|

|

Registered Investment Advisor

95 Broadhollow Road, Suite 102

Melville, NY 11747

(631) 923-2485

|

|

Investment Newsletter - Q2 2022 |

|

Greetings!

Three sayings come to mind recently:

"History doesn't repeat itself, but often rhymes", "It's deja vu all over again", and "Don't keep worrying about the world coming to an end - it will only happen once".

The reason we think of the first saying is simply the latest catalyst that has sparked the recent volatility is the war with Ukraine, that almost no one thought would happen just a few months ago. Regrettably, there are always going to be things that are unexpected that will suddenly occur, and quickly roil the markets. History has plenty of examples, such as the Covid-19 pandemic (and earlier as well as future pandemics); the housing/financial crisis; 9/11; Cuban Missile Crisis; assassinations and assassination attempts (an attempt on both Ronald Reagan and the Pope occurred in the same year); and so on.

That leads into the second saying of "It's deja vu all over again", because we often see the same thing, and as such we give the same responses as we have in the past. In our "Investment Topic" below, we will share the why that we (and most everyone else in the field) give the same responses to market volatility time after time.

The last comment on not worrying about the world coming to an end while may be a bit tongue in cheek, it is accurate because if and when that happens, there really is nothing at that point to worry about! Up until then though, no matter how terrible things may be, contrary to what some worry about the stock market will not go to zero, nor will the majority of the companies go bankrupt. People will still need to buy food, goods, and services no matter how tough things get. At worst, they may delay purchases, or not buy luxury items, but people will still need to eat, heat their homes, get medical treatment, put gas in their cars, etc. Also while they may put off buying new items, eventually items need to be replaced, so goods (and services), will need to be consumed regardless.

As Charles M. Schulz said: "Don't worry about the world coming to an end today. It's already tomorrow in Australia". Seriously though, if you are concerned about what current (or future) events means and if it will affect your financial future, we are always available to go over things in detail with you.

We give you a deeper insight into our thoughts on the past quarter and outlook further below. If you would like, we also have a link to the Q2 2022 Global Market Outlook by Russell Investments. Click here to access the short executive summary, or click here to access the more in-depth commentary. .

In this issue of our Investment Newsletter:

- Our current investment topic is: Volatility - What You Need to Know

- Recent articles where Landmark Wealth Management was quoted in the press.

- An overview of recent market activity, along with Our Perspective...

- A recap of the performance of major market indices from the past quarter

- Upcoming Economic Calendar

You will find past investment articles, by clicking the Articles tab above, or directly on our website, found under Periodicals.

If there is a topic of interest you would like to see covered in the future, please reply back to this email to let us know, or click here. Likewise, if you have any questions on this or anything else, feel free to reply back.

|

|

Investment Topic

Volatility - What You Need to Know

For our investment topic, we thought it important to show how volatility is something to be expected, and what history has shown us. Some of this information we believe will be eye-opening to many.

A picture is worth a thousand words, so we will use one page charts and slides to show key points on this subject.

As it is said, history doesn't always repeat, but often rhymes. We don't know the final outcome of the Russia/Ukraine situation, but the world has dealt with similar issues in the past and markets still went up over time. Click here to see a snapshot.

If you look at the market with a long-term lens, you can see that despite all of the negative headlines since the beginning of the financial crisis in 2007, the market has continued to grow and build wealth for those that stayed the course. Click here for a detailed chart.

As you can see from this slide, on the worst single days since 1960, extreme volatility is often followed by strong recoveries. Click here for the slide.

How long has it taken to recover in past market corrections? Historically, not too long. Click here to see.

The U.S. has experienced 26 bear markets since 1929. Our recovery record? 26 for 26. While we can't predict the future, as Warren Buffet has said, "It has never paid to bet against America". Click here to see a chart of Bull and Bear markets going back the past 80 years.

|

|

Recent articles where Landmark Wealth Management was quoted in the press

The past few years, Landmark Wealth Management has been quoted in the press for various articles. We have decided to start sharing these when they happen. If curious about past times we were mentioned, you can see it on our website under Articles > In The Press, or simply click here.

"5 expert tips for 20-somethings who want to invest but don't know where to start"

From an article that was on the website Business Insider, we thought you may find this story of interest:"5 expert tips for 20-somethings who want to invest but don't know where to start". To access this article, please click here.

"Russia-Ukraine conflict may mean higher prices on LI, economists say"

From an article that was originally printed in Newsday this December, we thought you may find this story of interest: "Russia-Ukraine conflict may mean higher prices on LI, economists say". To access this article, please click here.

|

|

Our Annual ADV

As per Securities and Exchange Commission (SEC) requirements, attached is our annual ADV brochure. To access this, please click here. If you would like us to email or mail a hard copy, please feel free to call/email us to let us know.

|

|

Our Perspective on Recent Market News and Activity |

|

Our synopsis of the past quarter, a look ahead, and putting it all in perspective: |

|

In our last newsletter, heading into 2022 we stated, “The prevailing consensus is that there are some headwinds”. We went on to discuss that the Federal Reserve was looking to tighten and raise interest rates and gave some overall market commentary. Well, as often can happen, the headwinds only grew and the markets were faced not only with rising interest rates, but also added in was a 180-degree pivot from the Fed from being dovish into being more hawkish, inflation levels that we have not seen in the last 40 years, and war in Europe not seen to this extent since World War II. If you add in another COVID delta variant and continued supply chain shortages, the markets and investors have had a lot absorb so far year to date. Time will resolve each of these issues, however undoubtedly there will also be new issues that appear down the road. As Billy Joel sang, “We didn’t start the fire, it was always burning, since the worlds’ been turning”.

We will get through this difficult period and better times are always just around the corner. It is of note however that this appears to be a fundamental shift away from a Fed that seemingly has had the markets back as some would call a “Fed put”, into a Fed that will need to be less accommodative to the markets, at least for the short-term or unless things were to take a severe turn downwards. With all of this “noise” the markets finished their worst quarter in the last 2 years.

So, what does one do in times like these? You stick to the plan. As they say, “History does not repeat itself, but if often rhymes”. If you break out each of the current market headwinds, we have historical context to times in history where the markets have been faced with such issues.

The dramatic increase in the M2 money supply over the last 2 years is a bit unprecedented, and that is a bit of a unique aspect to some of the inflationary challenges that we are currently witnessing. We have had very high inflation in the late 1970’s-early 1980’s. We have had wars to review how markets have reacted. We have had global pandemics to learn from. We have experienced periods of time when the Fed has tightened and we have seen how the markets have reacted in the past. As they always say, “past performance is not a guarantee of future performance”, however as we said history often rhymes. One might be surprised as to how the equity markets performed during the mid-1970’s to early 1980’s period of high inflation? Here are the numbers:

1975 Inflation 9.14% S&P 500 +23.84% 1976 Inflation 5.74% S&P 500 +23.84%

1977 Inflation 6.5% S&P 500 -7.18% 1978 Inflation 7.63% S&P 500 +6.56%

1979 Inflation 11.25% S&P 500 +18.44% 1980 Inflation 13.55% S&P 500 +32.42%

1981 Inflation 10.33% S&P 500 -4.91% 1982 Inflation 6.13% S&P 500 +21.41%

The equity markets are off of their February 24th lows, but most asset classes still remain negative year to date. The bond market has had a very difficult year so far, with the market factoring in another 6 more interest rate increases in 2022 after the 0.25% increase already done in March. Historically, the stock market is positive on average about 75% of all years. The bond market is positive in about 90% of all years. When you put those two asset classes together into a balanced type of mix, the results are positive about 80% of all years. Coming off 3 straight positive years, it is very possible that 2022 may just not be a positive year. Long term Investors must understand and accept this, with the recognition that the markets inevitably move through cyclical periods. Long- term assets move up over time and allows one to grow their assets in a manner that has historically helped investors to sustain a rate of withdrawal from their assets to help those assets last through retirement, while offsetting the effects of taxes and inflation over time.

Inflation is a big concern at present. The Consumer Price Index (CPI) is up 7.9% from a year ago, and economists think it will likely peak in the 8.5-9% range sometime in the next couple of months. This is the highest level since 1981. There are a lot of arguments about the causes of this inflation, but ultimately it comes down to just too much money creation over the last two years. The Fed has its work cut out to get inflation back down to more acceptable levels, and a soft landing appears to be a difficult one for them to pull off.

For our more conservative investors, with the effects that rising interest rates have had on bond prices has been difficult and is undoubtedly causing some angst. It was actually the US bond markets worst quarter in more than 40 years!

Hang in there, as we said in our last newsletter, the transition from lower rates to higher rates comes with some short-term pain. Going forward you will start to receive higher interest payments from your bonds which can ultimately lead to not having to take as much risk in a portfolio in an effort to obtain a higher overall rate of return. We do not know when the Fed will be finished raising rates, however a good portion of the expected 2022 future rates have already been factored into current bond prices.

For our investors who have higher percentages in stocks vs. bonds, the decline so far YTD has been nothing out of the norm vs. other periods of corrections. As we have often pointed out, the average intra-year decline for the S%P 500 over the last 40 years has been about 14% from a high to a trough in any given year, and we don’t think this year will be much different than most of those years. As always, we are here for you. If you have concerns, would like to revisit your own personal financial plan, we always welcome the opportunity to meet either in person, phone or Zoom to give you our thoughts and perspectives.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

|

|

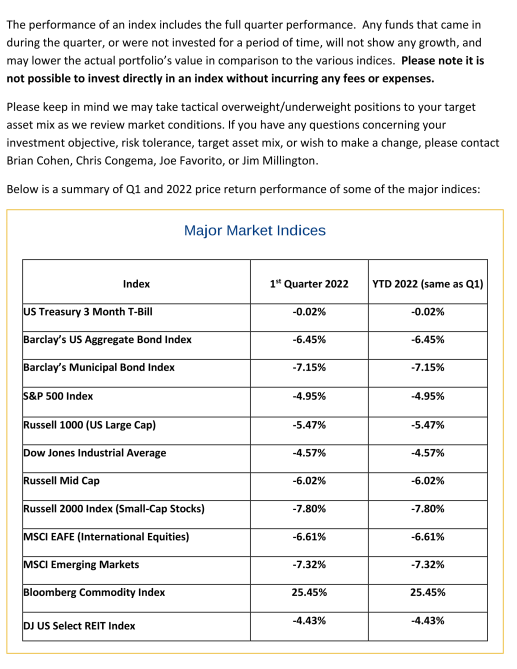

Below is the Q1 '22 price return performance of some of the major indices: |

|

On the Investment Horizon |

|

Upcoming Key Dates on the Economic Calendar

- First Friday of each month: Unemployment report for the prior month, released at 8:30AM.

- Wednesday, April 6 - Federal Open Market Committee (FOMC) releases minutes of previous meeting at 2PM.

- Friday, April 15 - Good Friday: US Markets closed.

- Thursday, April 2 at 8:30AM - GDP, 1st quarter (advance estimate).

- Tuesday, May 3 - Wednesday, May 4: The Federal Open Market Committee (FOMC) meets, and releases their announcement on Wednesday at 2PM.

- Wednesday, May 25 - Federal Open Market Committee (FOMC) releases minutes of previous meeting at 2PM.

- Monday, May 30 - Memorial Day: US Markets closed.

- Thursday, May 26 at 8:30AM - GDP, 1st quarter (second estimate).

- Tuesday, June 14 - Wednesday, June 15: The Federal Open Market Committee (FOMC) meets, and releases their announcement on Wednesday at 2PM.

- Wednesday, June 29 at 8:30AM - GDP, 1st quarter (third estimate).

- Monday, July 4 - Independence Day: US Markets closed.

|

|

For our clients - You should have received your statement directly from your account custodian (TD Ameritrade and/or Charles Schwab). If you have not, please let us know so that we may investigate the matter. Please review your statement carefully and let us know if you have any questions or comments.

Also, as a reminder, we have moved to a new office, with a nice sized conference room to use for our meetings and updates. If you do not feel comfortable coming into our office, we recommend that we possibly set up a Zoom or teleconference call to update your planning numbers, especially if it has been more than a year since we have last done so. Please feel free to reach out.

For everyone - If you desire an appointment, have any questions on any of this material, or any other financial subjects may relate to your own financial circumstance, please reach out to us at the contact information below:

Sincerely,

Direct phone: 631-923-2485

This communication is from Landmark Wealth Management, LLC, a Securities and Exchange Commission Registered Investment Advisory firm. The information in this email is not intended as tax or legal advice, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek tax, legal, or investment advice from an independent professional / financial advisor. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Information and use of materials contained in this email, including text and attachments, is confidential and is for the use of the intended recipient(s) only. If received in error, you are hereby notified that any dissemination, distribution, or copying of this communication, or any of its contents, is strictly prohibited. If you have received this communication in error, please reply to the sender and delete the original message and any copy of it from your systems. Be also advised that email communications are not secure. All e-mail sent to or from this address will be recorded by the Landmark Wealth Management, LLC email system and is subject to archival, monitoring, and inspection pursuant to securities regulations. Please direct any matters regarding this policy to [email protected].

|

|

|

|

Landmark Wealth Management, LLC

95 Broadhollow Road, Suite 102

Melville, NY 11747

(631) 923-2485

|

|

|

|

|

|

|