If you wish to suscribe to this newsletter click here

|

|

- Editorial Commentary: Mergers and Acquisitions Performance in Mexico During 2023 and Outlook for 2024

- Largest Transactions in the Last Five Years

- Amount and Number of Transactions: Comparative of the Last Five Years

- Number of Transactions, Exchange Rate (USD/MXN)

- Number of Transactions by Range of Disclosed Amount: Comparative 2019 - 2023

- Number of Transactions by Sector

- Cumulative Number of Mergers and Acquisitions by Industry

- Mergers and Acquisitions Transactions by Origin of Seller and Buyer

- Alternative Asset Activity: FIBRAs, Private Equity (PE) and Venture Capital (VC)

- VC Transactions

- Number of Transactions Worldwide with Transaction Value Exceeding USD $50 Billion

- Median EV/EBITDA Multiple of all Transactions Worldwide

- Multiple by Region Over the Last 10 Years

|

|

Dear reader,

As we do every year, we have prepared a summary and analysis of the mergers & acquisitions (M&A) activity during 2023 in Mexico. We hope you find it useful and interesting for your decision making.

Considering the dynamism that the Venture Capital market has gained over the last 3 years, as of 2022 we decided to separate the analysis of the M&A market from the VC market, so the graphs below only include M&A transactions, and not capital raises in startups. The analysis of VC activity is presented in a separate section.

|

|

1.-Editorial Commentary: Mergers and Acquisitions Perfomance in Mexico During 2023 and Outlook for 2024

|

|

Globally, the year 2023 continued to be marked by a high level of uncertainty, mainly due to continued high inflationary levels, high interest rates (which have an impact on discount rates in valuations and therefore on company values), as well as on costs and leverage levels in transactions with a debt component, and in the costs and leverage levels in transactions with a debt component) and multiple geopolitical tensions (the persistence of war in Ukraine, the increase of tensions in the Middle East with the war between Israel and Hamas, tensions between Taiwan and China, the coup attempt in Peru, the surprise elections in Argentina, to mention a few). In the face of these scenarios, Mexico presented itself to the world as a relatively stable investment destination by reducing inflation throughout the year, maintaining fiscal discipline and relative social and political stability. Investor confidence in the country was reflected in the exchange rate, where the Mexican peso appreciated 11.7% throughout the year; the price and quotes index of the Mexican Stock Exchange, increased 17.1%; and the M&A market activity, remained at practically the same levels observed in 2022 (1.2% increase in the number of transactions), when in most of the geographies of the rest of the world it showed a contraction. According to Pitch Book data, globally, the number of M&A transactions fell by 13.2%, from 45,777 to 39,733.

The year 2024 will most likely be an uncertain year for M&A activity in Mexico, mainly due to the presidential elections in the United States, because if the winner is Donald Trump, there will surely be fears regarding the measures he could take in relation to the increase of tariffs on imports, pressures for U.S. companies to invest in that country instead of in other geographies, and even, in an extreme case, decisions that could affect the free trade agreement between Mexico, the United States and Canada.

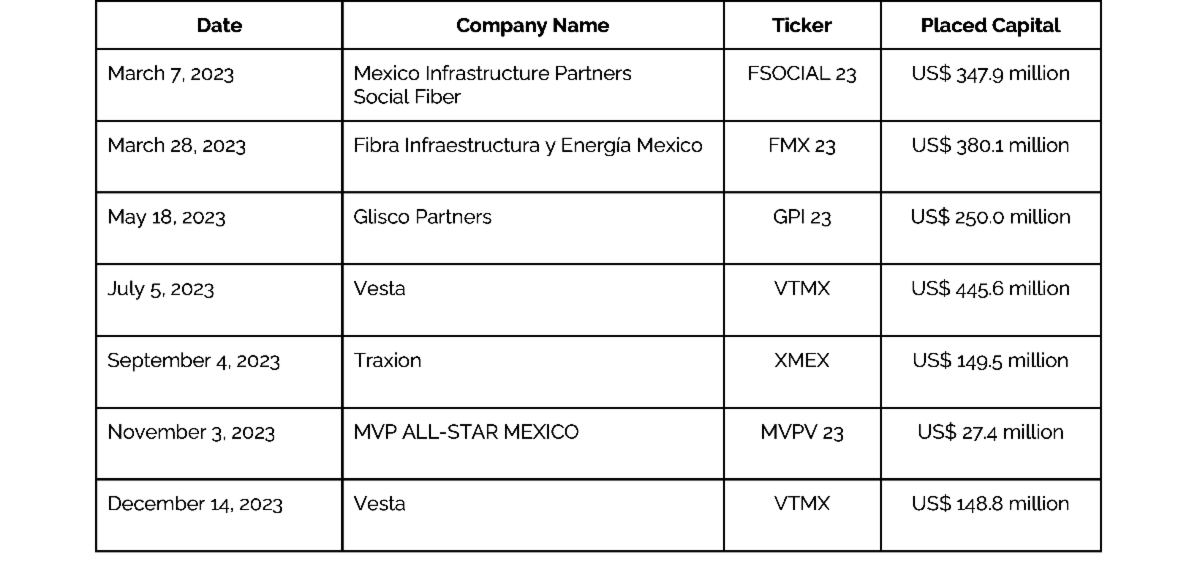

By 2024 we would expect to see activity in the real estate and logistics sectors, as the vehicles that have come out to raise capital in the markets over the last few months begin to use it. Here is a summary of the main placements through 2023 (USD $1,749 million):

|

|

2.- Largest Transactions in the Last Five Years |

|

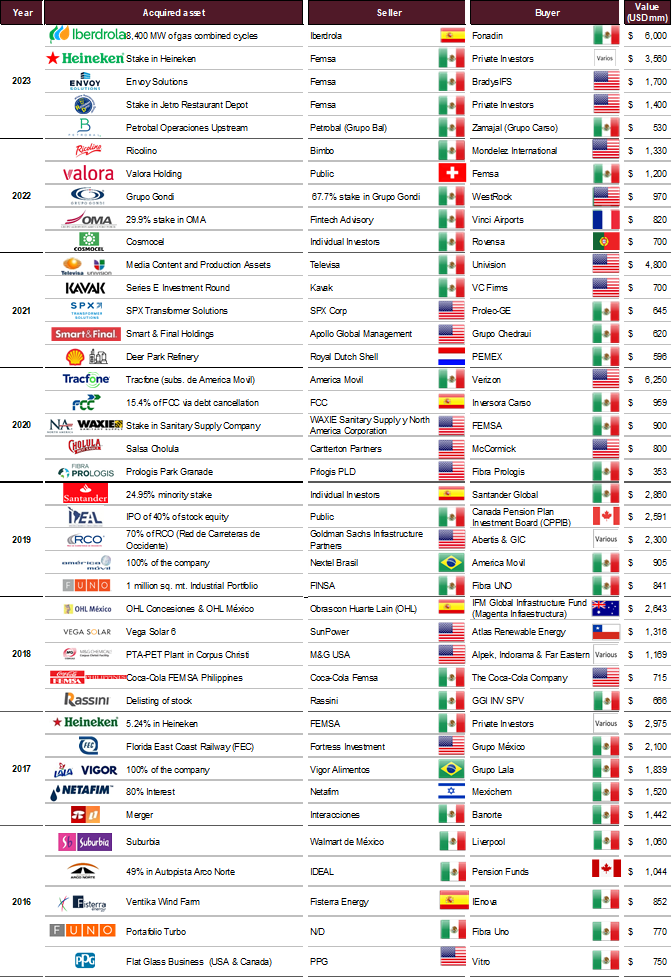

During 2023 they recorded 4 transactions with a value above USD $1 billion, which marked a recovery compared to the previous year, when only 2 transactions were recorded. Of the 5 largest transactions of the year, 4 were between Mexican and foreign counterparties, and only one of them was between Mexican counterparties.

The largest transaction announced in Mexico in 2023 was led by Spain's Iberdrola and the Fondo Nacional de Infraestructura (FONADIN), in which Iberdrola sold 13 power plants generating 8,400 MW for USD $6 billion. The second largest transaction was the divestment by Fomento Economico Mexicano (FEMSA) of its stake in the Dutch company Heineken for USD $3.5 billion.

Similarly, FEMSA made two more divestments for USD $1.7 billion and USD $1.4 billion. The first, Envoy Solutions, was sold to BradysIFS, a U.S.-based platform specializing in the distribution of foodservice, cleaning, and sanitary supplies. In the second case, the company sold its minority stake in the wholesale self-service chain specializing in restaurants, Jetro Restaurant Depot.

Finally, Grupo Bal sold its oil subsidiary Petrobal Operaciones Upstream for USD $530 million to Grupo Carso's Zamajal.

The following table presents the 5 most relevant transactions in Mexico, in terms of amount, for each year during the period 2019-2023. It is worth noting that, of the 25 transactions in the list, on 12 occasions (48%), the buyer was Mexican. On the selling side, in 13 cases (52%) the seller was Mexican.

|

|

Source: Prepared by RIóN M&A with public information |

|

3.- Amount and Number of Transactions: Comparative of the last Five Years

|

|

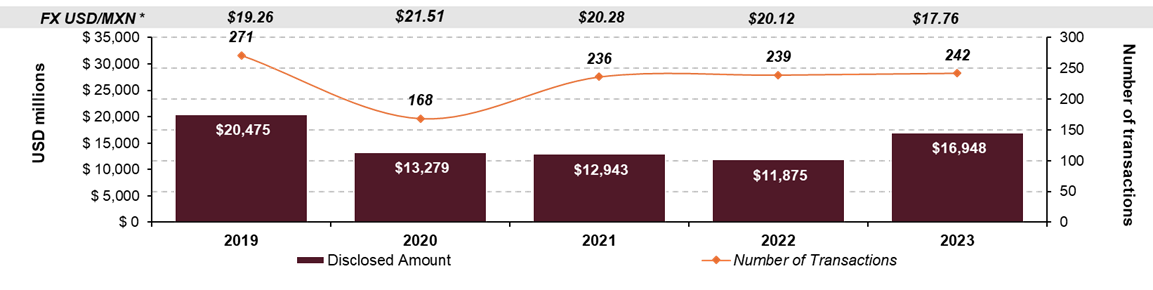

Amount disclosed in millions of USD, number of transactions per year |

|

* Average exchange rate for each year.

Source: Prepared by RIóN M&A with public information

|

|

During 2023, 242 M&A transactions were published in Mexico, 3 more than in 2022, representing a slight increase of 1.2%. It is noteworthy that despite the economic conditions observed both in Mexico and globally, there has been an increase in the number of transactions, as investors often stop their investment pace due to the uncertainty generated by geopolitical tensions or an upward cycle of interest rates. However, we still fall short of the levels of transactions recorded during 2019, when 271 were reported.

On the other hand, the cumulative amount disclosed was USD $16.9 billion, 42.7% higher than the amount reported the previous year (USD $11.8 billion), and 15.7% higher than the average of the last 4 years (USD $14.6 billion).

|

|

4.- Number of Transactions, Exchange Rate (USD/MXN)

|

|

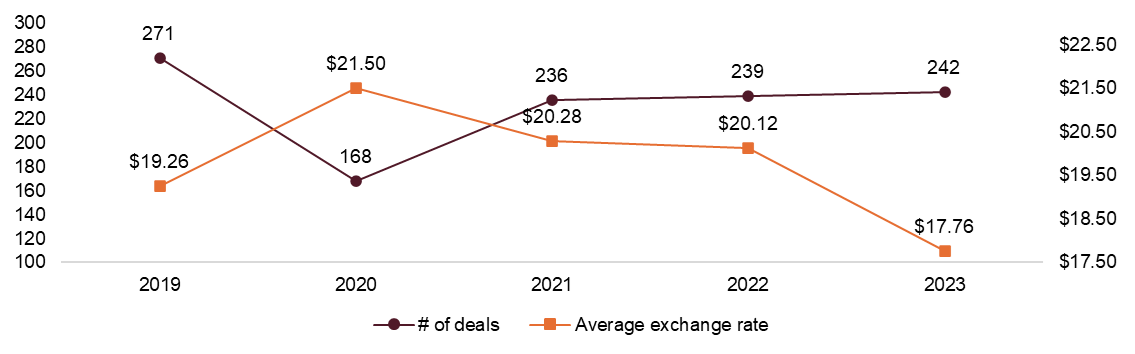

Number of transactions, average exchange rate during the period

|

|

* Average exchange rate for each year.

Source: Prepared by RIóN M&A with public information

|

|

Over the years we have observed that there is a certain degree of negative correlation between exchange rate levels (USD/MXN) and the number of transactions carried out during the year, which was not the case in 2023.

During 2020, the exchange rate increased by 11.7% and the number of transactions made in the year experienced a drop of -38%. In contrast, for 2021 the exchange rate fell -5.6% and the number of transactions increased by 40.5%. In 2022 both the exchange rate and the number of transactions remained stable.

However, by 2023 the exchange rate decreased -11.7%, from $20.12 to $17.76, and the number of transactions experienced a slight increase of 1.3%. We might have expected the increase in the number of transactions to be greater, however, a curious phenomenon was observed this year: in the case of both Mexican companies that export abroad and those that sell dollarized products in Mexico, their revenues and margins were negatively affected by the strength of the peso; on the other hand, companies with dollarized costs and peso-denominated sales benefited greatly from the behavior of the exchange rate, increasing their margins significantly. This phenomenon, together with the increase in interest rates and consequently in discount rates, affected the valuations of many companies, which in turn led to difficulties in price negotiations between buyers and sellers.

|

|

5.- Number of Transactions by Range of Disclosed Amount: Comparative 2019 - 2023

|

|

Number of transactions (with disclosed amount in USD) |

|

1) Number of transactions whose amount was disclosed / Total number of transactions reported in the year. Historically, more than half of the transactions occurring in the country do not report amounts (69% in 2021, 76% in 2022 and 78% in 2023, so they are not included in this chart).

Source: Prepared by RIoN M&A with public information.

|

|

Most transactions in Mexico are for less than USD $100 million. During 2023 of the 54 transactions reported, 67% had a value below that amount. In the last 5 years, on average, 65% of the transactions were less than that amount. It is important to consider that there are many private transactions, typically of smaller sizes, that are not made public, so the actual number of transactions under USD $50 million could be substantially higher than those published in our monthly bulletins.

During 2023, 5 transactions with a value above USD $500 million were recorded, 3 less than those observed in the previous year. Of these five, 4 of them were for a value greater than USD $1 billion.

|

|

6.- Number of Transactions by Sector |

|

Source: Prepared by RióN M&A with public information |

|

Historically, Mexico has been characterized as a manufacturing country, mainly for having a competitive labor force in terms of cost and quality, for its geographic proximity to the United States, and for the commercial strength it has with other countries (Mexico is one of the countries with the highest number of free trade agreements in the world). This is why, when reviewing the number of mergers and acquisitions by sector, the Industrials, Manufacturing and Engineering sector is the most active sector during each of the years analyzed. It is worth noting that this sector includes a wide variety of activities, ranging from companies in sectors such as light manufacturing, chemicals, metallurgy, to oil and renewable energies. During 2023, this sector accounted for 24% of total reported transactions.

After the industrial sector, the Consumer Products and Real Estate and Construction sectors were the most active in 2023, accounting for 16% and 14%, respectively, of total reported transactions.

|

|

7.- Cumulative Amount of Mergers and Acquisitions by Industry

|

|

Amount disclosed in millions of USD by sector |

|

Source: Prepared by RIóN M&A with public information |

|

As was observed in the number of transactions, in terms of amount disclosed, the Industrials, Manufacturing and Engineering sector dominated, with a 42% share of the total amount disclosed during the year. In second place is Consumer Products, which represented 40% of the accumulated amount. It is worth noting that FEMSA's transactions analyzed above represent 99% of the total amount disclosed during the year within this last sector.

The only other sector that accumulated an amount above USD $1 billion was Real Estate and Construction (12% of the total).

|

|

8.- Mergers and Acquisitions Transactions by Origin of Seller and Buyer |

|

Origin of the seller – origin of the buyer |

|

Transactions in which both the seller and the buyer are foreigners involve an asset that is in Mexico.

Source: Prepared by RioN M&A with public information.

|

|

In terms of the origin of the seller and buyer in mergers and acquisitions in Mexico, most years are dominated by transactions involving foreigners acquiring Mexican counterparties; however, during 2023, as was the case during 2020, there was greater activity of Mexican companies investing locally, which increased from 70 transactions to 81. On the other hand, the number of transactions of foreign companies acquiring in Mexico decreased and those of Mexican companies acquiring outside the country increased. One possible explanation for this behavior is the appreciation of the peso, since, in dollar terms, for foreign companies, transactions acquiring in Mexico were more expensive, while for Mexican companies acquiring abroad, were cheaper.

On the other hand, transactions of foreign companies with Mexican counterparties fell from 85 to 72.

The number of Mexican companies investing abroad increased from 50 to 60 transactions. The activity of large companies CEMEX, FEMSA and Grupo Bimbo, which together accumulated 15 transactions, stands out.

The decrease in the number of transactions of foreign companies acquiring in Mexico and the increase in the number of transactions of Mexican companies acquiring outside the country may have been due to the appreciation of the peso against the dollar, since for foreign companies, transactions acquiring in Mexico were more expensive (they needed more dollars to buy companies valued in pesos), while for Mexican companies buying abroad they were cheaper (they needed fewer pesos to buy companies valued in dollars).

As for the activity of foreign companies with foreign counterparties, as has been observed historically, these were the least active.

|

|

9.- Alternative Asset Activity: FIBRAs, Private Equity (PE) and Venture Capital Funds (VC)

|

|

Number of transactions and amount disclosed in millions USD

|

|

Source: Prepared by RióN M&A with public information |

|

The activity of private equity funds, such as FIBRAs in the country, has presented a downward trend, going from 28 and 17 transactions in 2019 to 19 and 15 in 2023 (a 9.2% and 3.1% compound annual drop, respectively). Analyzing the cumulative amounts disclosed there would appear to be a recovery in the PE sector, which although far from the USD $1.7 billion observed in 2019, in 2023 accumulated USD $545 million, a growth of 59.1% versus the previous year. On the FIBRAS side these accumulated USD $658 million (a drop of 46% against what was disclosed in 2022). During 2022, FIBRA MTY announced the acquisition of a portfolio valued at USD $662 million, which increased the comparison base extraordinarily.

After its lowest level in 2020 with 8 transactions, private equity fund activity has been slowly recovering to 19 deals in 2023, still far from the 28 investments reported in 2019. When analyzing the cumulative amounts disclosed there would appear to be a recovery in the sector, as in 2023 it accumulated USD $545 million, a growth of 59.1% against the previous year.

The number of real estate trust transactions (FIBRAs) has remained practically stable between 2020 and 2023.

Regarding transactions of Mexican startups receiving investments from venture capital funds or VCs, in 2021 there was a boom, both in number of transactions and amount. In 2022 there was also a 10.8% growth in the number of transactions (although the total amount of investment was lower), however, in 2023 there was a 26.4% decrease in the number of transactions, going from 163 to 120 with a cumulative amount 52.1% lower. The drop in the number of transactions and amount invested in VC operations in Mexico in 2023 was largely due to the fact that funds are now giving importance to the timeframe in which companies can reach their break-even point instead of only considering the revenue growth rate, and, likewise, have been more cautious in valuations, resulting in entrepreneurs and their investors in the first rounds finding it difficult to accept a lower valuation than in the last equity investment.

|

|

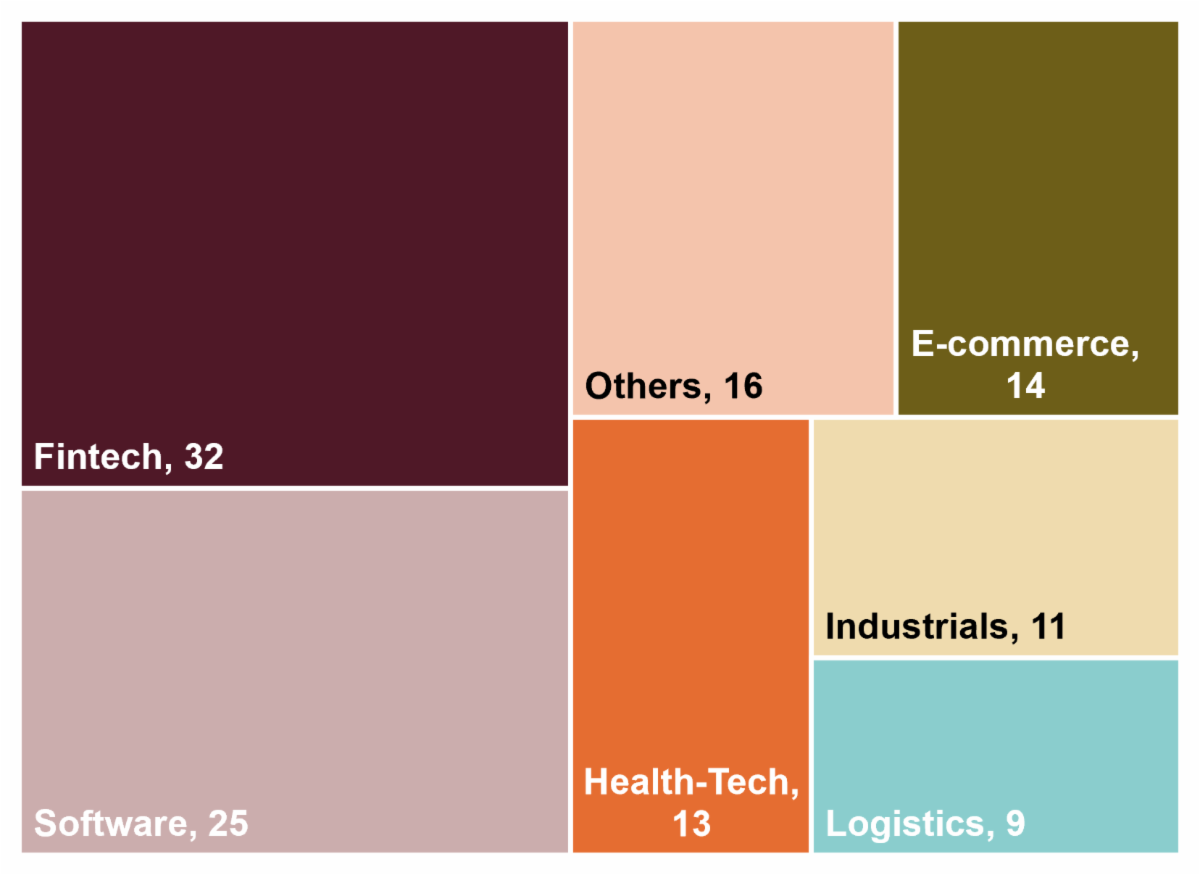

Number of transactions by sector |

|

Industry-Manufacturing-Engineering includes companies specializing in energy, technology infrastructure and food products.

Source: Prepared by RioN M&A with public information.

|

|

Considering the size of the VC market in our country, it is interesting to analyze which were the most attractive sectors. As observed last year, the sector with the highest number of transactions was fintech with 32, equivalent to 27% of the total 120 transactions published. The software and e-commerce sectors also stood out, with 25 and 14 transactions respectively, representing 21% and 12% of the total.

|

|

Amount disclosed in millions of USD by sector |

|

Industry-Manufacturing-Engineering includes companies specializing in energy, infrastructure technology, food products

Source: Prepared by RIoN M&A with public information.

|

|

In terms of the amount of investment disclosed in 2023, which totaled USD $627 million, the sector with the largest investment was fintech with USD $328 million (52% of the total). Within this sector, there was only one investment round with a value of more than USD $50 million, corresponding to the USD $60 million investment received by Clara. The next largest sector was software, with USD $128 million (20% of the total), including investment rounds received by the human resources administrator Osmos for USD $48 million, and the AI platform that generates conversations with clients, Yalo, for USD $20 million.

|

|

11.- Number of Transactions Worldwide with Transaction Value Exceeding USD $50 Billion

|

|

Source: S&P Capital IQ and Pitchbook |

|

During 2023, there were 2 transactions with a value of more than USD $50 billion. These were Chevron's acquisition of Hess for USD $60 billion, and ExxonMobil's acquisition of Pioneer Natural Resources, a transaction valued at USD $64.5 billion.

|

|

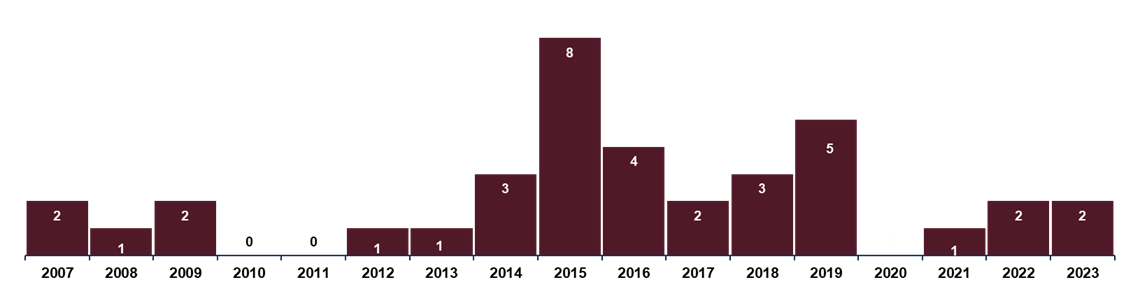

12.- Median EV / EBITDA Multiple* of All Transactions Worldwide

|

|

2007 – 2023, in times and thousands of operations |

|

* This multiple is the most used in merger and acquisition transactions as a reference for the valuation of acquired companies. It is obtained by dividing the company's enterprise value ("EV") by its operating income plus depreciation and amortization ("EBITDA"). Enterprise value (EV) refers to the value of stockholders' equity plus debt with cost.

Source: S&P Capital IQ and Pitchbook

|

|

During 2023, the total number of transactions fell 13.2% from 45,777 to 39,733, probably due to the geopolitical uncertainty observed and the continuation of the upward interest rate cycle. However, the EV/EBITDA valuation multiple recovered from 9.4x during 2022 to 10.2x during 2023. The increase in the multiple times EBITDA in 2023 could have been because buyers are more confident that the acquired companies can show better growth and profitability performance in the short and medium term. |

|

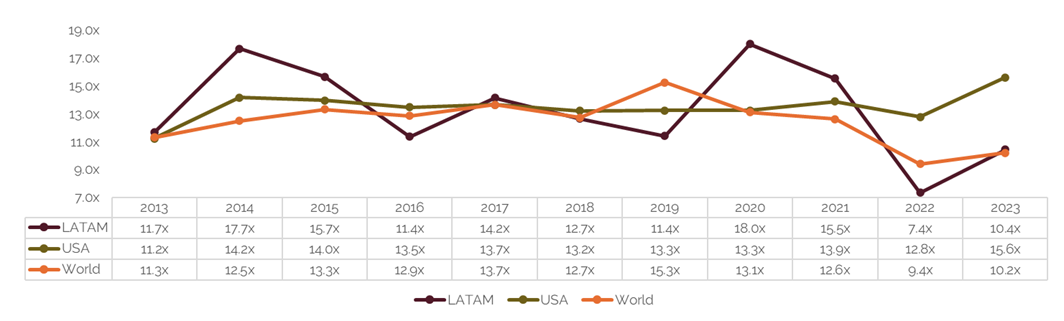

13.- Multiple by Region Over the Last 10 Years |

|

Average EV / EBITDA multiple |

|

In the graph above we analyze the behavior of the EV/EBITDA multiple over the last 10 years in three geographies: Latin America, the United States, and the rest of the world.

We note how the multiple is highly volatile in the Latin American case, peaking at 18x (in 2020) and 7.4x (in 2022). The United States and the rest of the world show a high correlation between them (mainly because the United States sets the global market pace).

During 2023, we see that the multiples have risen with respect to 2022 to 10.4x for Latin America, 15.6x for the United States and 10.2x for the rest of the world.

|

|

This is a free electronic newsletter courtesy of RIóN, sent with the purpose of providing you with useful information. Please feel free to share or forward this newsletter to you colleagues, friends and/or associates.

The editor is not responsible for the damages caused by the use of the information included. The information included in this newsletter was gathered from public sources (América Economía, Bloomberg, El Economista, El Financiero, El Excelsior, El Universal, Sentido Común, Reforma, El Norte, The Wall Street Journal, Mergermarket, Business Week, New York Times, Expansión y CNN / Expansión, DealWatch, LatinLawyer, El Mural, among others) and direct sources of Pablo Rion y Asociados and it is subject to the accuracy and truthfulness of them.

|

|

© 2004–2023 by RION M&A S.C. All rights reserved.

Reproduction is forbidden unless authorized by RIóN®.

|

|

|

|

|

|

|