|

1031 Remains under Fire

President's Budget Caps 1031 Deferral

Within the recently released President's 2015 budget is a proposal to limit gain deferral for real estate to $1 million per taxpayer per year (excerpt below).

This is another attack on IRC Section 1031. The justification for this proposal belies lack of understanding of the true benefits of �1031 exchanges.

Treasury Department "Green Book" Modifies the Like-Kind Exchange Rules for Real Property limiting the deferral to $1Million per taxpayer per year.-- "Pro small business rational."

Current Law

When capital assets are sold or exchanged, capital gain or loss is generally recognized. Under section 1031, however, no gain or loss is recognized when business or investment property is exchanged for "like-kind" business or investment property. As a result, the tax on capital gain is deferred until a later realization event, provided that certain requirements are met. The "like-kind" standard under section 1031, which focuses on the legal character of the property, allows for deferral of tax on the exchange of improved and unimproved real estate. Certain properties, including stocks, bonds, notes or other securities or evidences of indebtedness are excluded from non-recognition treatment under section 1031.

Reasons for Change

There is little justification for allowing deferral of the capital gain on the exchange of real property. The difficulty in valuing exchanged property is a primary historical justification for 1031 deferral. However, this rationale has limited appeal. For the exchange of one property for another of equal value to occur, taxpayers must be able to value the properties. In addition, many, if not most, exchanges affected by this proposal are facilitated by qualified intermediaries who help satisfy the exchange requirement by selling the exchanged property and acquiring the replacement property. These complex three party exchanges were not contemplated when the provision was enacted. They highlight the fact that valuation of exchanged property is not the hurdle it was when the provision was originally enacted. Further, the ability to exchange unimproved real estate for improved real estate encourages "permanent deferral" by allowing taxpayers to continue the cycle of tax deferred exchanges.

Proposal

The proposal would limit the amount of capital gain deferred under section 1031 from the exchange of real property to $1,000,000 (indexed for inflation) per taxpayer per taxable year. The proposal limits the amount of real estate gain that qualifies for deferral while preserving the ability of small businesses to generally continue current practices and maintain their investment in capital. Treasury would be granted regulatory authority necessary to implement the provision, including rules for aggregating multiple properties exchanged by related parties. The provision would be effective for like-kind exchanges completed after December 31, 2014.

Caution

Keep in mind that there has been NO bill introduced that would impact section 1031. 1031 CORP. will keep you advised if any bill is introduced. In the meantime, contact your Congressional leaders to let them know you think section 1031 is good for you and good for the economy.

|

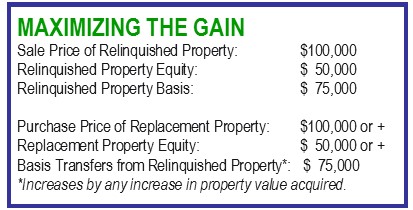

To Exchange or Not to Exchange

It's All in the Numbers

It's all or nothing! We have heard that many times when talking about 1031 tax-deferred exchanges. It refers to the misconception that you must acquire replacement property of equal or greater value or else the exchange will not work. While it is true that to maximize the tax deferral in a 1031 exchange one must acquire replacement property of equal or greater value and equity, one can trade down in either value or equity and pay tax on the difference. It's all or nothing! We have heard that many times when talking about 1031 tax-deferred exchanges. It refers to the misconception that you must acquire replacement property of equal or greater value or else the exchange will not work. While it is true that to maximize the tax deferral in a 1031 exchange one must acquire replacement property of equal or greater value and equity, one can trade down in either value or equity and pay tax on the difference.

While most taxpayers that initiate a 1031 exchange want to defer all of their gain, some are interested in trading down in property value or excluding a portion of the equity knowing full well that there will be a tax liability called "boot."

Another common misconception is that you only need to reinvest the gain. The fact is that your gain does not come into play when trying to maximize your tax deferral. It does come into play when trading down and unless you acquire replacement property that is greater than your tax basis, you will not defer any gain in a 1031 exchange. The higher the sale price of the replacement property, the greater the tax deferral. Read More

|

Trending this Month...

Inquiries Regarding Conversion of 1031 Replacement Property into Primary Residence

The number of calls and emails with questions regarding the transition from investment property to primary residence was up significantly in recent weeks. Learn more about the things to keep in mind when making the conversion. The number of calls and emails with questions regarding the transition from investment property to primary residence was up significantly in recent weeks. Learn more about the things to keep in mind when making the conversion.

|

Every Thursday, join us for one of our complementary Wealth Building Webinar Series sessions designed to help you build and preserve wealth. Register today!

April 3rd: 1031 Exchanges Made Easy

April 10th: Reverse & Improvement Exchanges: Preserving the Ability to Defer the Gain

April 17th: Advanced 1031 Exchange Topics

April 24th: 1031 Exchange as an Estate and Retirement Planning Tool

|

Our Margo McDonnell, CES� and Richard Heller, Esq., CCIM, CES� both have a number of upcoming continuing education courses for real estate professionals and attorneys scheduled at the Association of REALTORS� School in Malvern, PA.

Click on the course title below for dates, program descriptions and registration information.

1031 Tax-Deferred Exchanges presented by Margo McDonnell.

Taxation of Residential Real Estate presented by Rich Heller.

|

|

Message from our President

| | Margo McDonnell |

Dear Friends,

Yes, more concerning developments on the 1031 legislative front. However, please keep in mind that no bills have been introduced that would impact section 1031. In fact, 1031 exchange volume continues to pick up - not because there is concern that you may not be able to exchange after the end of the year - but because it makes sense and it is a great tax-strategy to help investors and business owners accomplish their goals.

Besides a full repeal of section 1031, the Camp Tax Reform Draft has many proposals that will negatively impact real estate owners. The National Association of REALTORS� has prepared an excellent summary of its impact on real estate. Now is the time to let your Congressional leaders know you oppose these proposals.

If you are considering a 1031 exchange, feel free to contact one of our Certified Exchange Specialists� with any questions or to discuss your transaction.

|

|

Please Join Us for

A Real Estate Spring Fling

Thursday, April 10th

Chart House, Philadelphia

6:00 - 9:00 PM

First Select Drink and Light Appetizers Included.

Drink specials.

CLICK HERE

SPONSORED BY:

1031 CORP.

Land Services USA

The Condo Shop

TD Bank

Astor Weiss Kaplan and Mandel, LLP

Voila Design

Robbini Bespoke

Wray's Touch Reflexology

|

|

Structured Sales Offer 1031 Alternative

Tax-Deferral Strategy Opens New Options

A  "Structured Sale" is an improved version of the traditional installment sale provisions in IRC �453. Instead of receiving a lump sum cash payment upon the sale of the property, the seller receives installment payments spread over a number of years and the gain is deferred over the life of the note with taxes only due when payments are received. A Structured Sale combines the security of a cash sale with the tax benefits of an installment sale. "Structured Sale" is an improved version of the traditional installment sale provisions in IRC �453. Instead of receiving a lump sum cash payment upon the sale of the property, the seller receives installment payments spread over a number of years and the gain is deferred over the life of the note with taxes only due when payments are received. A Structured Sale combines the security of a cash sale with the tax benefits of an installment sale.

Read more about Structures Sales

|

|

About 1031 CORP.

Serving as a nationwide qualified intermediary for 1031 tax-deferred exchanges since 1991, 1031 CORP. strives to provide a superior exchange experience for our customers and their advisors. We provide our customers with enhanced security of funds, knowledgeable exchange professionals and a commitment to keep the exchange process simple for our customers and their advisors. Every member of the exchange team is a Certified Exchange Specialist� and has the experience and expertise to facilitate even the most complex exchange transaction, including reverse, improvement and personal property exchanges. Additional information can be found at www.1031CORP.com. |

|

|

Margo McDonnell, CES�

Certified Exchange Specialist�

President

1.800.828.1031 ext. 212

Mobile: 610.680.6896

|

|

Sue Umstead, CES�

Certified Exchange Specialist�

Senior Vice President

1.800.828.1031 ext. 208

Mobile: 610.755.8520

|

|

Marissa LoCascio, CES�

Certified Exchange Specialist�

Senior Exchange Officer

1.800.828.1031 ext. 210

Mobile: 610.742.4351

|

|

Richard Heller, Esq., CCIM, CES�

Consultant

1.800.734.1031

|

|

Bettye J. Matthews, CPA

Consultant

1.800.680.1031

|

|

Joseph F. Szajnecki, CES�

Consultant

1.800.734.1031 |

|

2013 Exchange Reporting Guide

Download our 2013 Exchange Reporting Guide here for information on reporting your 1031 exchange, when to file your tax return, when to file for an extension and other important tax reporting assistance!

Helping you simplify the reporting of your 1031 exchange!

|

Interested in stayingup to date with Marcellus Shale? Interested in stayingup to date with Marcellus Shale?

|

|

Not a Subscriber? Interested in receiving our Exchanging Times newsletter each month?

Follow 1031 CORP.

"LIKE" 1031 CORP. on Facebook to receive a daily tidbit on 1031 exchanges and related topics.

|

|