RETIREMENT SECURITY MATTERS

A forum for retirement innovation information sharing focused on

states, supporters, and service providers.

Vol 40 | October 21, 2021

|

|

Greetings! welcome! to Retirement Security Matters – where we talk about retirement readiness innovation by states, supporters, and service providers.

|

It has been Monday all week here at RSM; we hope your week feels more like Friday-Friday-Friday. If not, we got you. Grab a snack and exhale. In this edition:

-

Groom Law’s Michael Kreps on the good and the hidden in new retirement security legislation

-

Fresh metrics on the state Auto IRA programs

-

State updates – Virginia, Colorado, New Jersey – and more

-

Advertising on your mind? How to think about it if you’re a state – with Joel Metlen

-

Hot Sauce: Communication that moves the needle – are workers starting to delay taking Social Security? And NIRS takes a look at middle class financial assets

-

And finally, PIX of the Week! that will have you looking for a warm sweater, tickets to somewhere warm, or a Halloween costume 🎃.

|

|

Michael Kreps of Groom Law: Cool Things You Might Not Know

|

|

Michael P. Kreps, Principal

Groom Law Group

|

|

One thing we love about our friend Michael Kreps is that despite his impressive bio and accomplishments as a principal at Groom Law Group and as senior pensions and employment counsel to the Senate HELP Committee, he is more spark than reserve – and he knows more about the industry than we are likely to forget in our lifetime.

Today we talk about some hidden elements of proposed federal legislation that, if passed, could be industry-changing. And if you want to return more than $60 billion to retirement savers, what’s the one thing you could do? Read on to find out.

|

|

Michael, there's a boatload going on in Washington, DC and around the country. What are you seeing that's interesting in the retirement security space?

Legislation continues to percolate! Now, keep in mind that retirement legislation is not a huge priority for Congress. There are a couple of members that care about it, but it's generally not a top tier issue for most members of Congress.

It just so happens that the Chairman of the Ways and Means Committee Richie Neal is particularly interested in it. It's an issue that he's been passionate about for a long time. So, we see a bi-partisan legislative path on a bill that is a grab bag of fix-it and clean up items for the retirement system. And then we also see a larger scale set of reforms in the Build Back Better Act, which is the partisan process. The Build Back Better Act is where the people in Congress, at least on the democratic side who care about retirement, are focused. It’s a priority for them that we should have universal automatic enrollment.

Build Back Better creates a national requirement for employers to enroll their workforce in some form of automatic retirement savings; non-ERISA solutions could include an enhanced version of payroll deduction IRA. What do you see?

I would characterize the current version as the most industry friendly version of the legislation I’ve seen. It's basically just a requirement that employers offer a plan. There's no public option, like there have been in prior versions.

In addition to imposing a requirement of the universal automatic enrollment on most employers, excluding all but the newest and smallest employers, it also then tries to make it easier on employers by providing a couple of different types of new plans employers can adopt that are pretty low cost, or don't have much burden on the employer. One is a 401(k) that doesn't require any … (What is that? Bookmark HERE to get the rest.)

Michael – what a terrific conversation. Thank you for sharing your expertise with us! Want more? You can connect directly with Michael Kreps by email here. You can follow Michael’s work at Groom Law Group here. You can also connect with Michael on social here.

|

|

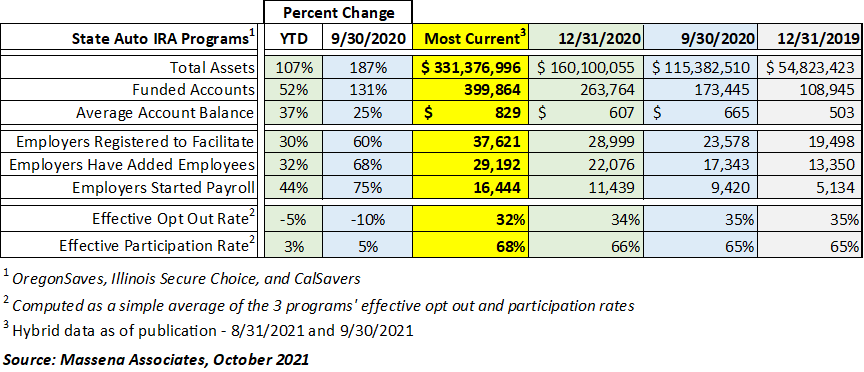

*Fresh!* State Auto IRA Program Metrics |

|

Chart-san, can you read this for us? Why yes! Check it out … funded accounts across the three programs are so close to crossing the 400,000 mark. When Oregon’s 9/30 numbers come in, we’ll be there. That’s more than 2x where we were a year ago. Combined assets are over $330 million.

Average account balances are now at $829. They dipped a little when California’s data came in because CA has so many new accounts. As reported recently, Oregon’s average account balance is higher ($1,175) because the program has been in place longer. Average 30-day saver contribution rates are $113, $138, and $143 (Illinois, Oregon, California). At these rates, balances will increase by $1,300 to $1,700 annually, not including investment impact. Employee opt out rates are steady, at about 30%.

Employer perspective: More than 16,000 employers are now facilitating state Auto IRAs. Another 29,000 have registered to facilitate and are in the process of providing employee roster information, which is the first step in the employee engagement process, or preparing to start payroll deductions for participating employees.

|

|

State Facilitated Retirement Programs - Fresh Highlights |

|

Virginia (workforce 4.3 million) – The Virgnia529 program has hired a Retirement Program Director for the new state-facilitated retirement savings program scheduled to launch in 2023. Mr. Peter Thompson joined the team of CEO Mary Morris this September and is hard at work already. If you’re reading this on Thursday the 21st, today is the first meeting of the Virginia529 Retirement Program Advisory Committee. The meeting is expected to provide an orientation to the program and its history as Virginia prepares to move into implementation mode.

|

|

Colorado (workforce 3.2 million) – The Colorado Secure Savings Program Board met October 18, 2021. At the top of the meeting, [Woohoo!] Colorado and New Mexico shared that they intend to partner together and that they are working on a Memorandum of Cooperation. The Board reviewed an amended proposed timeline for the program as well as program design elements such as automatic escalation, employer deadlines, Roth vs. Traditional IRAs and investment options.

An October 8, 2021 story in the Aspen Daily News notes that Colorado Treasurer spoke about the Colorado Secure Savings Program during a recent visit. “I think everybody understands they want to have retirement — how to actually make that happen is often not clear to people,” said Treasurer Young. “This is why we have so many people that aren’t saving.”

|

|

New Jersey (workforce 4.4 million) – An October 7 Insider NJ story reported that New Jersey’s gubernatorial candidates, Jack Ciattarelli (R) and Phil Murphy (D), both support the state’s Secure Choice program that would “create a voluntary and portable retirement savings option for around 1.7 million private-sector New Jerseyans who currently do not have a way to save for retirement at work.”

|

|

C O M I N G U P

-

New Mexico (workforce 1 million) – The next meeting of the New Mexico Work & $ave Board is scheduled for Nov. 4, 2021. For more information, please visit the Board’s website here.

-

Oregon (workforce 1.9 million) – The next meeting of the OregonSaves Board is scheduled for November 9, 2021.

-

California (workforce 17.9 million) –The next meeting of the CalSavers Board is scheduled for December 13, 2021.

|

|

Advertising: So Many Ways to Spend All Your Money! |

|

I once began a conversation with a marketing firm by asking, “Where should we advertise to get the best bang for our buck?” They answered the question with their own question, “How much money do you have?”

The response was annoying, but it made sense from their point of view. They knew there was a limit to what we could spend, and they saw their jobs as figuring out how to maximize the potential of each dollar available. They’d tailor their plan based on what we could afford, whether that was $5 or $5 million.

When starting a new program or service, like a state-sponsored retirement program, marketing is incredibly important for getting out the message to those impacted and eligible, so they know about it and have an opportunity to make an informed choice. It’s also a key factor in ensuring the program can achieve its goals to further people’s retirement security and ultimately pay for itself. This is true even if the program includes a mandate for employers to participate, and it’s even more critical if employer participation is voluntary, to help convince folks to join.

So where do you start?

Usually before I even begin talking to marketing firms, I like to …

|

|

The last thing to remember is that you can always shift tactics over time. My communications plans often only cover a short period, like six months or a year, and I like to revisit them often based on lessons learned. Often times, advertising for new programs is a learning experience and an opportunity to continuously improve messaging and tactics.

Stay tuned! / Joel

|

|

Columnist and Senior Associate Joel Metlen is based in Oregon. Joel is a pioneer of the state facilitated retirement savings space, woven into a career of public service and innovation. At OregonSaves, Joel’s responsibilities ranged from marketing and employer engagement to operations and data analysis. You’ll see his insights from that experience, and more, here.

|

|

We’re going to talk about this in more detail very soon, but NIRS’ Tyler Bond has a new infographic out on Middle Class Ownership of Financial Assets and we think you’re going to find the results a little disturbing.

Are people getting the message – and what are the implications? Our friends at Boston College find that more people – a few more people – are delaying taking Social Security in favor of a higher retirement benefit.

And, across the pond, NEST is finding that positive communication helps increase retirement savings account engagement and use. We like this! Three positive messages that had a dramatic impact:

- You're already on your way to having a retirement income: Boosting confidence by emphasizing what savers already have going for them

- Start from today and plan forward: Helping people work from what they know, to understand the gap they need to close

- There are steps you can take: Breaking it down into manageable and meaningful actions and showing the difference each step could make to a retirement income.

In the Presidential zone: This week we listened to this podcast on Presidential libraries by Delaney Hall for 99% Invisible but found it just a hair acerbic. What do you think? Maybe it’s because we hold a fondness for all things library, and we don’t mind the quirks. We’re thinking about adding presidential libraries, baseball parks and national parks to our to-do list.

|

|

… Coffee's getting cold, give us those PIX! |

|

Okay, okay! You know we love dogs around here, and it’s almost Halloween. Please give a friendly Hello to Pickles Kreps! Pickles, you are just styling, getting us ready for the season. We’ll take the money. You can keep the TNT ❤.

|

|

We don’t know how Michael Kreps has time for anything outside of work. But we know he loves to kayak (sometimes it’s cold out there), and sometimes his travels take him to even more distant shores. |

|

|

|

|

We hear the second pic is from a temple “very close” to North Korea.

Stay out of the DMZ, friend – we need you!

|

|

On other frontiers, this week we were introduced to the spot where Oregon’s first provisional government was formed, in 1843.

|

|

It’s situated on the south side of the Willamette River, well west of Portland in grape-and-hops country. And if you look closely, you can find a put-in for your kayak.

|

|

That’s it for this edition! ❤ Hug your people and change the world.

If you like this piece, please stick with us. We’ll be back in about two weeks. If you don’t like it, please unsubscribe below. Comments for us? Please let us know. Want your own subscription? Request one here. All information shared is from public sources or used with express permission.

|

|

Massena Associates provides process, policy, and implementation consulting on retirement savings programs and products.

Our clientele includes states, governments, policy organizations, and private sector providers. Our specialty – efficient, targeted results. We are an active speaker on retirement security topics, including state-facilitated programs, MEPs and more.

If you’d like to explore working together, we welcome the conversation. Connect with us here, and at 339-236-0684. |

|

Looking for a great retirement savings innovation resource? Led by Dr. Alicia Munnell, the Center for Retirement Research at Boston College develops and hosts terrific content and proprietary research related to states, financial security, social security, and more.

Pew’s Retirement Savings Project studies the challenges and opportunities for increasing retirement savings and is another great resource - check out the work of John Scott and his terrific team.

|

|

|

|

|

|

|