|

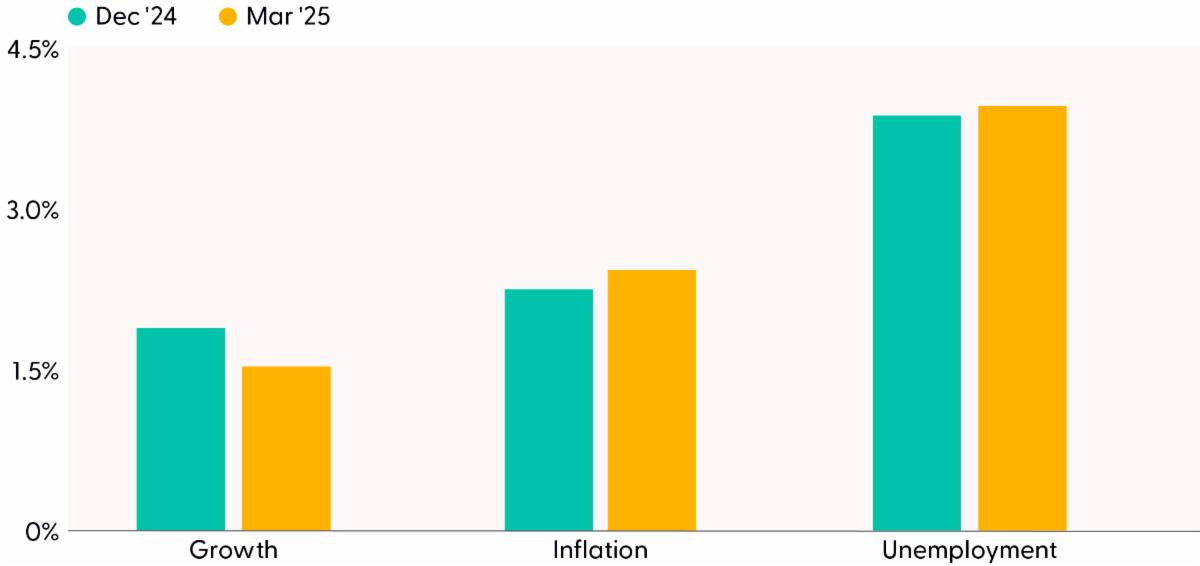

Source: LPL Research, Federal Reserve 03/24/25

Stagflation, a combination of low or no growth with persistent inflation, is not just a domestic risk. At the last meeting of Bank of England (BOE) officials, concerns across the pond are mounting about the same issues since trade wars benefit no one with impact across national boundary lines.

Investors were not surprised that the monetary policy-setting committee kept target rates unchanged. The committee is in the midst of policy fog as they await the repercussions from upcoming tariffs. And apparently, some companies have not waited until tariffs. According to the latest Beige Book, some firms have preemptively raised prices, creating some distortions with inflation data.

Despite this month’s inflation data having risks to the upside, we should expect core inflation to decelerate by the summer, in time for the Fed to cut in June.

The Hammer Award

Government jobs are often at risk when administrations get a fresh start. Perhaps most notable are the significant cuts to the federal workforce initiated by then-president Bill Clinton. The effort began after the National Performance Review initiative in March 1993. Over his eight-year term, Clinton reduced the federal workforce by approximately 380,000 jobs, which was about a 16% decrease. For those agencies able to improve efficiency and cut costs, Vice President Al Gore was gifted the symbolic “Hammer Award” in recognition of those efforts.

At that time, unemployment fell despite the cut in the federal workforce as the laid off workers were easily able to find new employment. Given the tight labor market currently, federal workers will not likely have any difficulty getting rehired, especially those with a professional degree. According to the Congressional Budget Office, total compensation for federal workers with a high school diploma, or less education, get 40% more than their private-sector counterparts. Government workers without a college degree are getting a premium, while those with professional degrees are working at a discount.1 To be sure, some monthly job reports could be soft but are unlikely to create any serious ripple effects across the job market.

Leading Indicators May Not Be Leading

So, how are consumers taking these developments, and what should we pay attention to? The Conference Board’s metric has remained below pre-pandemic levels since December 2022. Is this index no longer a signal, but just noise? Feelings — a.k.a. “consumer expectations” — continue to drive this index lower and have been a net drag since mid-2021. Apparently, the vibecession continues. The better component is the credit index, which tracks swap spreads, bank lending conditions, and debt balances at margin accounts. Conditions have improved recently.

The steady decline in new orders is a clear signal of a slowdown, and that signal started emerging in early 2022. Although, orders for nondefense core capital goods show stability.

Without a doubt, the economy started showing signs of a slowdown a while ago, and this metric is helpful in reminding investors of the fragility of business conditions. The two main risks globally are trade uncertainty and stagflation. These risks are not just in the U.S. but also in international economies, especially in the U.K. as highlighted in the latest press release from the BOE. Global investors should brace for heightened volatility as the global economy adjusts to the new regime.

A Potential Tailwind from Tax Policy

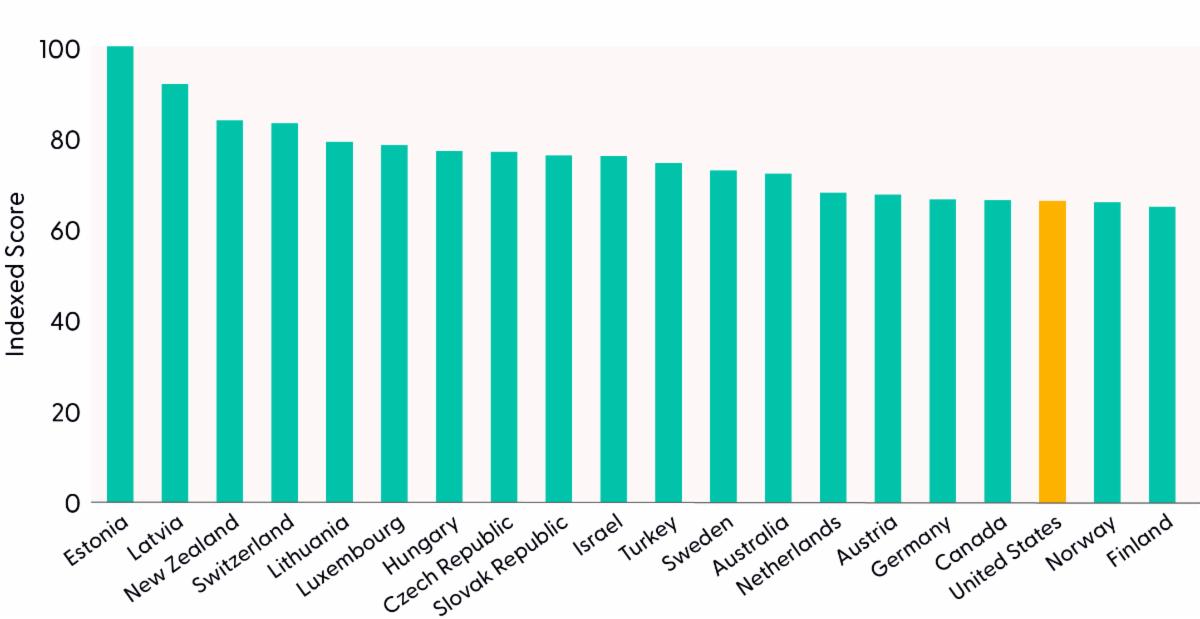

As this “new regime” takes shape, the U.S. has the opportunity to take advantage of change. In today’s globalized economy, the structure of a country’s tax system plays a crucial role in determining its economic performance. International tax competitiveness, which refers to how favorable a country’s tax policies are compared to others, can significantly impact both business and investment decisions. In times of economic slowdown, the policy response — which often includes monetary easing — should include business-friendly tax policies. Here’s why investors should carefully monitor for any progress on the tax front that lifts the U.S. from its 18th rank in tax competitiveness — currently behind other developed countries like Germany and Canada.

U.S. Must Look for Ways to Improve Competitiveness

|