RETIREMENT SECURITY MATTERS

A forum for retirement innovation information sharing focused on

states, supporters, and service providers.

Vol 26 | March 11, 2021

|

|

Greetings! welcome! to Retirement Security Matters – where we talk about retirement readiness innovation by states, supporters, and service providers.

|

Anyone else experiencing a “psychological spring” to go along with the equinoxal one? We are – as we watch everyone around us start getting vaccinated! And we’re seeing it out in the retirement space too. Here’s a great update on the freshest news:

-

John Scott from Pew – what's working - we want to know

-

The latest state metrics – setting some new records

-

Nine states in action: Arkansas, California, Colorado, Idaho, Illinois, Massachusetts, Minnesota, Missouri and Virginia

-

Grant’s Go To’s: Let’s Talk Automatic Enrollment

-

New thought leadership from Aspen and research from Boston College … and a few Easter eggs you’re going to want to crack open immediately

-

And, you got it, Pix of the Week!

|

|

Overcoming Barriers: What's Working Now, What We Want Next

|

|

John Scott,

Pew's Retirement Savings Project

|

|

We know John Scott as the Director of the Retirement Savings Project for Pew Charitable Trusts, where his team includes Alison Shelton, Andrew Blevins, Mark Hines and Theron Guzoto. In this role he is thoughtful, measured, articulate. His team cranks out an incredible amount of useful research and interesting findings, which is why we knew it would be important to touch on some of the latest work. But, did you know he can shuck oysters with the best of them? Sometimes its these little talents that get us through a pandemic! Read on for some great stuff. |

|

Greetings John! let’s jump into the deep end of the pool: what are some of your top focus areas with the retirement savings project at Pew?

(splash!) I’ll share three basic areas we're working in. We started early on by examining the barriers to retirement savings. We then looked at possible policy initiatives. That led us to the state Auto IRAs as being the most promising policy initiative to address barriers that workers face in trying to save for retirement, and that employers face in trying to offer retirement benefits to their employees. So that’s one focus area.

|

|

The second one is somewhat related. In the course of that earlier barriers work, we identified a gap for contingent workers. This is a broad term that covers a lot of non-traditional workers, whether that's independent contractors or gig workers or temp workers. To us it’s the group of people that don't have a direct employee-employer relationship, and also don't have the normal payroll system access that a lot of us use to save for retirement. So, we're focusing on those contingent workers and trying to figure out how we can get them into the savings system.

The last area would be looking at once you have retirement savings, how can you preserve those in retirement? We are looking at how retiring workers make decisions about their assets: whether to keep them in an employer plan or roll them over into an IRA, how do they make choices about their investments and do fees matter to them, because we know fees can reduce savings over time. So we're trying to understand that asset growth and preservation dynamic as well.

That's a lot of waterfront – and we think you’re talking about increasing the level of retirement security and confidence for Americans. Why does this matter and what's your biggest concern?

Well, taking a step back, I've always been taught by my parents that you can judge a country by how it treats the most vulnerable in its population. While elderly poverty is roughly half that of childhood poverty, many older Americans are just a few steps away – a job loss, health shock, unexpected bill -- from slipping into a reduced standard of living, if not outright poverty.

Most importantly, it’s entirely preventable. A failure to act on retirement security doesn't just reflect on us morally, but it's also a cost that we share as citizens and taxpayers. (… you know this piece is continued … read on here.)

John, we appreciate your focus on the big picture, long term! If you’d like to connect directly with John Scott, you can reach him here. You can follow John’s work and adventures on Twitter at @JohnCScott_DC or on LinkedIn. And you can follow and engage with Pew’s Retirement Savings Project here.

|

|

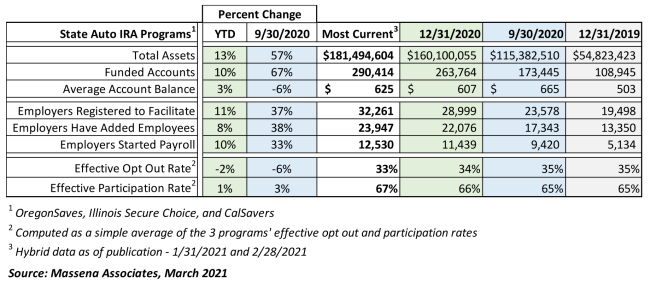

State Program Metrics - Auto IRAs |

|

What we see in these tea leaves – OK, a couple of things. Assets are closing in on the $200 million mark. Underneath the tea leaves, California’s assets are up almost 50% year to date. Yes, in the two months from December 31 to February 28.

More impactfully, these three programs are nearing 300,000 funded accounts. In fact, funded accounts are up by two-thirds since just September. Average account balances are on the rise to over $625, including new accounts. Opt-out rates have declined over this period and effective participation rates are up by about 3% since September and 1% YTD.

32,000 employers are now registered to facilitate – up 11% year to date. 12,500 employers have started payroll deductions – up 10% year to date and 33% since September 30.

|

|

State Facilitated Retirement Programs in Rollout, Study and Leg Mode |

|

Arkansas (workforce 1.4 million) – The Legislature’s Joint Committee on Public Retirement and Social Security Programs met this week on Monday. The agenda included HB 1349, the Every Arkansan Retirement Plan Opportunity Act creating a Multiple Employer Plan. Representative Les Warren described the proposed program, intended to serve as an incubator for small plans. Amendments introduced would now create a transition point when employer plans reach $600,000 requiring them to exit the program. The bill passed out of committee as amended with one “no” vote by Senator Jason Rapert, who argued that an Arkansas MEP would replicate offerings currently available to employers.

|

|

California (workforce 17.9 million) – coming very soon: CalSavers’ next employer deadline. June 30 is the date for employers with 50+ employees and no retirement plan to register to facilitate the program. Expect to see another big bump in facilitating employers, funded accounts, and assets.

|

|

Colorado (workforce 2.4 million) – The Colorado Secure Savings Program Board met March 10 (scroll for agenda) to further its work on planned program and investment consulting RFPs. The Board is targeting a March 15 week publication of RFPs.

|

|

Idaho (workforce 0.8 million) – Idaho’s bill, HO 180, which would establish a new retirement program for workers who do not have an employer-sponsored retirement program, was introduced February 16, 2021, and referred on to committee.

|

|

Illinois (workforce 5.7 million) – The Illinois Secure Choice program has proposed legislation for the 2021 session; most recently the bill has gone to committee for review.

|

|

Massachusetts (workforce 3.1 million) – which sponsors the CORE Plan for Nonprofits (a MEP administered by industry powerhouse Empower) has also introduced a bill that would authorize a Secure Choice Retirement Savings Program (Auto IRA). The state’s MEP is available to a limited set of employers today: nonprofits with 20 employees or fewer. This leaves a large segment of the workforce continuing in an uncovered status.

|

|

Minnesota (workforce 2.8 million) – HF 1258 was introduced February 18, 2021 to establish the Minnesota Secure Choice Retirement Program – consisting of both a Multiple Employer Retirement Plan (a MEP) by January 2025 and an Individual Retirement Account Plan (Auto IRA) by January 2023. Referred on to committee.

|

|

Missouri (workforce 2.5 million) – introduced HB 1299 on February 22, 2021 to establish the Missouri Workplace Retirement Savings Plan, a multiple-employer plan. It was referred to the House Pensions Committee March 4, 2021. A companion bill, SB 298, was heard in the Senate Health and Pensions Committee February 24, 2021.

|

|

Virginia (workforce 3.8 million) – Following on the heels of its thoughtful report, Virginia proposed legislation which has 🌟 passed 🌟 the General Assembly and is now headed to the Governor for signature. Here’s a piece on the legislation from NAPA, the National Association of Plan Advisors.

|

|

Grant's Go-To's: Automatic Enrollment and Escalation |

|

Anyone working on a state-facilitated auto-IRA program has probably been asked at some point why a state should offer a savings product already available through banks, credit unions and other financial institutions. The answer? State-facilitated programs – whether Auto IRAs, MEPs or Marketplaces – are designed to significantly increase retirement savings by reaching workers at the workplace and by including automatic features that make participation more likely.

Behavioral economists suggest people fail to save for retirement because of inertia and because of shortsightedness that leads most of us to value immediate gratification over the long-term benefits of saving now for the future. These are precisely the obstacles workplace automatic enrollment plans are designed to overcome.

Research provides convincing evidence in support of workplace plans with automatic features. An often-cited …

|

|

... Given that people tend to take the path of least resistance when it comes to retirement savings, states with retirement savings programs and initiatives should be applauded for paving that path in a direction that leads to greater participation and savings.

In the next edition we’ll explore the range of investment options state-facilitated programs have adopted.

Stay tuned! / Grant

|

|

This week Boston College’s Center for Retirement Research notes that Federal Minimum Wage is 40% Below 1968. While that’s technically not a retirement issue, in practicality, it is a retirement security-related challenge. Having a little more disposable income puts folks in a better position to save for retirement – and emergencies.

March is a great month to lean in on influential, world changing women. Does Ladybird Johnson come to mind? If not, we have a surprise for you: In Plain Sight: Lady Bird Johnson is a great new 8-part podcast by author Julia Sweig. Do not miss it! And our latest download, possibly saving the best for last? Just as I Am: a Memoir by fan favorite Cicely Tyson. |

|

... oh man, so much scrolling to get to these PIX! |

|

We promised you oyster shucking – and check this out! John Scott is lucky enough to live within a 10 minute walk of the Chesapeake Bay and a 30 minute drive from a local waterman who will sell oysters direct from his weekly catch. Here’s a little shucking at home for dinner prep. We’ll be right over.

|

|

No, you don’t need a rod and reel to catch oysters … the Scott family likes to vacation in the Finger Lakes of upstate NY, where John grew up – it’s a great place to hike and fish. John has a confession for you: “Despite what it looks like, the fish are generally safe with me.”

Does anything ever get this upbeat guy down? Eh, we hear that “policy work at Pew is rewarding, but our contracting procedures can be rigorous.” Very, very rigorous.

|

|

|

|

Meanwhile in the Northwest, spring is coming. 🌷

ALMOST makes up for the devastation we experienced last month when all our trees fell down.

|

|

OK, that’s a wrap. ❤ Hug your people and change the world.

If you like this piece, please stick with us. We’ll be back in about two weeks. If you don’t like it, please unsubscribe below. Comments for us? Please let us know. Want your own subscription? Request one here. All information shared is from public sources or used with express permission.

|

|

Massena Associates provides process, policy, and implementation consulting on retirement savings programs and products. Our clientele includes states, governments, policy organizations, and private sector providers. Our specialty – efficient, targeted results. We are an active speaker on retirement security topics, including state-facilitated programs, MEPs and more.

“We would not be where we are without Lisa’s great leadership and direction.”

If you’d like to explore working together, we welcome the conversation. Connect with us here, and at 339-236-0684. |

|

Looking for a great retirement savings innovation resource? Led by Dr. Alicia Munnell, the Center for Retirement Research at Boston College develops and hosts terrific content and proprietary research related to states, financial security, social security, and more.

Pew’s Retirement Savings Project studies the challenges and opportunities for increasing retirement savings and is another great resource - check out the work of John Scott and his terrific team.

|

|

|

|

|

|

|