at both oil-focused E&P firms.

We're available for any questions.

Please always note the dates of the articles in the options commentary stream that follows this article.

Always our very best,

The Valuentum Team

www.valuentum.com

Please note that with options trading, investors can lose their entire premium. Don't ever trade with money that you can't afford to lose. Valuentum is an investment research publisher and accepts no liability for how readers may choose to utilize the content. By continuing with your additional options commentary membership, you accept our Terms and Conditions. If you do not agree with the Terms and Conditions, you must stop using this service and cancel your additional options commentary membership.

|

|

Image Shown: Shares of Qualcomm Inc (depicted by the blue line in the above graph) and Vertex Pharmaceuticals Inc (depicted by the orange line) have surged higher during the past three months into late December 2021. We see ample room for shares of QCOM and VRTX to continue climbing higher going forward as we get ready for 2022.

December 29, 2021

Please always note the dates of the articles in the options commentary stream that follows this article. We hope you find this format helpful. Performance is hypothetical and no trading is taking place.

Dear members:

We hope you had a wonderful time with family, friends, and loved ones during this past Christmas weekend. Today, we're highlighting the third and fourth options ideas for the month of December 2021. Our third idea is long call options on Qualcomm Inc (QCOM) with a $190 strike price that expire April 14, 2022.

In November 2021, Qualcomm forecasted that its addressable market opportunity will grow by ~$100 billion over the next decade to reach ~$700 billion by 2030 during its 2021 Investor Day event. Shares of QCOM have surged higher since then as investors are becoming increasingly bullish on the semiconductor company’s longer term growth trajectory.

The high end of our fair value estimate sits at $206 per share of Qualcomm, indicating there is ample room for shares of QCOM to run even higher (shares are trading at ~$186 each at the time of this writing). We covered why we are big fans of Qualcomm in this article here that we strongly encourage our members to check out.

Our fourth options idea for the month of December 2021 is long call options on Vertex Pharmaceuticals Inc (VRTX) with a $250 strike price that expire April 14, 2022. Please note that with this idea there are liquidity concerns (i.e. a wide bid/ask spread) as this options tranche is thinly traded.

Vertex Pharma is one of our favorite biotech plays out there. The company has a history of meaningful guidance increases and recently published favorable clinical trial data on one of its leading drug candidates, topics that we covered in this article here that we strongly encourage our members to check out.

Vertex Pharma is a net cash-rich, free cash flow generating company in an industry where many companies generally are burning through vast amounts of cash. It is also actively buying back its stock, helping to provide equity-price support, and has upside potential with respect to CRISPR technology via partnerships.

Our fair value estimate sits at $250 per share of VRTX, and the high end of our fair value estimate range sits at $350 per share (shares are trading at ~$223 each at the time of this writing). We see ample room for Vertex Pharma’s stock price to continue surging higher in the coming months. Shares of VRTX have exhibited strong technical performance of late, too.

Please let us know if you have any questions, and have a Happy New Year!

Please always note the dates of the articles in the options commentary stream that follows this article.

Always our very best,

The Valuentum Team

www.valuentum.com

Please note that with options trading, investors can lose their entire premium. Don't ever trade with money that you can't afford to lose. Valuentum is an investment research publisher and accepts no liability for how readers may choose to utilize the content. By continuing with your additional options commentary membership, you accept our Terms and Conditions. If you do not agree with the Terms and Conditions, you must stop using this service and cancel your additional options commentary membership.

|

|

Image Shown: Shares of Republic Services Inc have been on an upward tear year-to-date as of this writing, and we see room for additional upside potential. A meaningful portion of the garbage hauler's contractual agreements are CPI-based, meaning that it has the capacity to generate additional service pricing gains as traditional measures of inflation remain elevated.

|

|

December 15, 2021

Please always note the dates of the articles in the options commentary stream that follows this article. We hope you find this format helpful. Performance is hypothetical and no trading is taking place.

Dear members:

Today, we're highlighting the first and second options ideas for the month of December 2021. Our first idea is long call options on Dick’s Sporting Goods Inc (DKS) with a $120 strike price that expire March 18, 2022. Our fair value estimate for the sporting goods retailer sits at $148 per share (shares are trading at ~$105 at the time of this writing). Dick's Sporting Goods' stock page >>

When the sporting goods retailer reported third quarter earnings for fiscal 2021 (period ended October 31, 2021) on November 23, the company beat both consensus top- and bottom-line estimates. Additionally, Dick's Sporting Goods once again raised its full-year guidance for fiscal 2021 in conjunction with its latest earnings update (we covered the firm’s latest earnings and outlook in this article here).

The company’s Executive Chairman and former CEO, Stack Edward, recently purchased some shares of DKS (link to the relevant Form 4 SEC filing), and we see this as a good sign. We view Dick’s Sporting Goods’ capital appreciation upside potential quite favorably and appreciate management’s growing confidence in the company’s outlook, a confidence we share.

We believe the holiday selling season will be a good one, too, despite some supply chain hiccups across various verticals, and Dick's Sporting Goods' omni-channel strategy continues to resonate with athletes, coaches and beyond. The sporting goods retailer has some of the best brands for the serious athlete, and we're expecting a big calendar fourth quarter as consumers think "healthy" with respect to holiday gift giving -- especially as sports at all levels get back to "normal" following the shutdowns and safety precautions to limit the spread of COVID-19.

Shares have also seemed to be hitting technical support in the $100-$105 per-share price range after closing the gap up in August. We think shares of Dick's Sporting Goods are setting up nicely.

The second options idea for December 2021 is long call options on Republic Services Inc (RSG) with a $140 strike price that expire April 14, 2022. We caution that these options have seen only modest levels of daily trading activity of late, meaning there are liquidity concerns to be aware of here, namely a rather wide bid/ask spread.

This idea is not one that we expect to generate the type of huge hypothetical "gains" as some of our more recent ideas, but we like the "positioning" heading into a more volatile end-of-year period.

On a fundamental basis, Republic Services posted a stellar third quarter 2021 earnings update on October 28, which saw the firm beat both consensus top- and bottom-line estimates. The waste management company also (once again) raised its full-year guidance in conjunction with its latest earnings report (we covered its previous guidance boosts in this article here).

We see ample room for capital appreciation upside potential going forward at Republic Services, as many larger investors seek to do some de-risking as a result of the fallout of more speculative ARK Innovation-type stocks. This could result in a bump in the value ascribed to this options idea consideration, as markets remain choppy (volatile) and therefore attract incremental money flow to more conservative ideas.

Republic Services also has exposure to CPI-linked contractual pricing arrangements, and with inflation coming in hotter than expectations, some may start to view Republic as a unique inflation hedge. This could attract even more capital to the position. Republic Services' stock page >>

We look forward to releasing the second two options ideas for the month of December in the coming weeks. Let us know if you have any questions, and we hope you are enjoying this wonderful holiday season!

Please always note the dates of the articles in the options commentary stream that follows this article.

Always our very best,

The Valuentum Team

www.valuentum.com

Please note that with options trading, investors can lose their entire premium. Don't ever trade with money that you can't afford to lose. Valuentum is an investment research publisher and accepts no liability for how readers may choose to utilize the content. By continuing with your additional options commentary membership, you accept our Terms and Conditions. If you do not agree with the Terms and Conditions, you must stop using this service and cancel your additional options commentary membership.

|

|

Image Shown: Though we remain very bullish on the stocks that make up the category of large cap growth (see here), some downside protection may be warranted, in our view, due to recent reports coming out of South Africa concerning a new highly transmissible and complex variant of COVID-19, referred to as the Omicron variant. Equity markets in the US are currently trading just below their all-time highs, with the SPDR Dow Jones Industrial Average ETF Trust shown in the chart up above. We are monitoring the situation closely as markets appear spooked by the news as the chance of another round of lockdowns, particularly in Europe, continues to grow. Investors shouldn't panic by any stretch, however, and we remain very bullish on stocks for the long haul.

November 30, 2021

Please always note the dates of the articles in the options commentary stream that follows this article. We hope you find this format helpful. Performance is hypothetical and no trading is taking place.

Dear members:

Today, we are highlighting the third and fourth options ideas for the month of November 2021. But before we do, we think it makes sense to reiterate our bullish take on the equity markets and point to the area of large cap growth as one of our favorites (see here).

For the past many years, we've been pounding the table on companies that comprise large cap growth, including Facebook (FB), Alphabet (GOOG), Microsoft (MSFT), Apple (AAPL) and beyond, and we've shunned overleveraged entities that have trouble paying their dividends with free cash flow.

Probably to no member's surprise, the area of large cap growth has been one of the best performers in the past five years, while MLPs, which are overleveraged and have trouble meeting their dividend obligations, have been one of the worst. It's always nice to see things line up the past 5 years largely how we predicted (see here).

With that said, let's dig into the new ideas. Our third idea for the month of November is long put options on the SPDR Dow Jones Industrial Average ETF Trust (DIA) with a $340 strike price that expire on January 21, 2022, and our fourth idea is long call options on the SPDR Gold Trust ETF (GLD) with a $170 strike price that expire on January 21, 2022.

As you're probably aware, there have been recent reports coming out of South Africa that a complex and highly transmissible strain of the coronavirus (‘COVID-19’) has begun to spread, known as the Omicron variant, which is spooking markets. Reportedly, mutations in the spike protein of the B.1.1.529 (the Omicron) variant are of particular concern. Confirmed cases of the Omicron variant have been identified in South Africa, various countries in Europe (including the UK, Germany, and Italy), along with other countries including Israel and Hong Kong.