|

|

Registered Investment Advisor

95 Broadhollow Road, Suite 102

Melville, NY 11747

(631) 923-2485

|

|

Investment Newsletter - Q3 2021 |

|

Greetings!

As always, we hope this finds you well. We want to let everyone know that we have just moved our main location in Melville. We are still on Route 110, about a half mile south of where we used to be. A picture of the office building is on the right, and there is more information about the move a little further below.

In regards to the new office, we have a nice sized conference room to use for our meetings and updates. If you do not feel comfortable coming into our office, we recommend that we possibly set up a Zoom or teleconference call to update your planning numbers, especially if it has been more than a year since we have last done so. Please feel free to reach out.

Regarding the economy and the stock market, we give you our thoughts, specifically on the past quarter and outlook further below. If you would like, we also have links to the Q3 2021 Global Market Outlook by Russell Investments, one being a detailed report, and the other an "Executive Summary". To access either of those, please click here*. *Please note, when you click, you may need to wait about 5 seconds for the screen to load, and then scroll and click the url underneath the Russell Investments picture.

In this issue of our Investment Newsletter:

- Our current investment topic is: Cryptocurrency: What is the Value?

- We have moved our main location - still in Melville, just down the road

- Access to our updated ADV brochure (updated due to our move)

- An overview of recent market activity, along with Our Perspective...

- A recap of the performance of major market indices from the past quarter

- Upcoming Economic Calendar

You will find past investment articles, by clicking the Articles tab above, or directly on our website, found under Periodicals.

If there is a topic of interest you would like to see covered in the future, please reply back to this email to let us know, or click here. Likewise, if you have any questions on this or anything else, feel free to reply back.

|

|

Investment Topic

For our investment topic, "Cryptocurrency: What is the Value?" we attempt to give a high-level overview of the topic. To learn more, please click here.

|

|

We have relocated our main office

Landmark Wealth Management is pleased to announce that we have moved our main location in Melville, about a half mile south on Route 110, to 95 Broadhollow Road, Suite 102.

|

|

We are extremely excited about the move, for a number of reasons. In addition to staying in the same general vicinity where it is convenient for many people, our larger space has enough offices not only for Brian, Chris, Joe, and Jim, but also for the possibility of future growth as well. Besides the space being larger and more of a contemporary look and feel, it also has the benefit of a conference room that we can utilize whenever it is needed. |

|

Our new location also is similar to where we have been in Melville with parking that is close to the entrance, and we now are on the ground floor. For those that are on or close to Long Island, we look forward to your seeing our new location! |

|

Our updated ADV

As per Securities and Exchange Commission (SEC) requirements, attached is our updated ADV brochure, that reflects our new address. To access this, please click here. If you would like us to email or mail a hard copy, please feel free to call/email us to let us know.

|

|

Our Perspective on Recent Market News and Activity |

|

Our synopsis of the past quarter, a look ahead, and putting it all in perspective with some additional commentary from Brian Wesbury, Chief Economist at First Trust: |

|

We ended our last quarterly newsletter with the following statement, “Be safe and healthy, the finish line is hopefully approaching on this pandemic. The wish for our next newsletter is that you are all too busy on vacation to even think about the markets!” We understand that may have sounded overly optimistic, however we have seen tremendous progress in dealing with the COVID-19 virus. We know that the end is not yet here, however we do know that many of our clients are starting to get back to life as we once knew it. Nothing makes us happier than listening to our clients asking us to model into their financial plans increased travel and on other things such as concerts, ballgames, etc. What a painful lesson that we all learned on how to really appreciate the things in life that we previously just took for granted.

As for the stock market, it has continued to show confidence that things are and will be improving and it was another positive quarter of returns this past quarter for equities.

What is the market concerned about going forward? All eyes are on the Federal Reserve and Jerome Powell. Do they successfully navigate their way through a re-opening economy, or do they make a policy mistake which could lead to a next recession? The Federal Reserve is still holding interest rates near 0% and buying $120 billion worth of bonds every month, as if the US were still in a financial crisis.

When it comes to short-term interest rates, the “dot plot” from the Fed now shows seven policymakers in favor of at least one 25 basis point rate hike in 2022, up from only four policymakers back in March. While those seven are still a minority of Fed policymakers, that was not the case for the following year. For 2023, a majority of policymakers – thirteen of eighteen – think the Fed will raise interest rates versus only seven of eighteen back in March. Moreover, the “median dot” now suggests the Fed would raise rates twice (for a total of 50 bp) in 2023.

In addition, according to Chairman Jerome Powell, the Fed is now officially “talking about talking” about tapering its balance sheet purchases. For the time being it will keep buying a total of $120 billion in Treasury and mortgage securities per month and Powell made it clear at the press conference that the Fed will only start tapering after it provides notice “as far in advance as possible.” We think that notice will be provided by this Fall, with tapering starting by the beginning of 2022, maybe sooner.

The key problem with the labor market right now is that the government is still giving out unemployment benefits far in excess of what the situation demands. Sending out these jobless benefits might have made sense in the early days of the pandemic, back when the government’s shutdown-heavy response to COVID-19 amounted to a “taking” of many people’s businesses and livelihoods. That was an incredibly unusual situation. Some think it was a mistake while others felt if the government “takes” away your job for public health reasons, it’s logically consistent to “compensate” you for it. In the meantime, the system is awash in money. This lifts asset values, in spite of problems in the labor market. Moreover, interfering with the dynamics of the labor market reduces output while increasing consumption, which is a recipe for inflation.

The Fed has said it thinks the inflation surge, at least when looked at on a year-over-year basis, is overstated because it is built on comparisons to a period when prices were falling during the onset of the COVID-19 crisis. They also think any recent pressures are “transitory,” caused by supply-chain issues that should go away as the economy continues to recover.

Meanwhile, it has discounted extremely rapid growth in the M2 measure of the money supply. Because central banks around the world have introduced Quantitative Easing in the past decade, with no pick-up in inflation, the Fed thinks any link between money and prices has been broken…Jerome Powell even said we should “unlearn” this idea that money growth causes inflation.

Clearly, the Fed is dismissing the surge in inflation this year and Fed forecasts show that it expects inflation to fall back down to its 2.0% target in 2022 and beyond.

Where does this leave investors? As we always tell our clients, while this may make for interesting conversation and discussion, as a long-term investor it should not cause for any meaningful diversion from a long-term plan. A well-diversified, and properly asset allocated portfolio should be built to withstand whatever the markets throw at us over a full market cycle. If you have not met with us in a while, please set an appointment and come see us! At the very least we would like to show you our new office, but more than that we want to make sure your planning numbers are current and up to date.

Wishing you all an enjoyable summer. Our job is to watch, monitor and act on your behalf, and for that we always appreciate your confidence, trust, and loyalty. Enjoy!

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

|

|

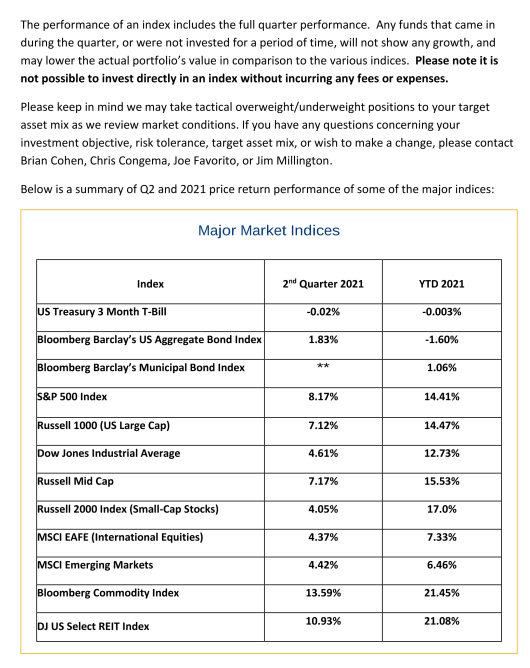

Below is the Q2 '21 price return performance of some of the major indices: |

|

On the Investment Horizon |

|

Upcoming Key Dates on the Economic Calendar

- First Friday of each month: Unemployment report for the prior month, released at 8:30AM.

- Monday, July 5 - Independence Day observed: NYSE closed.

- Wednesday, July 7 - Federal Open Market Committee (FOMC) releases minutes of previous meeting at 2PM.

- Tuesday, July 27 - Wednesday, July 28: The Federal Open Market Committee (FOMC) meets, and releases their announcement on Wednesday at 2PM.

- Thursday, July 29 at 8:30AM - GDP, 2nd quarter (advance estimate).

- Wednesday, August 18 - Federal Open Market Committee (FOMC) releases minutes of previous meeting at 2PM.

- Thursday, August 26 at 8:30AM - GDP, 2nd quarter (second estimate).

- Monday, September 6 - Labor Day: NYSE closed

- Tuesday, September 21 - Wednesday, September 22: The Federal Open Market Committee (FOMC) meets, and releases their announcement on Wednesday at 2PM.

|

|

If you desire an appointment, have any questions on any of this material, or any other financial subjects may relate to your own financial circumstance, please reach out to us at the contact information below:

Sincerely,

Direct phone: 631-923-2485

This communication is from Landmark Wealth Management, LLC, a Securities and Exchange Commission Registered Investment Advisory firm. The information in this email is not intended as tax or legal advice, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek tax, legal, or investment advice from an independent professional / financial advisor. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Information and use of materials contained in this email, including text and attachments, is confidential and is for the use of the intended recipient(s) only. If received in error, you are hereby notified that any dissemination, distribution, or copying of this communication, or any of its contents, is strictly prohibited. If you have received this communication in error, please reply to the sender and delete the original message and any copy of it from your systems. Be also advised that email communications are not secure. All e-mail sent to or from this address will be recorded by the Landmark Wealth Management, LLC email system and is subject to archival, monitoring, and inspection pursuant to securities regulations. Please direct any matters regarding this policy to [email protected]

|

|

|

|

Landmark Wealth Management, LLC

95 Broadhollow Road, Suite 102

Melville, NY 11747

(631) 923-2485

|

|

|

|

|

|

|