|

|

Registered Investment Advisor

95 Broadhollow Road, Suite 102

Melville, NY 11747

(631) 923-2485

|

|

Investment Newsletter - Q4 2022 |

|

Greetings!

The market has not turned around yet and that is due to a number of factors: inflation concerns, the Fed raising rates to combat inflation, ongoing supply chain issues (which has been a "fuel" of sorts that has spurred inflation), and all this has led to a concern of an upcoming recession.

As we presented before, a couple of common questions we have heard are what is the best course of action to take now and going forward? Also, knowing that we are in a downturn, and it may last a while, shouldn't people perhaps "cash out" of investments, and wait for the signs of a rebound?

The answer still remains the same as before too. The challenge is that by the time that signs of a rebound have happened, that is usually after the market starts going up, and then you miss that upside because you are sitting out of the market. Plus, it is not necessarily clear if the market rising is just a temporary upswing, or something sustainable, and by the time the signals show it is sustainable, then you missed that prolonged upswing.

In essence, the above is market timing, and study after study shows market timing is almost always the wrong way to go when it comes to investing, and instead it is time in the market that makes the difference. While it may feel like it will not get better and continue to go lower and or stay low, it will get better. This has happened each and every time, and the markets not only recover, but surpasses where it had been prior.

It is for that reason that we, and most every reputable financial professional, will generally recommend that investments should have a long term outlook (5 years or more), which also includes for the planning of taking a stream of income when needed for retirement.

This is in conjunction for all of our clients to have a full year's worth of expenses in emergency funds in their bank, to help weather storms such as this. For those that are retired and have sufficient lifetime guaranteed sources of income in excess of their expenses, 6 months of expenses will do. That stated, if having a little more of emergency funds helps people sleep better, that's fine as well.

We give you a deeper insight into our thoughts on the past quarter and outlook further below. If you would like, we also have a link to the Q4 2022 Global Market Outlook by Russell Investments. Click here to access the commentary. .

In this issue of our Investment Newsletter:

- Our current investment topic is: What Does a Recession Mean for Investors?

- Recent articles where Landmark Wealth Management was quoted in the press.

- An overview of recent market activity, along with Our Perspective...

- A recap of the performance of major market indices from the past quarter

- Upcoming Economic Calendar

You will find past investment articles, by clicking the Articles tab above, or directly on our website, found under Periodicals.

If there is a topic of interest you would like to see covered in the future, please reply back to this email to let us know, or click here. Likewise, if you have any questions on this or anything else, feel free to reply back.

|

|

Investment Topic

What Does a Recession Mean for Investors?

For our investment topic, "What Does a Recession Mean for Investors?", we give a high-level overview of the topic. To learn more, please click here.

|

|

Recent articles where Landmark Wealth Management was quoted in the press

The past few years, Landmark Wealth Management has been quoted in the press for various articles. We have decided to start sharing these when they happen. If curious about past times we were mentioned, you can see it on our website under Articles > In The Press, or simply click here.

"Is It Possible To Run Out Of Money In Retirement?"

From an article that was in the US News & World Report in August: "Five Ways Muni Investors Can Navigate a Rising-Rate Environment". To access this article, please click here.

|

|

Our Perspective on Recent Market News and Activity |

|

Our synopsis of the past quarter, a look ahead, and putting it all in perspective: |

|

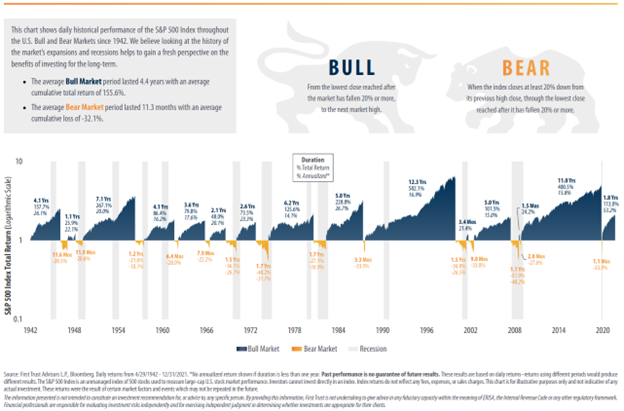

As we exit from Q3, one thing that is abundantly clear is that this Bear Market has some teeth. If watching bonds have their worst year in in a century wasn’t difficult enough, stocks showed that they can still be the leaders in volatility and sold off after a relatively strong but short-lived July rally. As we said in our last newsletter, this is exactly how Bear Markets are supposed feel and this has been no exception. As we and many other financial professionals will tell you, this too shall pass. However, until it does pass, we certainly know and understand that watching asset values fall is not fun and can be a bit frightening. That is why during these periods of time, we seek to remind our clients to let history be their guide.

So, what does history tell us about Bear Markets and recessions? Well, if you look at the chart below you will see that if we look at the historical performance of the S&P 500 since 1942, the average Bull Market has lasted an average of 4.4 years with an average cumulative return of +155.6%. Those are pretty powerful numbers. The average Bear Market has lasted 11.3 months with an average cumulative return of -32.1%. Where are we today as we enter Q4? Well, we are going into the 10th month of this Bear Market and the S&P 500 is off 25%, the Dow Jones Industrial Average is down -21% and the NASDAQ is down -32%. While we are in Bear Market territory, we are still below the historical average for a Bear Market, so be prepared there could still be some more downside to go before a recovery begins. However, a good amount of downside has been realized, so take a good deep breath, and give yourself a pat on the back for managing to hang in there and stick to the long-term plan. We know it is not easy and requires a certain degree of faith.

What the chart below you shows is that all of the past Bear Markets do eventually end, and it is usually measured in months and not in years. It is also followed by a nice rebound that eventually brings the market to new highs. You should also note in the chart below, that the Bear Market usually precedes a recession (the vertical gray line in the chart), which tells us that the market is a leading indicator and normally starts to rally before the recession ends and the market news starts to get better. One only has to go back two years ago to the Covid induced market sell-off as a reminder. That market decline which came on in record time saw the S&P 500 fall -34% in just a few weeks. That bottom turned out to be March 23rd, 2020, and at that time there was nothing good going on in the news. We were still a month away from possibly peaking with Covid deaths, a vaccine was still a long way off, and we were facing a complete shutdown of the global economy. Would anybody on March 23rd, 2020, thought that the market would go on to rally about 20% in the next 3 trading days, and not only recoup the -34% decline but to go on and finish up +18% for the full year 2020? Highly unlikely and those that got derailed from the long-term plan took on a huge loss for that year. We saw the same thing happen over a longer period of time during the Financial Crisis/Great Recession of 2007-2009. Staying the course turned out to be the best course of action and the market rewarded those who stuck around. Our point is again to let the market work through this difficult period so that it can eventually start moving back up again over time.

|

The chart above may be difficult to read in this format. If so, please click here, which will bring you to our related article in this newsletter, and a full page picture of the above chart.

|

Many investors unfortunately suffer from “myopic loss aversion”, which is a fancy way of saying one is taking a short-term focus on what should be a long-term goal. Investing is not easy, and it comes with these periods of extreme volatility. We encourage our clients to remind themselves that they are not the only ones who have seen their portfolio go down in value. It affects investors worldwide and is a global phenomenon. We also ask our clients to remind themselves that they have extremely diversified portfolios. Some may ask, “what is the value of a diversified portfolio if all the asset classes have gone down”? Well, the answer is that not all asset classes go down at all times, or at least to the same degree.

Normally bonds will serve a better buffer during periods of volatility, and while technically bonds are down less than stocks this year, they are not holding up their end of the bargain in a way that they normally do. That is a rare thing for bonds, and the bond market has seemingly priced in a good amount of rate hikes that have not yet been realized by the Fed yet to date. The good news is that bonds are now paying interest at higher levels than we have seen in quite a long time, and should the Fed ever get to the point where they need to cut rates, that will drive up the prices of existing bonds. A diversified portfolio also helps ensure that you will not have the misfortune of picking the wrong individual stocks or bonds. We have seen many prospects coming in to see us this year who have seen market declines in their portfolio of -40%, -50%, -60% or more because they got caught up in the excitement of some of the recent high-flying companies that you have seen in the news that were the darlings of Wall Street. In a diversified portfolio, you should never have that big a percentage in any one individual company, which reduces downside risk.

We are entering what is normally a seasonally strong period of the year, combined with a mid-term election year which has normally produced some fairly good returns. However, there has not been a lot of 2022 that has been “normal” so one must stay grounded should this just turn out to be another bad quarter and ultimately a bad year for the markets. The monthly CPI and jobs reports are key data points for the Fed as they look for signs that inflation is starting to come down in a meaningful and lasting way. The Fed would like to see a cooling off in the real estate and jobs market, so the monthly economic reports take on an important role to help give a better sense as to when the Fed will be able to signal an end to the rate hiking cycle. It may sound counterintuitive, but sometimes good news can be bad news as taming inflation is no easy task, especially after the very large increase in M2 money supply that we saw over the previous few years.

As we always say, if you find yourself overly concerned or anxious about your accounts, the markets, how this all affects you on personal level, we strongly encourage you to let us know and we will spend as much time as you would like to go over your own personal situation. We know that it takes courage to get through these markets, and there should be no shame, worry or hesitancy to let us know so that we can help you get through this difficult market period.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

|

|

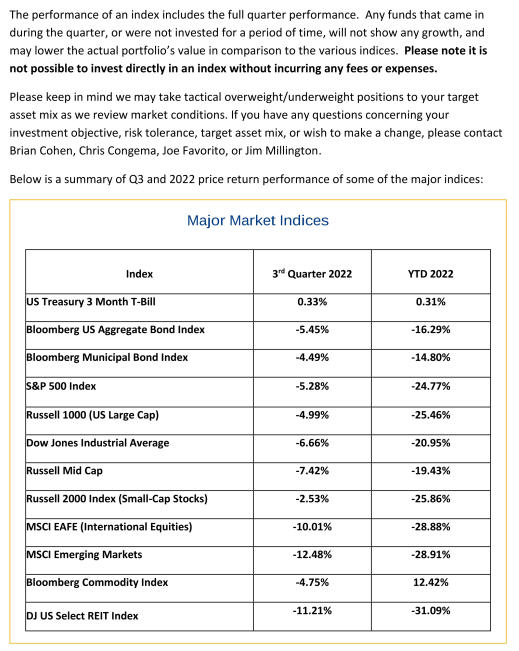

Below is the Q3 '22 price return performance of some of the major indices: |

|

On the Investment Horizon |

|

Upcoming Key Dates on the Economic Calendar

- First Friday of each month: Unemployment report for the prior month, released at 8:30AM.

- Monday, October 10 - Columbus Day: US Bond Markets closed.

- Thursday, October 22 at 8:30AM - GDP, 3rd quarter (first estimate).

- Tuesday, November 1 - Wednesday, November 2: The Federal Open Market Committee (FOMC) meets, and releases their announcement on Wednesday at 2PM.

- Friday, November 11 - Veterans Day: US Bond Markets closed.

- Thursday, November 24 - Thanksgiving Day: US Markets closed.

- Wednesday, November 30 at 8:30AM - GDP, 3rd quarter (second estimate).

- Tuesday, December 13 - Wednesday, December 14: The Federal Open Market Committee (FOMC) meets, and releases their announcement on Wednesday at 2PM.

- Thursday, December 22 at 8:30AM - GDP, 3rd quarter (third estimate).

- Monday, December 26 - Christmas Day (observed): US Markets closed.

- Monday, January 2 - New Year's Day (observed): US Markets closed.

|

|

For our clients - You should have received your statement directly from your account custodian (TD Ameritrade and/or Charles Schwab). If you have not, please let us know so that we may investigate the matter. Please review your statement carefully and let us know if you have any questions or comments.

Also, as a reminder, we have moved to a new office, with a nice sized conference room to use for our meetings and updates. If you do not feel comfortable coming into our office, we recommend that we possibly set up a Zoom or teleconference call to update your planning numbers, especially if it has been more than a year since we have last done so. Please feel free to reach out.

For everyone - If you desire an appointment, have any questions on any of this material, or any other financial subjects may relate to your own financial circumstance, please reach out to us at the contact information below:

Sincerely,

Direct phone: 631-923-2485

This communication is from Landmark Wealth Management, LLC, a Securities and Exchange Commission Registered Investment Advisory firm. The information in this email is not intended as tax or legal advice, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek tax, legal, or investment advice from an independent professional / financial advisor. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Information and use of materials contained in this email, including text and attachments, is confidential and is for the use of the intended recipient(s) only. If received in error, you are hereby notified that any dissemination, distribution, or copying of this communication, or any of its contents, is strictly prohibited. If you have received this communication in error, please reply to the sender and delete the original message and any copy of it from your systems. Be also advised that email communications are not secure. All e-mail sent to or from this address will be recorded by the Landmark Wealth Management, LLC email system and is subject to archival, monitoring, and inspection pursuant to securities regulations. Please direct any matters regarding this policy to [email protected].

|

|

|

|

Landmark Wealth Management, LLC

95 Broadhollow Road, Suite 102

Melville, NY 11747

(631) 923-2485

|

|

|

|

|

|

|