Each month in our Signals newsletter, we share the latest results from Pulse Perspectives, our pulse survey designed to amplify the voices of independent school leaders across a wide range of roles and responsibilities and to provide a snapshot of high-level data, giving our community a clear picture of emerging trends and perspectives.

Beginning this month, we’re taking it a step further. A couple of weeks after each survey release, you’ll receive a follow-up article delivered directly to your inbox. This piece will dive deeper into the data, exploring insights through the lens of school size and key demographics to help you better understand how different types of schools are experiencing and responding to the issues in an evolving educational landscape. In the first edition, we take a closer look into the response from admissions and enrollment professionals and highlight some key insights from it.

|

The Evolving Admissions and Enrollment Landscape for SAIS Schools: Insights from the August 2025 Pulse Survey

By: Sheri Burkeen, SAIS Director of Research & Resources

The August 2025 pulse survey for admissions and enrollment professionals captured responses from 157 SAIS schools, representing a 40% response rate. The findings reveal a complex landscape where schools are navigating challenges while experiencing shifts in enrollment patterns, financial pressures, and the growing influence of school choice programs.

| | |

Current Enrollment Realities: Mixed Outcomes Across School Sizes

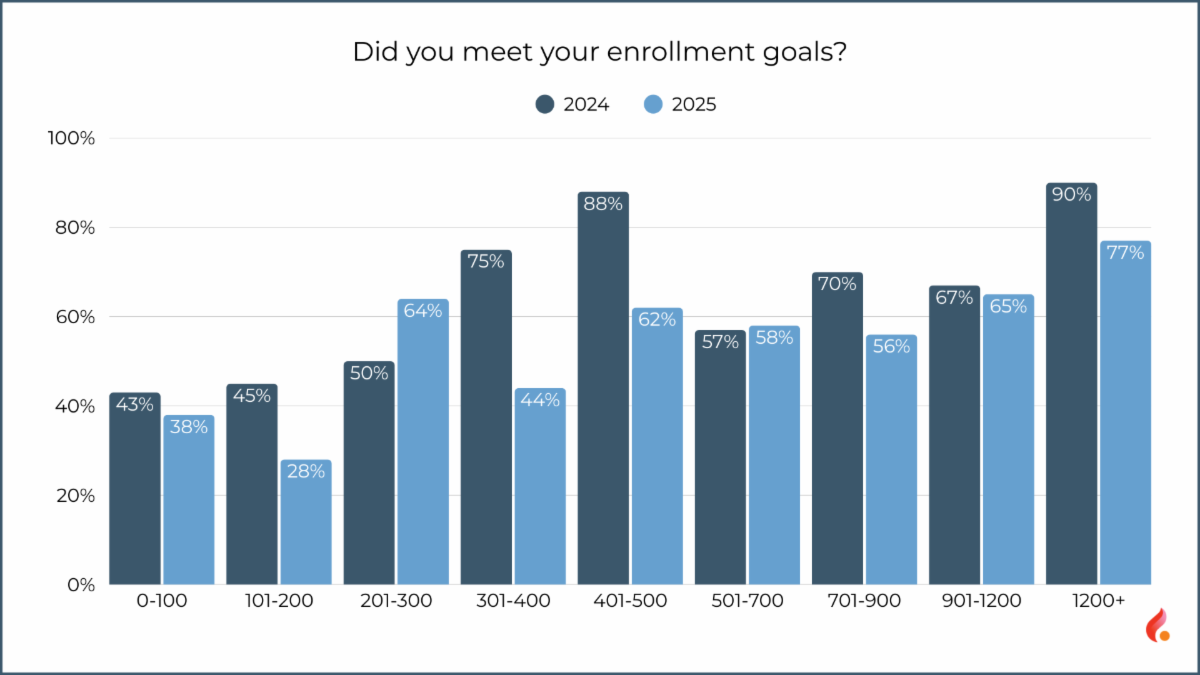

The 2025 survey reveals a nuanced picture of enrollment outcomes that varies significantly by school size. While 44% of schools report enrollment increases of 1-10%, the overall landscape shows downward trends in meeting enrollment goals. Only 54% of schools met their enrollment goals in 2025, representing a significant decline from 67% in 2024.

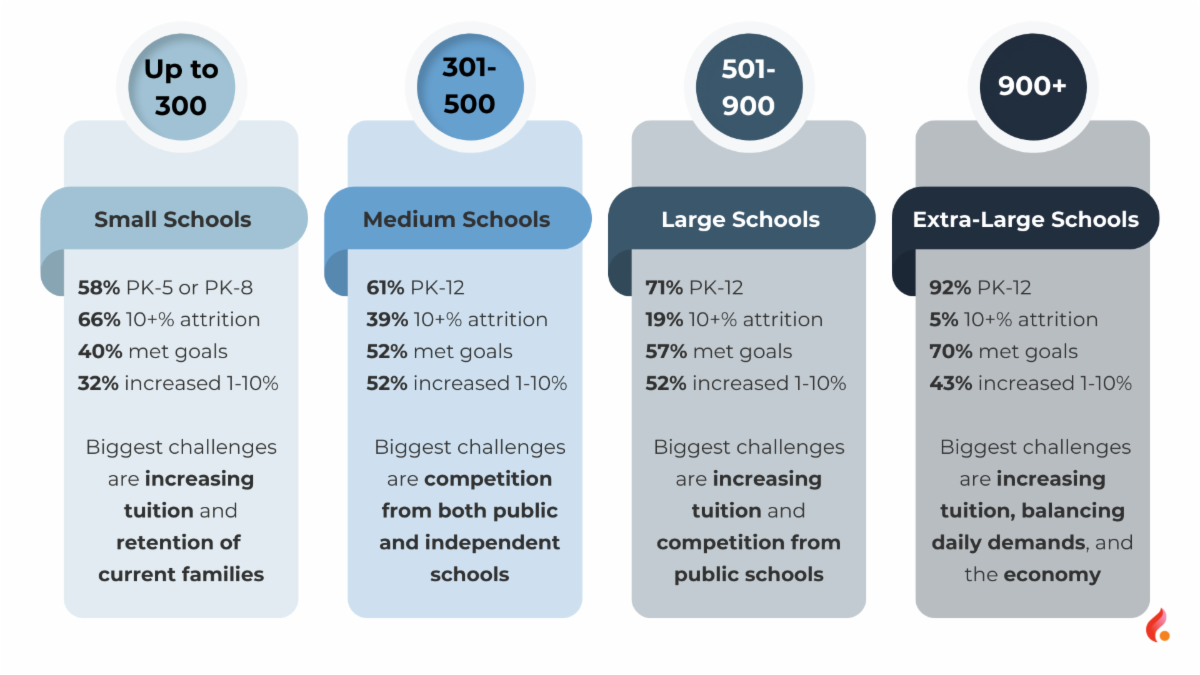

School size appears to be a contributing factor in enrollment success. Extra-large schools (over 900 students) demonstrated the strongest performance, with 70% meeting their enrollment goals, while small schools (under 300 students) struggled most, with only 40% achieving their targets, suggesting that larger schools may have the resources and stability to weather current market challenges.

| | |

The Attrition Challenge: A Growing Concern

Perhaps most concerning is the increase in schools experiencing high attrition rates. Schools reporting attrition rates of 10% or higher jumped from 25.6% in 2024 to 33.1% in 2025. This trend is particularly pronounced among smaller schools, where 66% report attrition rates exceeding 10%, compared to just 5% of extra-large schools.

The attrition patterns also reveal divisional differences, with schools experiencing enrollment declines reporting that middle and upper school divisions are showing the greatest losses. Conversely, schools with enrollment increases are seeing their strongest gains in lower school and early childhood programs, aligning with the broader decade-long trend toward growth in younger grades.

| | |

The School Choice Surge: Expanding Access and Impact

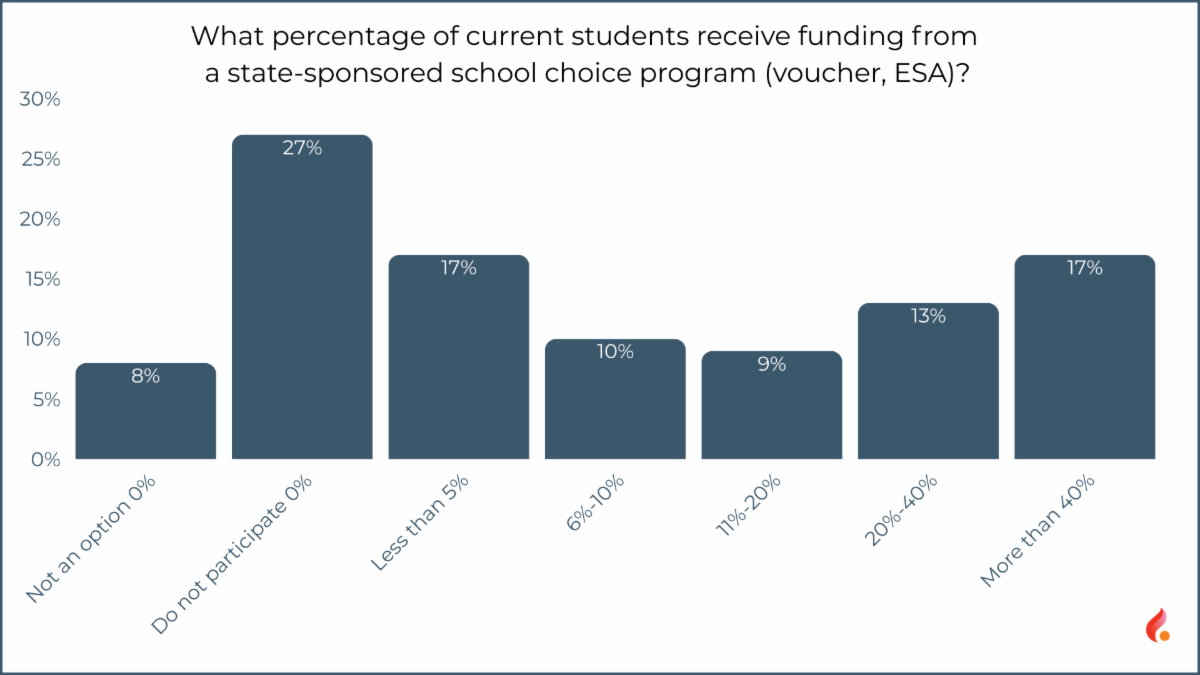

One of the most significant developments captured in the survey is the expansion of school choice programs across states where SAIS member schools are located. In 2024, 22% of schools indicated that vouchers and educational savings accounts were not available in their state or country. By 2025, this figure declined to just 8%, indicating rapidly expanding school choice options. However, 27% of schools surveyed choose not to participate in available programs.

Schools with high student participation rates (20-40%) in school choice programs increased from 4% to 13%, while those with 40% or higher participation more than tripled from 5% to 17%. Notably, smaller schools show the highest voucher and ESA participation rates, with 28% of small schools reporting that more than 40% of their students receive funding from state-sponsored school choice programs, doubling the 14% reported in 2024.

| | |

Financial Pressures: The Persistent Challenge

Financial challenges emerge as a theme across all school categories, though they manifest differently depending on school size and enrollment trends.

Financial Challenges: Concerns include increasing tuition costs (40% of schools up from 30% in 2024), the economic and employment landscape of their communities (31% up from 20% in 2024), and financial aid availability (26%).

Competition Challenges: Schools face pressure from both public schools (34%) and independent school competitors (29%). Half of rural schools and 34% of suburban schools specifically cite competition from local public schools as a significant challenge.

Operational Challenges: Particularly for larger schools, balancing daily demands with strategy emerged as a key concern.

| |

The Inquiry Pipeline

While 29% of schools report inquiry levels remaining the same as 2024-2025, the patterns vary significantly by school size. Medium schools (300-500) are seeing the strongest inquiry growth, with 59% reporting increases, while extra-large schools are experiencing declines, with 32% reporting inquiries down 1-10%.

| | |

Looking Forward: Strategic Implications

The expansion of school choice programs represents both an opportunity and a challenge, providing new funding sources while potentially increasing competitive pressure. The strong performance of early childhood programs suggests that schools investing in comprehensive early learning offerings may be best positioned for sustained growth.

The difference between large and small schools' performance indicates that size may increasingly matter in the current environment. Small schools face the dual challenge of higher attrition rates and greater difficulty meeting enrollment goals, while larger schools demonstrate more stability and success in achieving their targets.

| | |

Guiding Questions for School Leaders

As school leaders consider implications for their own institutions, the following questions may guide productive discussions and strategic planning:

-

How does the school's attrition rate compare to similar-sized institutions, and what specific retention strategies might be implemented to address the factors prompting families to leave, particularly in middle and upper school divisions? Developing an enrollment journey map for this specific persona may help identify gaps or pain points in the process.

- Considering that only 54% of schools met their enrollment goals in 2025, how might we refine our value proposition and enrollment strategies to stay competitive and ensure our goals reflect current market realities? Consider conducting a SWOT analysis and, when focusing on strengths, narrow down to 2-3 unique strengths to leverage.

- As financial challenges continue to dominate school concerns, particularly around increasing tuition and wider economic conditions, what innovative approaches to tuition, financial aid, and communication of our value proposition might we explore to maintain accessibility while ensuring financial sustainability?

| |

Additional Resources From SAIS

| | | | |