Hello All-

Happy Friday. And May. For those of you in warmer climates, I hope you’re enjoying your ‘prime’ spring weather. For the rest of us, well, it’s been nice to get a few glimpses of the proverbial light at the end of the tunnel!

I’m pushing this out a bit earlier than planned (otherwise next week) given the particularly steep gyrations we have seen in the market this week. As I mentioned a few weeks ago, we intend to get your personalized 2022-2023 financial planning checklists out, along with an outline of recent trades made in your account and corresponding rationale. With the more significant volatility lately, I’m actually going to reverse the order of distribution---we’ll get the trade rationales out next week, and the financial planning checklists out by the end of the week of May 20th.

So, despite the April jobs report which reported that the U.S. economy beat expectations (428,000 v. 400,000), stocks continued to slide this morning. The unemployment rate remains at a historically low 3.6% and wages grew 5.5% year over year. On Wednesday, the Fed said it is not currently considering hiking the benchmark lending rate by three quarters of a percentage point, so markets are forecasting half-point or quarter-point hikes from here. This was initially cheered by investors and the market surged on Wednesday…only to give it all back and then some yesterday. So, to put it simply, despite some very positive news, Wall Street is on edge.

Since there can only ever be one headline issue in financial journalism—and since that issue must always be presented as a looming catastrophe—we are currently being told that the only economic issue in the world today is a recession. This replaced stagflation, Russia/Ukraine, soaring oil prices and rising interest rates, all of which were at various times in the last few months the only issue.

Nevermind when the recession is going to happen, how deep and/or long-lasting it’s likely to be, or what effect (if any) it will have on the equity market. For that matter, never mind that many of the sharpest economic minds continue to regard recession as quite a bit less than probable. These questions are entirely too nuanced! In the journalism that hits most of us like a firehose these days, the question is purely binary: will there/won’t there be a recession? Always looking hungrily for the next ‘crisis’, journalism is all but assuring us that there will be.

But let’s look at some facts, compiled by Nick Murray, a 50-year veteran advisor with an incredible talent for putting things in perspective at moments like these:

- Just since 1980, there have been six recessions, an average of one every seven years

- The longest was that surrounding the Global Financial Crisis. It ran for a year and a half from Dec 2007 to Jun 2009; GDP declined 5.1% from peak to trough

- The shortest was the COVID-19 shock recession. It ran from February to April 2020, and took GDP down 19.2%

- The average duration of the six recession was 10 months, and the average GDP decline was about 5% (without COVID-19 crash, average GDP decline was just over 2%)

- The total number of months from January 1980 through April 2022 was 508. The total number of months of decline in the six recessions was 58. That is to say that during this period the US economy was expanding 88% of the time.

- According to the Federal Reserve, real (inflation adjusted) GDP per capita in the first quarter of 1980 was $30,174. For the fourth quarter of 2021, it was $59,553. During these four decades when the American economy was experiencing six recessions—every one of which was reported in the media to be the End of Economic Life As We Have Known It—U.S. real GDP per capita doubled.

- Over the same period mentioned above (Jan 1980-Apr 2022), the average annual compound rate of total return of the S&P 500 was 11.8%- quite a bit higher than the long-term average of 10.5%

But these are just facts that I understand are not always helpful in these moments. So, what exactly is a recession, and how much should we be worried about it here in the short term?

What is a recession?

First, textbook: A recession is a prolonged period of economic decline, beginning when the economy peaks and ending when it bottoms out. Recessions are typically marked by an economy shrinking in back-to-back quarters, typically measured by GDP (gross domestic product- how much are we collectively buying and producing as a society). But there are exceptions to this rule, including the brief and exceedingly steep recession the US entered during the early months of the pandemic. And that technical designation doesn’t mean much to anyone who’s not an economist.

The reality of how a recession feels is broadly economically gloomy—think rising unemployment, a stock market in decline, and stagnating or shrinking wages. People often rein in spending as gloom sets in, giving recessions a psychological component that can be hard to shake. For example: Technically, the Great Recession that began in 2007 lasted just 18 months, but the impact of the crisis weighed on consumers far longer.

Economists call this lingering effect, especially in the labor market, “hysteresis”. The 2020 recession itself was brief, but its mass layoffs and furloughs, along with a rapid shift to working from home, shattered previous assumptions about the value and meaning of work. Around the world, workers’ dissatisfaction with their employers has stirred a movement to seek something better, a phenomenon known as the ‘Great Recession’.

What causes a recession?

For now let’s just focus on the most pressing risk right now: The Fed’s fight against inflation. One of the quirks of our modern capitalist system is that when the economy is going strong, officials have to deliberately hurt it to keep it from going completely off the rails. That is what the Fed is trying to do right now.

On Wednesday, the Fed raised it’s key interest rate a half-percentage point, its most aggressive rate hike in 22 years. Interest rates are the Fed’s primary tool to control inflation. But predicting economic expansions and recessions is notoriously difficult, and the Fed has been historically bad at it. So the actions taken have to be extremely delicate. The bank has to raise interest rates just enough to take the heat off surging prices. Overdo it, and economic demand could crater, resulting in recession. Do too little, and prices may keep going up, which would also lead to recession.

The ideal outcome is known as a ‘soft landing’ in which consumer prices come down and economic growth carries on at a steady clip. Regardless, we want them to do this. If it takes a recession to break the back of this inflation—and if that recession causes the equity market to sell off further and longer than it already has—a sane long-term investor must not merely endure this but embrace it. This is exactly how Paul Volcker ultimately snuffed out the hyperinflation of 40 years ago. It wasn’t pretty- the fed funds rate shot up over 20%, unemployment soared to near 11%, and the S&P 500 went down 27%. But with inflation dead, the greatest bull market of all time—from August 1982 until March 2000---ensued.

Remember that we have had three years of 24% annual compounding to some extent because the Fed overstimulated. If there’s a price to be paid for that, let’s try to be stoic about paying it. The cure is not worse than the disease. One way or another, we need to stamp out inflation.

As financial planners and investment advisors, we have listened carefully to understand your financial goals and make sure you have adequate liquidity/stable assets to fund them, no matter what happens with the stock market in the relative short term (the primary goal is of course not being in a position to have to sell stocks when they’re down in order to come up with necessary liquidity to fund ‘life’). As hard as it can be as mere mortal human beings, we mustn’t let our emotions get the best of us. The best thing to do is stay disciplined and stick to our investment allocation, which was constructed around the notion that a recession could always be around the next corner. We are prepared. We have been all along. So all we’ve had to do lately is some small fine tuning in light of the unique set of risk factors at play given current events.

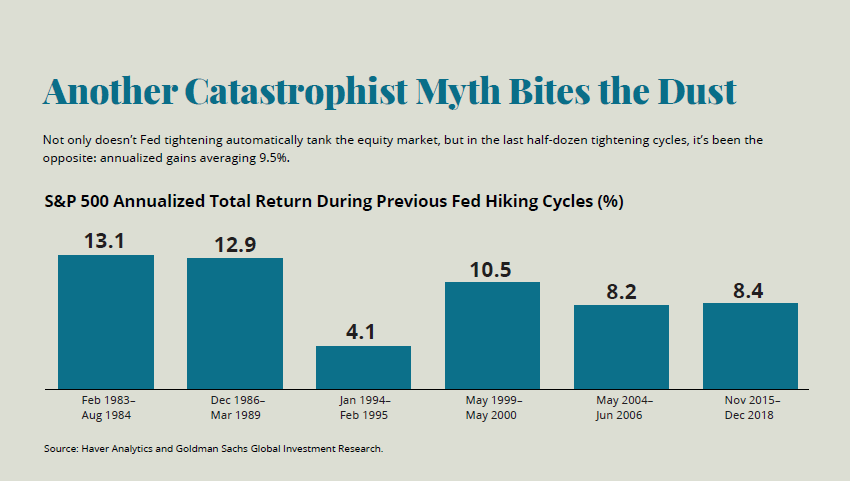

I have more content I’ve been curating for you over the last month, and will assemble that for an additional distribution in the coming weeks. But for now, I will conclude with a useful visual that shows that the past six times we’ve seen a rate hike, a year later, the market is higher. So for those who have been asking/wondering, YES, we feel very confident that now is still a great time to invest if you have some time to ride this out.

We’re grateful for your trust and confidence. As always, please don’t hesitate to call or email with questions.

Charlie