The Guam-Micronesia Mission of Seventh-day Adventists Retirement Plan (the “Plan”) makes saving for retirement even easier by offering an automatic enrollment feature for all newly-hired eligible employees. Newly hired employees will be automatically enrolled in the Plan at a 3% salary reduction contribution level. This 3% contribution will be deducted from your eligible compensation each pay period and contributed to the Plan as a salary reduction contribution. You can choose to contribute more, less, or even nothing, or choose to have the 3% deducted as a Roth contribution, by contacting Tara Brecht (GMM), Raeann Garrido (Guam Clinic) or ASC Trust to elect a Roth contribution, a different contribution percentage or no contribution at all. Keep in mind that if your employer makes matching contributions, it will match one dollar for each dollar you contribute, up to 3% of your eligible compensation.

The Plan also has an automatic escalation feature. All eligible Plan participants who are not making salary reduction or Roth contributions of at least 7% on July 1, 2022 will automatically have their salary reduction contribution increased by 1% at that time. Thereafter, each July 1, your salary reduction percentage will increase by an additional 1% until your contribution percentage reaches 7%. This automatic escalation feature will not change your salary reduction or Roth contribution level if you already participate at a 7% (or greater percentage) level. You can have these salary reduction contributions made as Roth contributions or change your contribution level at any time by contacting Tara Brecht (GMM), Raeann Garrido (Guam Clinic) or ASC Trust.

1. Does the Plan’s automatic enrollment feature apply to me?

The Plan’s automatic enrollment feature applies to all newly-hired eligible employees. This means 3% of a newly hired employee’s eligible compensation for each pay period will be contributed to the Plan as a salary reduction contribution, starting when you are hired and continuing through June 2022. Beginning on July 1, 2022, and every July 1 thereafter, your contribution level will increase by 1% (see question 2 for more information on the automatic escalation feature), until your salary reduction and Roth contributions reach 7% of your eligible compensation. To learn more about the Plan’s definition of eligible compensation, you can review the Plan’s summary plan description. Your salary reduction contributions to the Plan are taken out of your compensation on a pre-tax basis and are not subject to U.S. and Guam/CNMI income tax at that time. Instead, they are contributed to your Plan account and will be credited with market gains or losses. Your account will be subject to U.S. and Guam/CNMI income tax only when withdrawn (unless you make Roth contributions, which are taxed at the time of contribution). This helpful tax deferral rule is a reason to save for retirement through Plan contributions. You are in charge of the amount that you contribute. You may decide to take no action at this time and contribute 3% to the Plan, or you may choose to contribute an amount that better meets your needs. You can change your contribution levels at any time by contacting Tara Brecht (GMM), Raeann Garrido (Guam Clinic) or ASC Trust. Be aware that there are limits on the maximum amount you may contribute to your account. You may want to contact ASC Trust or your tax advisor to find out how these limits affect you. The limits are also described in the Plan’s summary plan description.

2. Does the Plan’s automatic escalation feature apply to me?

If you are not contributing at a 7% level on July 1, 2022, your salary reduction contributions will automatically increase by 1% at that time. Every July 1 thereafter, your contribution level will increase another 1% (unless you choose a different level or notify your employer or ASC Trust that you want to opt out of the Plan’s automatic escalation feature), until your salary reduction contributions reach 7% of your eligible compensation. Each year, you can elect to make these contributions as Roth contributions, elect a different percentage contribution to the Plan or to not contribute by contacting Tara Brecht (GMM), Raeann Garrido (Guam Clinic) or ASC Trust.

3. In addition to the contributions taken out of my compensation, what amounts will my employer contribute to my Plan account?

Your employer may make contributions to your Plan account. Your employer may match, on a dollar-for-dollar basis, the first 3% of eligible compensation you contribute each pay period. Your employer may also make an additional basic contribution of 3% or 5% of your compensation. Your employer determines which employees are eligible for matching or basic contributions - if you have questions about whether you are eligible to receive employer matching or basic contributions, please contact your employer.

4. How will my Plan account be invested?

The Plan lets you invest your account in a number of different investment options. Unless you choose a different investment option or options, your Plan account will be invested in the appropriate target date default fund based on your assumed retirement age. You can change how your Plan account is invested among the Plan’s investment options by contacting Tara Brecht (GMM), Raeann Garrido (Guam Clinic) or ASC Trust.

To learn more about the Plan’s investment options and procedures for changing how your Plan account is invested, contact ASC Trust.

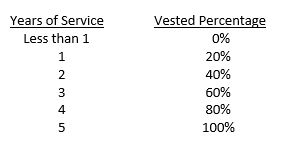

5. When will my Plan account be vested and available to me?

You are always fully vested in your salary reduction, Roth and rollover contributions to the Plan. You will also always be fully vested in the amount in your account merged into this Plan from the 401(k) Plan. Any employer contributions (both matching and basic) will vest according to the following 5-year graded vesting schedule: