|

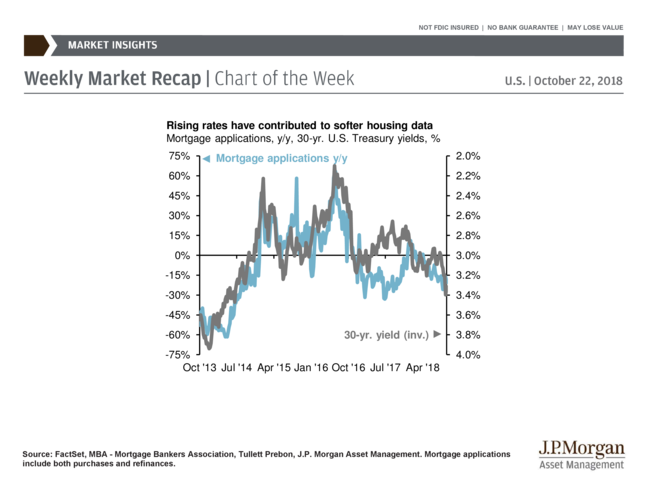

Housing Chart

Housing starts are considered one of the leading economic indicators for economists. This indicator provides a timely glimpse into the health of the overall economy. Even at their peak during this current economic expansion, housing starts have remained well below their pre-crisis level. Additionally, they were uncharacteristically slow to recover during this expansion phase as well. This may have been due to the tighter lending standards that had been established following the financial crisis. But it is worth noting that the housing starts data suggests a softening has begun. This is likely due to several things: higher raw materials costs (Canadian softwood lumber) due to tariffs, slower output due to a shortage in construction workers combined with increased wages in the homebuilder's sector, rising mortgage interest rates, and a reduction in mortgage applications.

How Tax Law Changes Affect Value of Home Ownership

It may be time for your clients to re-evaluate the benefits.

BY Martin M. Shenkman & Alan Gassman

The 2017 Tax Act made a host of changes that apply to homeowners, with the primary impact being the loss of formerly available deductions for most clients. This changes the basic equation for many clients as to whether to buy a home, how much home they should own, how much to borrow and even whether they're better off renting their home to someone else. With respect to home tax benefits, much is different.

There are several general changes to the law that indirectly impact home ownership, such as the doubling of the standard deduction (and elimination of many itemized deductions), which is causing most taxpayers to not have any benefit from specific deductions for taxes, interest and other items on their personal income tax returns. The recent tax law changes may also exacerbate any significant downturn in housing prices, making things worse for homeowners.

Mortgage Interest

New, post-Act home mortgages will only be deductible for interest on up to $750,000 worth of debt. Prior law permitted deduction of interest on up to $1 million of home mortgages. Mortgages that existed prior to the Act are grandfathered, but if your client takes out a new mortgage, the lower limit may impact him.

Property Tax

The property tax deduction is greatly restricted. The acronym that's used is "SALT, which stands for state and local tax. SALT tax deductions have been capped at only $10,000 per person or married couple, and this amount won't be inflation indexed. This impacts clients who have more than $10,000 in combined personal state income tax, real estate and sales taxes and reduces the amount of itemized deductions that the taxpayer would have had towards exceeding the new high standard deduction, thus further restricting the number of taxpayers who can itemize deductions. Some wealthy property owners may set up special trusts and place income producing items into the trusts with real estate to allow for deducting $10,000 per trust per year for property taxes.

Itemized Deductions

Taxpayers can only deduct certain itemizable deductions if the sum thereof exceeds the "standard deduction," which is $12,000 for a single person and $24,000 for a married couple filing their income tax return jointly. The itemized deductions include charitable donations, interest expense real estate subject to the above caps, state and local income taxes also as limited above and medical expenses exceeding a specified percentage of the taxpayer's adjusted gross income. Some taxpayers will "bunch" deductions by making charitable donations and paying discretionary medical expenses and, to the extent feasible, real estate taxes every few years to exceed the standard deduction amount every other year. For example, your client might push 2018 deductions off to 2019 and in 2019, accelerate 2020 deductions by prepaying them if permissible.

Even if your client had, say, $10,000 in property tax, $10,000 in mortgage interest deductions and $2,000 in charitable deductions in a married filing joint situation, assuming no other deductions, your client is still going to have the standard deduction, which is $24,000 in 2018 for most married homeowners. Your client gets no incremental income tax benefit from all these expenses (including those for his home) as would have been the case under prior law, but your client might delay his charitable and real estate tax payments until 2019 and then pay $20,000 in real estate

taxes, $10,000 in interest and $4,000 in charity to endeavor to qualify for a $34,000 deduction instead of $24,000 in that year.

Casualty Loss

Casualty loss deductions have been greatly restricted or almost eliminated, unless the property is in a disaster zone declared by the federal government. Your client may want to consider reducing any deductibles on his homeowner casualty policy and increasing the maximum coverage to take into account that there may not be any tax benefits to help him in the event of a fire, flood or other situation.

Moving Expenses

Moving expenses are no longer deductible with a limited exception for military personnel when certain requirements are met.

Economics May Offset Tax Benefit Losses

Overall, these are all significant negatives tax ramifications for home ownership. But with the low present October 2018 unemployment rates and a growing economy, increasing home values and a hot stock market, many Americans may nonetheless be bullish on home ownership. This may change fast when the next recession happens, and at that time, more people will rent instead of owning because of the tax situation. This may more often be a lifestyle decision than a tax decision, but the average taxpayer will be able to afford less home than before because of the tax savings elimination.

Vacation Homes

Vacation homes are also negatively affected by all the Tax Act changes. So, there's certainly a greater out-of-pocket cost to having a vacation home.

Home Office Deductions

More homeowners will consider making sure that they qualify for the office deduction, which requires that the requirements of Internal Revenue Code Section 280A are met. There's certainly a greater incentive for your client to have his home-based business to allow a pro-rata portion of what might be otherwise non-deductible tax, interest and other expenses become deductible. So, if 20 percent of your client's home is used for your business, then 20 percent of his property taxes and other things may also be deductible.

Time to Re-evaluate

It may be time to re-evaluate your client's situation to determine his after-tax cost of home ownership and what he might do to improve his situation. This may mean renting instead of buying because your client's landlord can afford to give him a low rent thanks to the tax deductions she's receiving, converting his personal home to a rental, moving his business or part thereof into the home and possibly downsizing. Make sure that your client understands the economics of it before making a decision. Please remember that while the value of the median home in your client's area may have grown by 3.5 percent a year on average, these statistics don't take into account that your client's home gets older every year and therefore may lose part of its value and that your client's home will need a new roof, new air conditioning and other items that aren't counted in statistical average appreciation figures. While many Americans think that their homes have been their best investments, buy and hold diversified stock and mutual fund investments have more than doubled the rate of return over the past 60 years, and stocks and mutual funds don't need new roofs, or incur real estate taxes.

Medicare Plan Choices Require Study

By Kevin Stankiewicz

The Columbus Dispatch

The Medicare open enrollment period, which began last week, is an important time for all eligible adults to ensure that they find the right health-care plan.

But it's even more critical for those who have multiple chronic conditions, said Ken Thorpe, a professor of health policy at Emory University in Georgia and chairman of the Partnership to Fight Chronic Disease.

That's because their health-care needs mean they likely go to the doctor more frequently than others, Thorpe said, and require a significant number of drug prescriptions. If they end up in an inadequate Medicare plan, it could lead to a surprising amount of out-of-pocket spending, he said.

People with multiple chronic conditions also continue to make up a larger share of Medicare-eligible adults, placing them on the front lines in the battle to curb rising health-care costs in the United States. In 2015, more than half of Medicare patients had five or more chronic conditions - such as diabetes, high blood pressure, high cholesterol, pulmonary disease and back problems - and they accounted for three-fourths of Medicare spending, according to data provided by Thorpe.

In 1996, only a quarter of Medicare patients were in that category, and they represented a little more than half of Medicare spending, he said.

Consumers are offered a range of Medicare options, but that can make finding the right plan tricky, some say.

"It can feel very overwhelming," said Christina Reeg, director of the Ohio Senior Health Insurance Information Program (OSHIIP), an arm of the state Department of Insurance that offers education and guidance to Medicare beneficiaries.

When choosing a Medicare plan, people have to decide if they're going to enroll in original Medicare or a Medicare Advantage plan, offered by private insurers.

While they cover all the services original Medicare does, and sometimes more, Medicare Advantage plans have provider networks. That is especially critical for people with chronic conditions, Reeg said, because "typically they might have providers they don't want to give up."

So they should make sure their doctors would be "in network," she said. That isn't really a worry for those on original Medicare.

Another option to consider is a Special Needs Plan. A type of Medicare Advantage plan, these privately offered plans are tailored around the care someone with a specific condition such as HIV, dementia or cancer would need.

Most Medicare Advantage plans also include prescription drug coverage, but those choosing the original Medicare route will need to choose the best prescription drug plan - known as Part D - for their needs. It's an area where significant out-of-pocket costs could pile up, Thorpe said.

He recommends that Medicare beneficiaries list all the medications they're on and do an online comparison of the plans to find which would have the lowest out-of-pocket cost. There are 26 Part D plans offered in Ohio for 2019.

In addition to the services provided by OSHIIP, the Central Ohio Area Agency on Aging will be holding two educational workshops before enrollment closes Dec. 7. Medicare's website allows for plan comparison, as well. Coverage goes into effect Jan. 1.

Current Medicare enrollees should keep an eye out for updated cards being mailed during the enrollment window, Reeg said. Social Security numbers were removed from the cards in an attempt to reduce medical identity theft.

Taking time to research all available options reduces the chance of getting a hefty medical bill by surprise, Thorpe said.

"Consumers are generally just looking to see what they'd pay for a monthly premium, but that's probably not the biggest part of what they're going to end up paying," he said.

Central Ohio Area Agency on Aging's Medicare workshops begin at 2 p.m. on Wednesday and on Nov. 14 at the agency's office, 3776 S. High Street. Call 1-800-589-7277 to register.

|

Jacquelyn O'Brien. Jacquelyn is from Pittsburgh, Pennsylvania and in her third-year at Ohio State studying finance, with minors in economics and leadership studies. She serves on the finance branch of BuckeyeThon, the largest student-run philanthropy in the state of Ohio, and also serves as a peer financial coach through Scarlet and Gray Financial. Outside of school, she loves to bake, play tennis, and hang out with her nephews and niece! Go Bucks (... and Steelers)!

Jacquelyn O'Brien. Jacquelyn is from Pittsburgh, Pennsylvania and in her third-year at Ohio State studying finance, with minors in economics and leadership studies. She serves on the finance branch of BuckeyeThon, the largest student-run philanthropy in the state of Ohio, and also serves as a peer financial coach through Scarlet and Gray Financial. Outside of school, she loves to bake, play tennis, and hang out with her nephews and niece! Go Bucks (... and Steelers)!