|

|

Registered Investment Advisor

95 Broadhollow Road, Suite 102

Melville, NY 11747

(631) 923-2485

|

|

Investment Newsletter - Q4 2021 |

|

Greetings!

As we all get a little bit older, of course time goes faster and faster. This summer was no exception. It seems like we were just wishing you all a happy summer and to hopefully enjoy it as much as possible and now we are already in fall. Another year, flying by! We are looking forward to a stronger Q4 and wishing you all to be safe and healthy.

For our clients, as a reminder, we have moved to a new office, with a nice sized conference room to use for our meetings and updates. If you do not feel comfortable coming into our office, we recommend that we possibly set up a Zoom or teleconference call to update your planning numbers, especially if it has been more than a year since we have last done so. Please feel free to reach out.

Regarding the economy and the stock market, we give you our thoughts, specifically on the past quarter and outlook further below. If you would like, we also have links to the Q4 2021 Global Market Outlook by Russell Investments, one being a detailed report, and the other an "Executive Summary". To access either of those, please click here*. *Please note, when you click, scroll and click the url underneath the Russell Investments picture, and the pdf should download automatically.

In this issue of our Investment Newsletter:

-

Our current investment topic is: Inflation Concerns Heading into 2022

-

Our investment topic is "Inflation Concerns Heading into 2022".

- A recent article that Landmark Wealth Management was quoted in the press: "Have bitcoin dreams? What to know about the hype, the reality and the future of cryptocurrencies"

- An overview of recent market activity, along with Our Perspective...

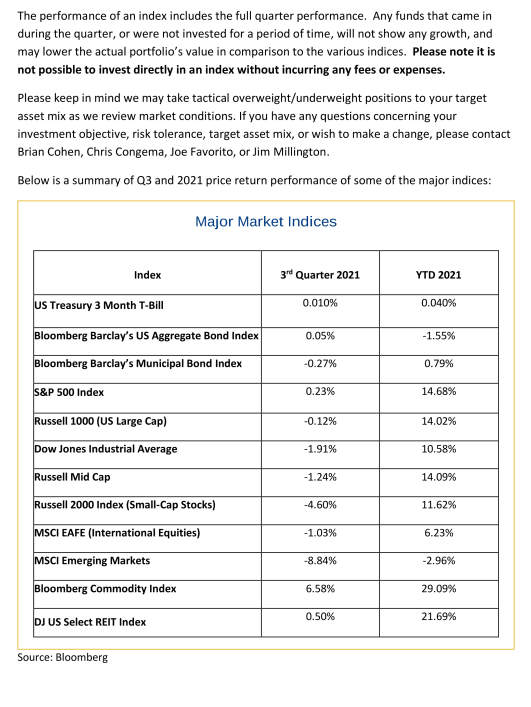

- A recap of the performance of major market indices from the past quarter

- Upcoming Economic Calendar

You will find past investment articles, by clicking the Articles tab above, or directly on our website, found under Periodicals.

If there is a topic of interest you would like to see covered in the future, please reply back to this email to let us know, or click here. Likewise, if you have any questions on this or anything else, feel free to reply back.

|

|

Investment Topic

Inflation Concerns Heading into 2022

For our investment topic, Inflation Concerns Heading into 2022 we give a high-level overview of the topic. To learn more, please click here.

|

|

Recent articles where Landmark Wealth Management was quoted in the press

The past few years, Landmark Wealth Management has been quoted in the press for various articles. We have decided to start sharing these when they happen. If curious about past times we were mentioned, you can see it on our website under Articles > In The Press, or simply click here.

From an article that was originally printed in Newsday this August, we thought you may find this story of interest: "Have bitcoin dreams? What to know about the hype, the reality and the future of cryptocurrencies". To access this article, please click here.

|

|

Our Perspective on Recent Market News and Activity |

|

Our synopsis of the past quarter, a look ahead, and putting it all in perspective: |

|

The third quarter was a bit of a lackluster quarter, primarily dampened down by a coolish September. No surprise, markets simply do not go up each month, each quarter, and each year. That being said, the market is still having a good year overall and sometimes it just needs to adjust a bit given the fact that the “market was a little too far over its skis”.

As you can see by the market indices summary, YTD returns for equities are all positive, while bonds have not fared as well with municipal bonds basically flat and corporate bonds slightly negative YTD.

Inflation has certainly been in the spotlight as of late, and you can access a recent article we just posted on our website under the Articles tab on our website. Fed Chair Powell recently testified before Congress and basically said that inflation is likely to stay high in the coming months before moderating. He also indicated the Fed was likely to begin reversing its easy-money policies at its next meeting, November 2-3rd by tapering its $120 billion in monthly asset purchases and complete that process by the middle of next year. A surge in inflation due to supply-chain bottlenecks, combined with other challenges related to the reopening of the economy has been larger and a bit longer lasting than anticipated. He also said that the supply chain disruptions will abate and as they do, inflation is expected to drop back toward the Fed’s 2% goal. He did also acknowledge that there are some risks that price pressures are higher than anticipated or more enduring, and if that does occur the Fed would raise interest rates “if sustained higher inflation were to become a serious concern”.

The Delta variant of Covid-19 appeared to temper economic growth this summer, however economists expect the recovery from the pandemic to reaccelerate as the virus’s toll eases. Over the last few weeks, many economists had lowered their forecasts for 3rd quarter economic growth in large part due to consumers slowing down spending on hotels and airline tickets, and meals out with the spread of the highly contagious Delta variant. The Delta surge also complicated office and school reopening’s, which turned what had been an expected September boom into a downturn. However, at present the recovery is still on solid footing, and just as robust as we saw in the first half of the year. Many economists have raised their growth forecasts for next year, under the premise that some spending and production have been delayed by the Delta surge and supply chain disruptions, but it is not lost for good. There are early signs that the spending slowdown is bottoming out as Covid-19 cases decline.

Covid-19 cases are likely to keep falling, according to projections from the Centers for Disease Control and Prevention. If they do, American households could tap into a record $142 trillion in net worth and ramp up spending on in-person services, economists say. Consumer spending is the biggest driver of U.S. economic growth. Some economists expect growth to reaccelerate after the 3rd quarter. The U.S. economy is far from fully healed from the Covid-19 disaster, but now that the government has stepped back from extra large payments to the unemployed, many think that the labor market is on the verge of a big step forward. As long-term investors, we absorb this news but do not overreact to short term volatility.

Fall represents a great time to start planning for the new year. Open enrollment on health plan coverage in most states runs from November 1 and will continue through January 2022. Please use this time to evaluate your current coverages and if you need any help in this regard, please just let us know. If it has been a while since you have met with us either via a Zoom call or in person appointment, we encourage you to set an appointment with us to go over your financial planning numbers.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

|

|

Below is the Q3 '21 price return performance of some of the major indices: |

|

On the Investment Horizon |

|

Upcoming Key Dates on the Economic Calendar

- First Friday of each month: Unemployment report for the prior month, released at 8:30AM.

- Monday, October 11 - Columbus Day: US Bond Markets closed, NYSE is open.

- Wednesday, October 13 - Federal Open Market Committee (FOMC) releases minutes of previous meeting at 2PM.

- Thursday, October 28 at 8:30AM - GDP, 3rd quarter (advance estimate).

- Tuesday, November 2 - Wednesday, November 3: The Federal Open Market Committee (FOMC) meets, and releases their announcement on Wednesday at 2PM.

- Thursday, November 11 - Veterans Day: US Bond Markets closed, NYSE is open.

- Thursday, November 24 at 8:30AM - GDP, 3rd quarter (second estimate).

- Wednesday, November 24 - Federal Open Market Committee (FOMC) releases minutes of previous meeting at 2PM.

- Thursday, November 25 - Thanksgiving Day: US Markets closed.

- Friday, November 26 - Day after Thanksgiving, US Markets close early.

- Tuesday, December 14 - Wednesday, December 15: The Federal Open Market Committee (FOMC) meets, and releases their announcement on Wednesday at 2PM.

- Friday, December 24 - Christmas Day observed: US Markets closed.

- Monday, January 2 - New Year's observed: US Markets closed.

|

|

If you desire an appointment, have any questions on any of this material, or any other financial subjects may relate to your own financial circumstance, please reach out to us at the contact information below:

Sincerely,

Direct phone: 631-923-2485

This communication is from Landmark Wealth Management, LLC, a Securities and Exchange Commission Registered Investment Advisory firm. The information in this email is not intended as tax or legal advice, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek tax, legal, or investment advice from an independent professional / financial advisor. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Information and use of materials contained in this email, including text and attachments, is confidential and is for the use of the intended recipient(s) only. If received in error, you are hereby notified that any dissemination, distribution, or copying of this communication, or any of its contents, is strictly prohibited. If you have received this communication in error, please reply to the sender and delete the original message and any copy of it from your systems. Be also advised that email communications are not secure. All e-mail sent to or from this address will be recorded by the Landmark Wealth Management, LLC email system and is subject to archival, monitoring, and inspection pursuant to securities regulations. Please direct any matters regarding this policy to [email protected]

|

|

|

|

Landmark Wealth Management, LLC

95 Broadhollow Road, Suite 102

Melville, NY 11747

(631) 923-2485

|

|

|

|

|

|

|