|

Important Changes to Texas Property Product Offerings

Effective: Immediately

HOA South Carolina Agent,

We’re sharing several important updates to our Texas property product offerings that are now in effect. These changes are designed to support long-term product stability while continuing to offer competitive options for your clients across the state.

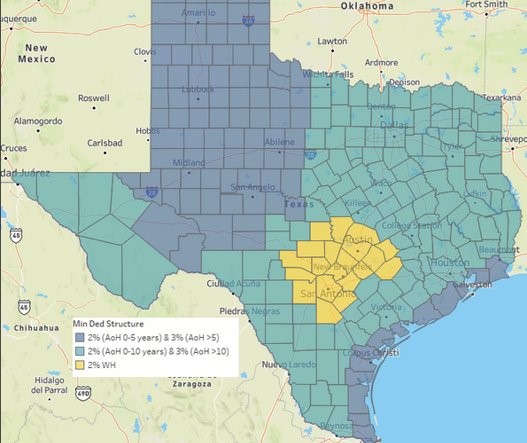

Revised TX Homeowners Minimum Wind/Hail Deductible (refer to map):

Tier 1 (Dark Gray) Counties:

- The HO Minimum Wind/Hail deductible remains at 3% of Coverage A for homes older than five years, and 2% of Coverage A for newer homes.

- Andrews, Aransas, Armstrong, Bailey, Baylor, Borden, Brazoria, Briscoe, Calhoun, Callahan, Cameron, Carson, Castro, Chambers, Childress, Cochran, Coke, Coleman, Collingsworth, Concho, Cottle, Crane, Crockett, Crosby, Dallam, Dawson, Deaf Smith, Dickens, Donley, Ector, Fisher, Floyd, Foard, Gaines, Galveston, Garza, Glasscock, Gray, Hale, Hall, Hansford, Hardeman, Hartley, Haskell, Hemphill, Hockley, Howard, Hutchinson, Irion, Jefferson, Jones, Kenedy, Kent, King, Kleberg, Knox, Lamb, Lipscomb, Loving, Lubbock, Lynn, Martin, Matagorda, McCulloch, Midland, Mitchell, Moore, Motley, Nolan, Nueces, Ochiltree, Oldham, Parmer, Pecos, Potter, Randall, Reagan, Refugio, Roberts, Runnels, San Patricio, Schleicher, Scurry, Shackelford, Sherman, Sterling, Stonewall, Sutton, Swisher, Taylor, Terrell, Terry, Throckmorton, Tom Green, Upton, Ward, Wheeler, Wilbarger, Willacy, Winkler, Yoakum.

Tier 2 (Yellow) Counties:

-

The HO Minimum Wind/Hail deductible reduced to 2% of Coverage A for homes of all ages.

- Atascosa, Bandera, Bastrop, Bexar, Blanco, Burnet, Caldwell, Comal, Fayette, Gillespie, Guadalupe, Hays, Kendall, Kerr, Lee, Llano, Medina, Travis, Williamson, Wilson.

Remainder of State (Teal):

- The HO Minimum Wind/Hail deductible increased to 3% of Coverage A for homes older than ten years, and 2% of Coverage A for newer homes.

Note: In all counties, the HO minimum AOP deductible remains at 1% of Coverage A.

|