When you are an investor, you have to expect good years and bad years. This has been a great year! OK, now what? | | Market Update - December 2025 | |

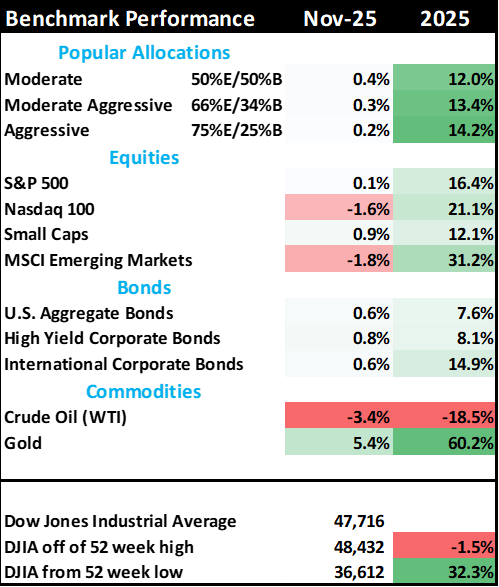

- Stocks sold off about 5% mid-November but rallied back to unchanged by the end of the month. Health care and Energy stocks did well, while Technology and Real Estate fell the most. This is normal chop in a calm market.

- Bonds maintain a slow grind higher; yields are falling as the Fed continues to cut interest rates. We expect a rate cut in December, then a gradual reduction in rates to 3% by the end of 2026.

- Silver has risen sharply, but not as much as gold has over the last few years. There are tremendous fears that the central banks are deliberately debasing the global currencies. These fears are justified, sadly.

- Inflation remains muted at 3%, but well above the Fed's 2% target.

| | Table 1: Market performance estimates as of 11/28/2025 (LIMW) | | November experienced normal choppiness | | |

November was a choppy month where the market didn't really go anywhere. This is quite normal, but there was tremendous fear mid-month that the Fed would not continue rate cuts or that the artificial intelligence narrative was changing.

For now, the markets are expecting another 25-bps interest rate cut by the Federal Reserve in December and further rate cuts down to 3% in 2026. The spending freight train on artificial intelligence continues unabated; Nvidia announced they had completely sold their chip production in the most recent quarter.

However, valuations are high, there are problems in the private credit space and the middle and lower classes are getting squeezed horribly by inflation.

Figure 1: S&P 500 performance 2020-2025 (LIWM)

| | |

Despite the fear of more inflation, the bond market has done reasonably well this year. It is our view that the bottom for this cycle is in for the bond markets. With Fed rate cuts and inflation at a tolerable 3%, there is room for this market to move higher if ANY problems crop up in the broad economy.

Figure 2: Aggregate bonds 2019-2025 (LIWM)

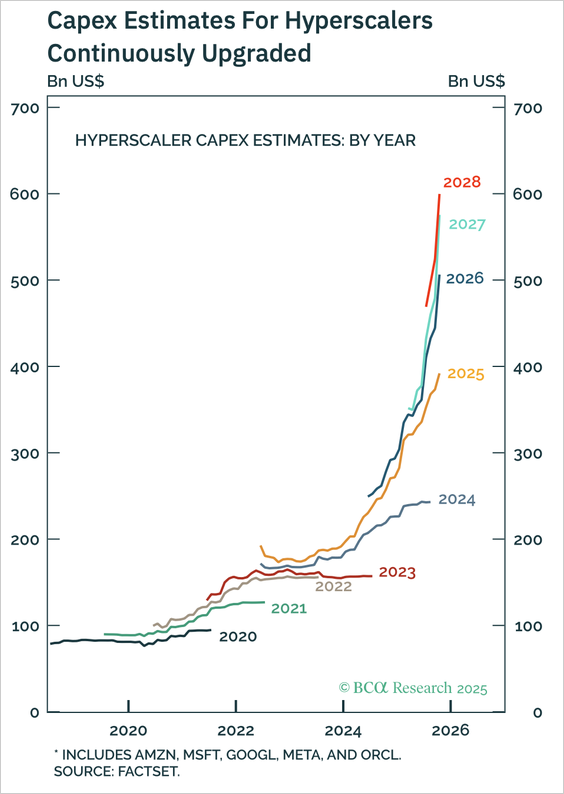

| | It's not the data centers; it's the power supply | | |

Many investors are focused on the capital spending intentions of the large players in the artificial intelligence space: Amazon, Microsoft, Google and Oracle are some of the big names that have poured billions into data centers designed to deliver this service.

Anything that interferes with this parabolic trajectory of spending will affect the investment thesis for dozens of technology stocks, especially those leading the current stock market.

Figure 3: Capital expenditure estimates for the "hyperscalers" in AI by year (Factset)

| | |

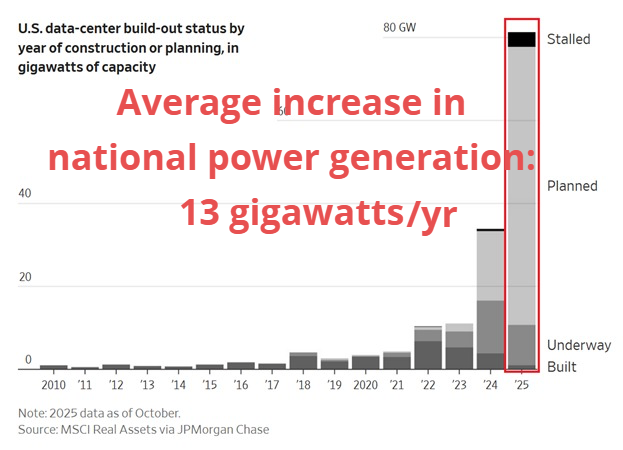

The problem is not access to high end chips. It is a much more mundane problem: no excess electricity supply. No power; no power computing.

For example, here is a study that estimates how much power will be needed by planned AI projects. This all sounds great. The only problem is that over the last 20 years, the average increase in power supply in the United States is 13 gigawatts PER YEAR.

This isn't like a movie where you say, "If you build it, he will come." No, this is the real world where it takes years to build new capacity, the utility business is highly regulated, and nobody wants new generation units in their backyards. It is a real problem.

| | Figure 4: Data center build out status by year (JP Morgan) | | |

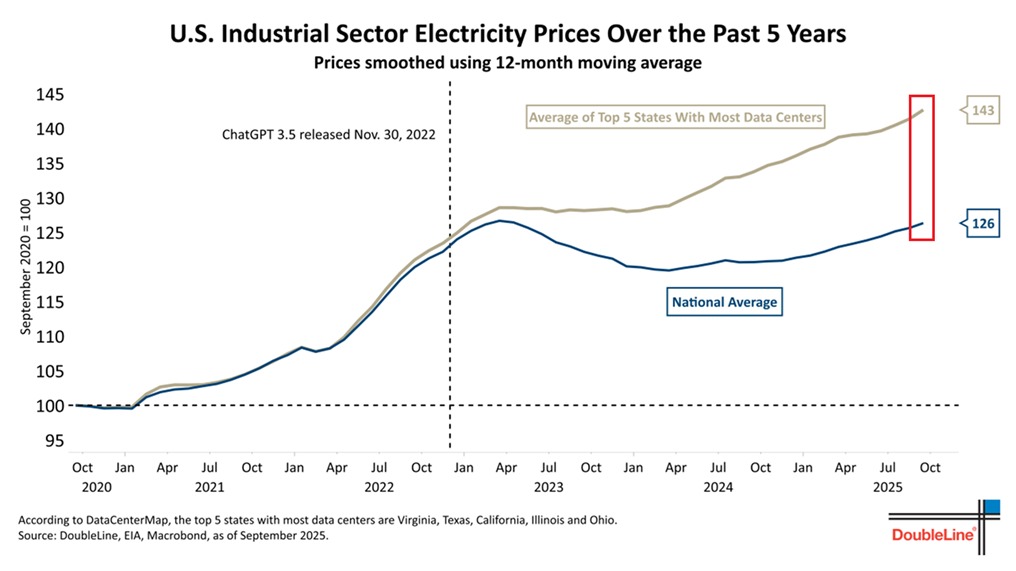

There are also signs that this increase in demand for power is pushing up base power pricing in regions where data centers are prevalent. The broad base of electric customers is paying for the excess demand caused by heavy data center use.

Figure 5: Price comparison of data center regions (Double Line)

| | |

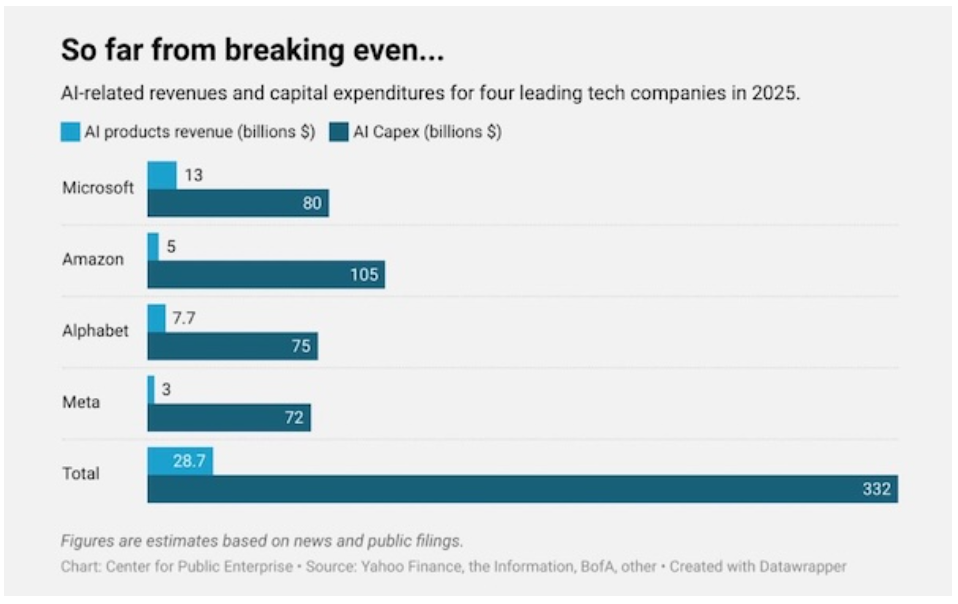

On top of that, there is a huge mismatch between revenue and capital expenditure. Hyperscalers are building like crazy to get the first mover advantage, but it is not clear how or when these investments will turn into a revenue generating business. Risk is very high.

If the AI revolution plays out the same way as the year 2000 Tech Bubble, expect lots of financial problems with the early movers, a collapse in stock prices, but with an eventual group of winners that will come out on the other side. For example, in 2002 after the tech bubble collapsed, new firms such as Google, Facebook and Twitter emerged that created new business models based on the technology buildout of the late 1990s.

Figure 6: AI Capex and Revenue comparison (Center for Public Enterprise)

| | Inflation is a major problem | | |

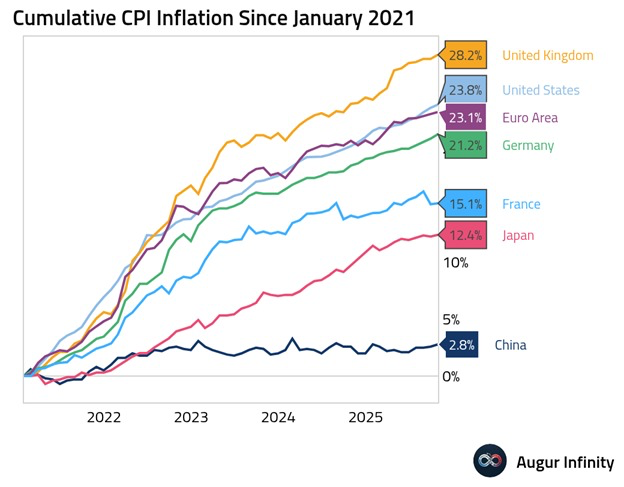

Unless you have very high levels of wealth, you probably are noticing how badly inflation is squeezing the budgets of the middle and lower classes. This is not an imaginary phenomenon; your dollars are worth a lot less than they were 5 years ago.

Your spending power is down about 24% in the last 5 years.

Figure 7: Decline is spending power of major currencies (Auger Infinity)

| | |

But the message is even worse if we look at history. When governments take on too much debt, inflation is one of the easiest ways to quietly default on their debtor obligations.

"By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens. This method allows governments to confiscate arbitrarily, enriching some while impoverishing many, and undermines confidence in the equity of the existing distribution of wealth."

John Maynard Keynes, Economist, 1919

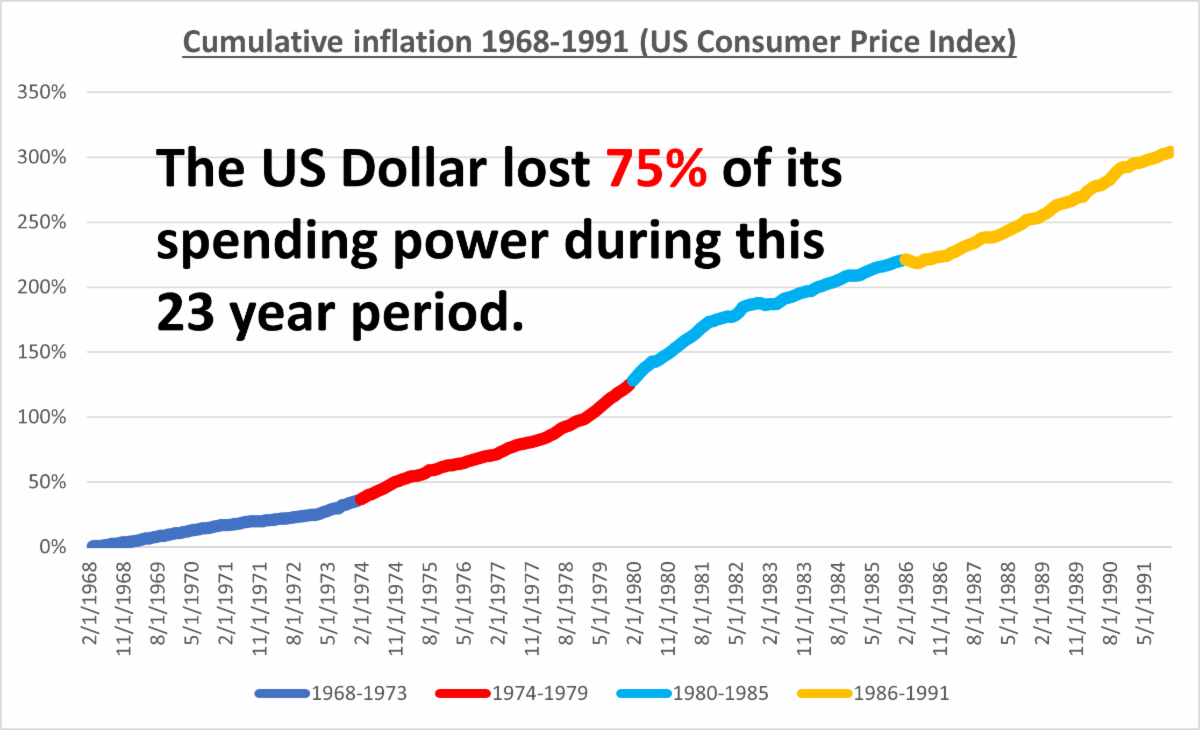

When people think of hyperinflations, they think of Weimar Germany, Zimbabwe, but certainly not the United States. What if I told you that during the 1970s and 1980s, our government allowed the value of the currency to fall 75%!

That is exactly what happened 1968-1991 during the worst of that inflationary period.

Figure 8: Consumer price index cumulative inflation 1968-1991 (Bureau of Labor Statistics)

| | |

For those who grew up in the New York tri-state area, you may recognize this guy. He was the actor in all the Crazy Eddie commercials that would end each cut with the catch phrase "His prices are INSANE!!!!"

We don't like to think our government is insane, but they have historically allowed inflation to run out of control for long periods of time for reasons that suit themselves, to the obvious detriment of all citizens.

| | |

It is obvious what strategy the governments of the world are using to deal with record levels of government debt. They are inflating it away.

While this is the long-term strategy for governments, in the short-term, there is an economic cycle playing out that is affected by several offsetting factors:

Bullish factors:

- Fed cutting interest rates; halting quantitative tightening.

- Trump tax cuts going into effect during 2026.

- $2 trillion of deficit spending by the federal government.

Bearish factors:

- Unresolved bond losses by banks from 2021.

- Commercial real estate weakness.

- After effects of the Fed's 5% interest rates 2 years ago.

- Tariff wars suppressing demand.

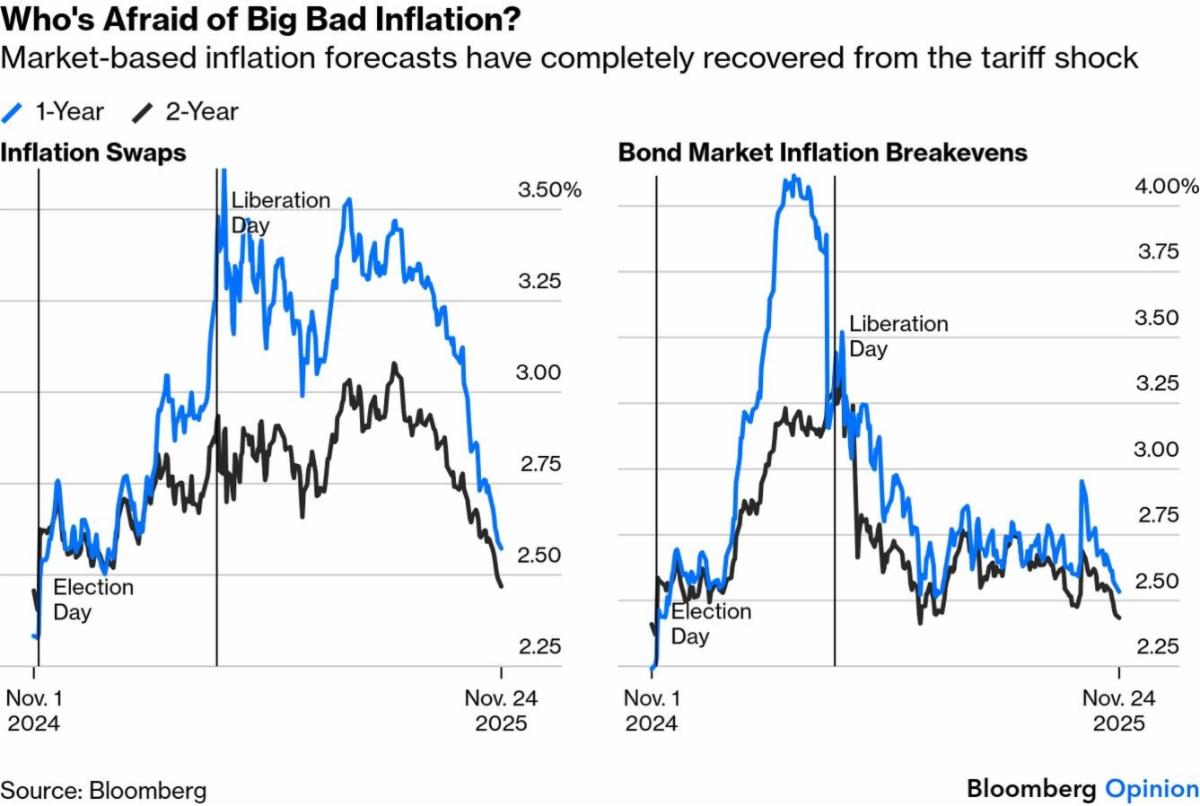

For now, inflation is ebbing and the markets expect yields to fall in the near future. This is bullish short-term for bonds.

Figure 9: Short-term interest rate indicators (Bloomberg)

| | |

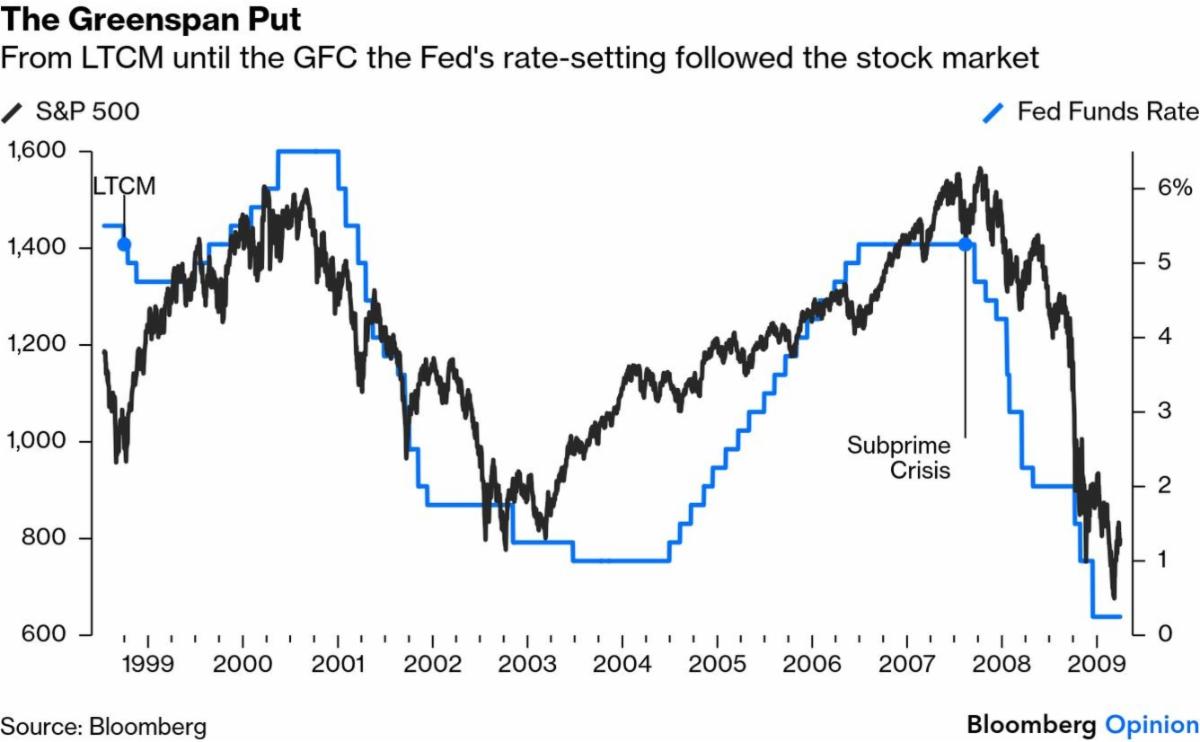

Common knowledge says that Federal Reserve rate cuts are bullish. However, historically, there is a lag between the rate cuts and subsequent positive action in the markets. Why does this happen?

From the Fed's perspective, they cut rates to avoid problems. It might be a bank crisis or impending recession, but cutting rates is an insurance policy against a severe economic downturn. So, let's not get too far ahead of ourselves in getting excited over Fed rate cuts.

Figure 10: The Greenspan Put: Federal Funds rate v. S&P 500 (Bloomberg)

| | |

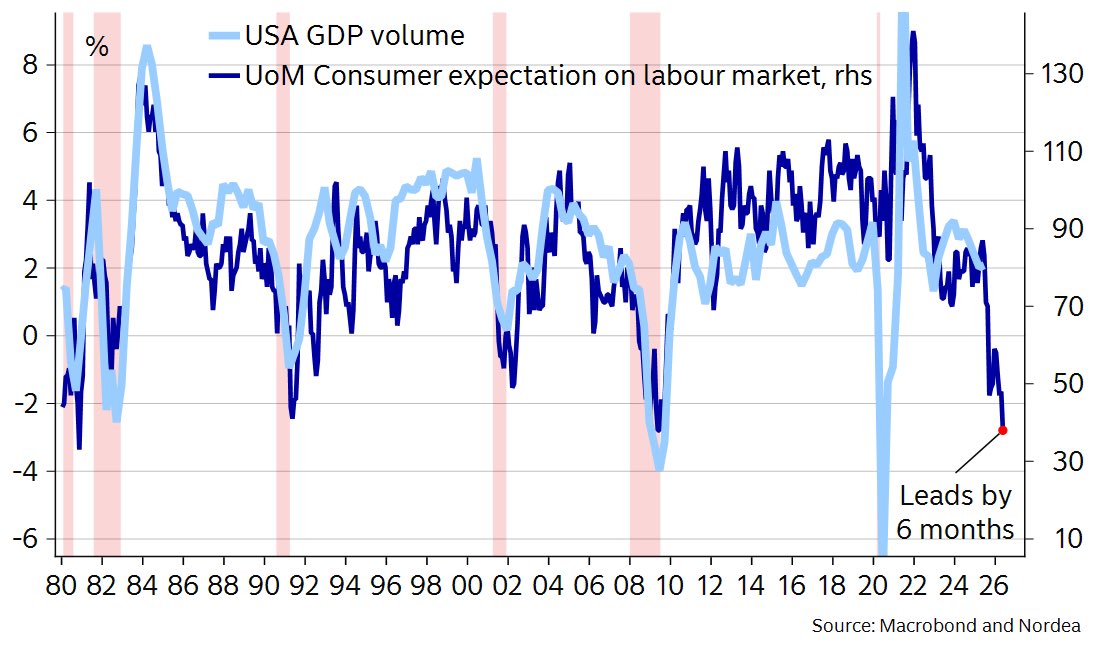

The latest readings on consumer confidence are quite bleak. For now, this doesn't matter because consumer spending has been gradually skewing towards the wealthy over the years. The latest estimates are that about 50% of consumer spending is driven by high-net worth activity. As long as the stock market holds up, we expect consumer spending to remain firm.

Figure 11: Consumer expectations for labor (University of Michigan)

| | |

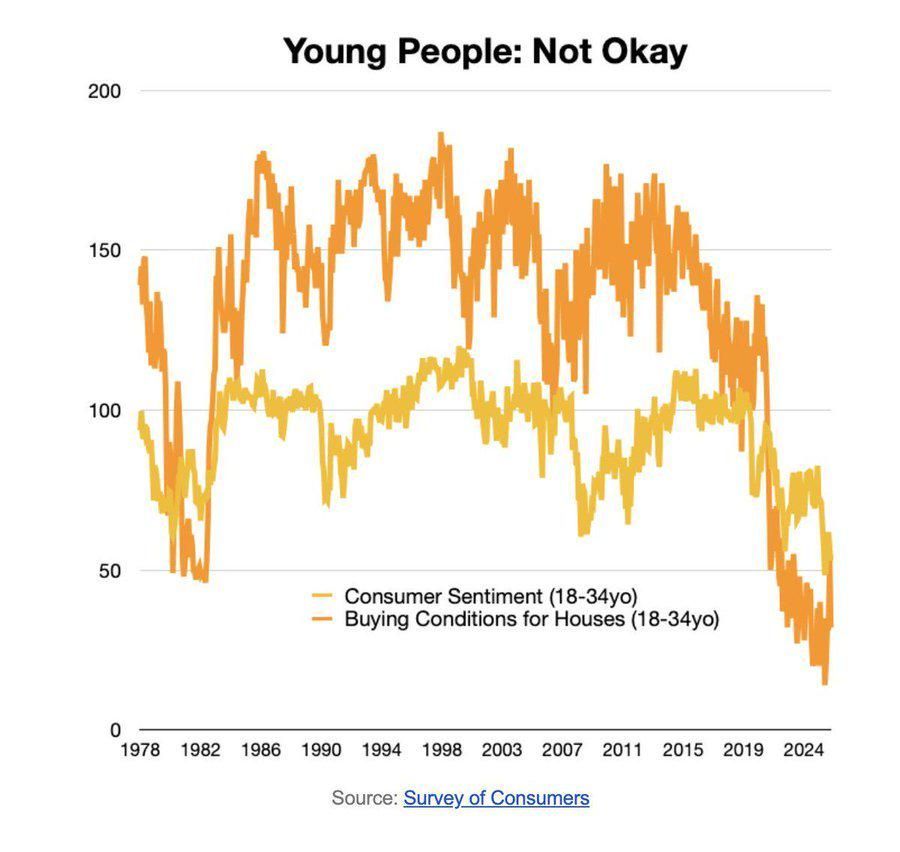

In particular, consumer confidence among the young is very bad. These readings are stunning.

Figure 12: Consumer confidence of the young (Survey of consumers)

| | Interesting similarities to the year 2000 top | | |

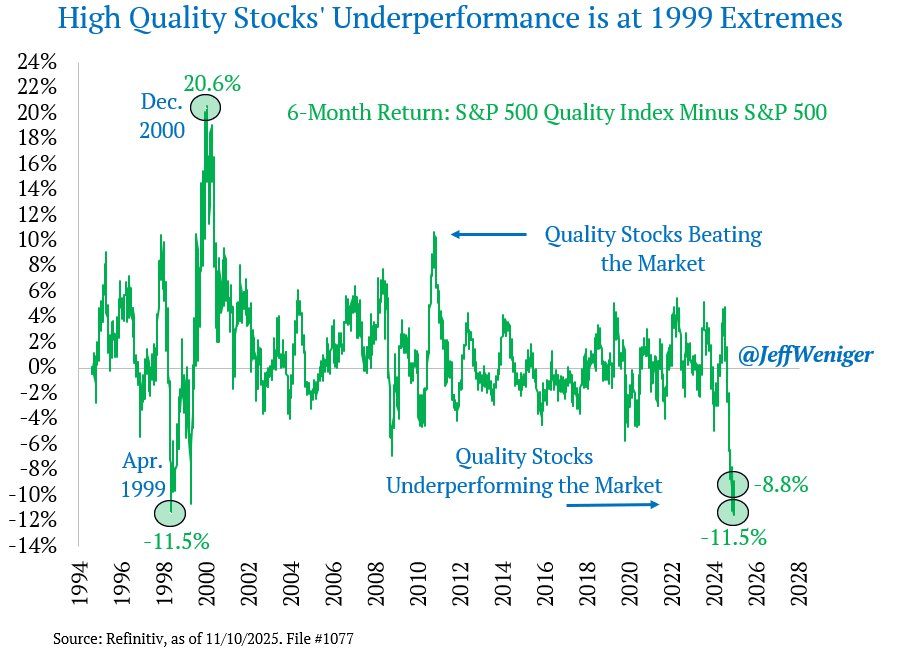

If technology stocks are in a bubble, then where should you look for new ideas in the stock portion of the portfolio? This is a great question.

The behavior of high quality stocks mirrors that of the late 1990s. During this period, many stocks classified as "value" or "high-quality" performed terribly as the tech stocks marched higher. Many portfolio managers with this quality bias were fired back then and replaced with managers who liked tech stocks. This did not work out great for the clients, by the way.

Typically, high quality stocks are utilities, energy, health care or consumer staples companies. This is a good starting place for new ideas IF there is a break in the current tech stock narrative. Please call us if you would like to discuss it in detail.

Figure 13: High quality stock performance (Jeff Weniger)

| | |

It has been an interesting year. Our strategy of changing asset allocations at extremes worked well: after being underweight stocks in the 1st quarter 2025, we rotated into stocks during the April sell-off and rode most of the rally overweight stocks till late August. This worked out well for our clients and we are grateful for their support.

In an era of rising and sustained inflation, this type of asset allocation strategy may prove valuable. If the 2020s are anything like the 1970s, there will be wild swings in stocks and bonds as the cycle changes. We believe in taking advantage of those swings.

As always, we welcome your feedback and are happy to discuss our research and how it applies to your situation.

| | |

Rob 281-402-8284

Chris 281-547-7542

| | |

Christopher Lloyd, CFP ®

Vice President and Senior Wealth Planner

Lloyds Intrepid Wealth Management

1330 Lake Robbins Dr., Suite 560

The Woodlands, TX 77380

281-547-7542

Chris.Lloyd@lloydsintrepid.com

www.lloydsintrepid.com

| Lloyds Intrepid LLC is an Investment Advisor registered with the State of Texas, where it is doing business as Lloyds Intrepid Wealth Management. All views, expressions, and opinions included in this communication are subject to change. This communication is not intended as an offer or solicitation to buy, hold or sell any financial instrument or investment advisory services. Any information provided has been obtained from sources considered reliable, but we do not guarantee the accuracy, or the completeness of, any description of securities, markets or developments mentioned. We may, from time to time, have a position in the securities mentioned and may execute transactions that may not be consistent with this communication's conclusions. Please contact us at 281.886.3039 if there is any change in your financial situation, needs, goals or objectives, or if you wish to initiate any restrictions on the management of the account or modify existing restrictions. Additionally, we recommend you compare any account reports from Lloyds Intrepid LLC with the account statements from your Custodian. Please notify us if you do not receive statements from your Custodian on at least a quarterly basis. Our current disclosure brochure, Form ADV Part 2, is available for your review upon request, and on our website, www.LloydsIntrepid.com. This disclosure brochure, or a summary of material changes made, is also provided to our clients on an annual basis. | | | | |