|

China-

US Trade Conflict: Causes and Impact

|

|

Introduction

Most analysts agree that the

China-United States relationship

is interdependent as the word is taken to imply a

relative

view of international relations; different states are interconnected in multiple ways and therefore share mutual interests which they can pursue together. However, it is more accurate to say that interdependence means

mutual dependence

, where the ability of any state to pursue its aims is

dependent not only on its own actions but on the actions of others

. This is an important point to recognize because it highlights the fact that every country in the world has to actively

manage

its

external relationships

; the outside world is not something that can be ignored. In pursuing their aims, states therefore have to take other states' likely aims and actions into account, and they will expect other states to do the same. Such situations are described as ones of

strategic interdependence

. Accordingly, China and the United States are linked in so many ways in political, military, economic and cultural matters,

but

the degree of dependence may be very uneven and vary

as aspect to another.

|

|

Question 1: Background of China-US trade conflict

|

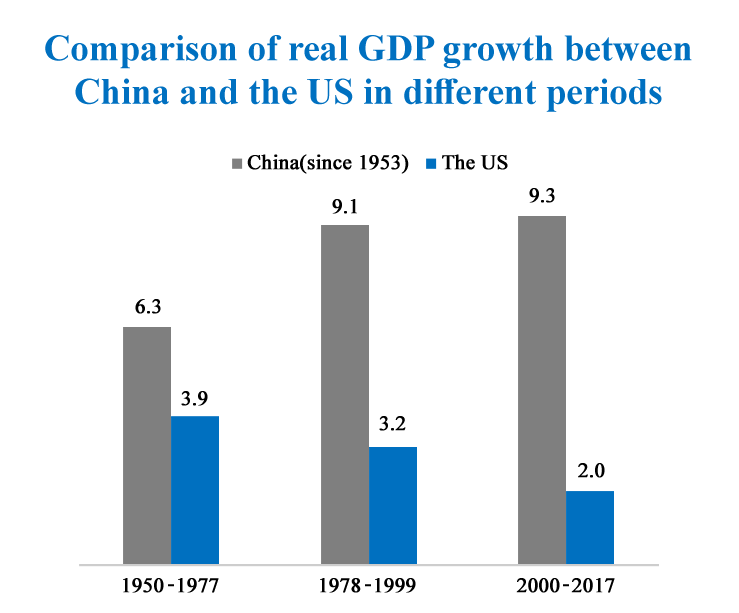

- Since 1950s, the US economic growth has been slowing down, while China economic growth has been continuously increasing. According to the World Bank, China economy could exceed the US in terms of total volume becoming the largest economy in the world in 2031, if the average economic growth of the US remained at 2% and China at 6% since 2018. In addition, if China contribution to the world economy would maintain its high percentages reaching 35.6% average in 2008 to 2016 in comparison to the US, which have low average percentage reached 7.4% from 2008 to 2016.

- The China-US economic and trade ties started to develop in the late of 1970s when both countries formally established diplomatic relations through entering into bilateral agreements. In 1980, total trade between China and the US was about 4.9 BN USD. At that time, China was the US 24th largest trading partner, 16th largest export market, and 36th largest source of imports.

- Over the past four decades, trade ties between the two countries have expanded drastically, in particular upon China agreement to the World Trade Organization (WTO) in 2001. China has now become the largest trading partner of the US, while the US is China second largest trading partner after the European Union (EU).

- In US, total merchandise imports from China amounted to 505.5 BN USD in 2017, an increase of 390% compared to 2001. Over the same period, its total merchandise exports to China have grown by 570% to 129.9 BN USD.

- On the US side, this represented a trade deficit in goods with China at 375.6 BN USD. On the other hand, the US maintained a trade surplus with China in services at a value of 40.2 BN USD.

- As indicated in the table below, the US percentage share of merchandise trade with China in terms of imports and exports stood at 21.6% and 8.4%respectively in 2017. From the perspective of China, the respective figures were 8.4%and 19%.

|

|

Question 2: What are the main causes of China-US trade imbalance?

|

- China can produce many consumer goods at lower costs than other countries. Americans, of course, want these goods for the lowest prices. Most economists agree that China competitive pricing is a result of two factors:

- A lower standard of living, which allows companies in China to pay lower wages to workers.

- An exchange rate that is partially fixed to the dollar.

- If US implemented trade protectionism, US consumers would have to pay high prices for their "Made in America" goods. It's unlikely that the trade deficit will change. Most people would rather pay as little as possible for computers, electronics, and clothing, even if it means other Americans lose their jobs.

- China current account has remained roughly balanced, with its balance occupying 9.9% of GDP at peak in 2007, and declining to 1.4%in 2017.

- The US trade deficit with China is still high, and 46% of total US deficit was with China in 2017, while 44.3% of total deficit was with the other seven countries.

Following the collapse of the Bretton Woods system, the US trade deficit began to rise

- US trade in goods has registered a continuous deficit since 1975. Under the Bretton Woods system, the dollar was convertible into gold; in this context, US deficit in foreign trade led to monetary contraction and then lower demand. In turn, this suppressed imports and promoted exports. Accordingly, the self-correcting mechanism was formed and the trade deficit shrank. However, since the US dollar was decoupled from gold in 1971, the US has been able to pursue its monetary policy freely, and the above-mentioned self-correcting mechanism has disappeared.

- Dollars earned in trade surplus countries are then channeled back to the US and support American purchases of foreign goods.

Upgrade of "World Factory" Export

- While China has surplus with Europe Union and the US, it has deficit with other countries, which can show the pattern of global industrial chain. China imports intermediate products and export final products, and the data over estimated China surplus with EU and the US.

- Considering the high percentage of processing trade in China total trade, China trade surplus amounts to one third, which is still very high. China-US trade deficit measured by traditional/ value-added method has risen up from around 40% in 2000 to 70%in 2015, indicating an upgrade of China export.

- Currently, US trade deficit with China is still high, but the added-value in China export is increasing gradually, which shows improvement of China industrial chain and industrialization, and great achievement that has been made during the process of transformation and upgrading of China industrial structure.

Difference in Savings rates

- Saving rate is an important factor to a country's trade balance.

- International comparisons suggest that a country's saving rate is highly correlated with its foreign trade balance. Countries with high savings rates usually have a trade surplus.

- Savings rate is also highly correlated with labor population as shown in China labor population which reached its peak in 2010, then decreased, and accordingly the saving rate declined.

|

|

Question 3: What is the impact on the Chinese economy ?

|

Impact on the Chinese economy

-

Industrial impact:

The US announcement of

25%

tariff on products worth

50 BN USD

on 22 March 2018 would largely affect industries linked to the "

Made in China 2025

" strategy in mid-and-long run. An additional tariffs on products worth

100 BN USD

could have impact on

consumer goods

and

labor-intensive industries

.

- Chinese household consumption accounted for 39% of GDP in 2016 and the same in 2017, much lower than in other major economies.

- China imports of consumption goods was 3.2% of household consumption or 1.3% of GDP in 2016, far lower than countries like the US and Malaysia, due to high tariff rates and distribution costs.

|

|

Question 4: What are the impact on the US economy?

|

- China pegs its currency to the dollar using a modified fixed exchange rate. When the dollar loses value, China buys dollars through US Treasuries to support it. In 2016, China began relaxing its peg. It wants market forces to have a greater impact on the yuan's value. As a result, the dollar to yuan conversion has been more volatile since then. China influence on the dollar remains substantial.

- China must buy so many US Treasury notes that it is the largest lender to the US government. Japan is the second largest. As of July 2018, the US debt to China was 1.17 TR USD. That's 19% of the total public debt owned by foreign countries.

- Many are concerned that this gives China political leverage over US fiscal policy. They worry about what would happen if China started selling its Treasury holdings. It would also be disastrous if China merely cut back on its Treasury purchases. By buying Treasuries, China helped keep US interest rates low. If China stopped buying Treasuries, interest rates would rise. That could throw the United States into a recession. But this wouldn't be in China best interests, as US shoppers would buy fewer Chinese exports. In fact, China is buying almost as many Treasuries as ever.

- US companies that can't compete with cheap Chinese goods must either lower their costs or exist the business. Many businesses reduce their costs by outsourcing jobs to China or India. Outsourcing adds to US unemployment. Other industries have just dried up. As these industries declined, so has US competitiveness in the global marketplace.

- However, in H1-2018 the overall US deficit in goods was up 7%. The deficit in China was up 9% and 16% with Europe. Those trends will almost certainly continue in H2-2018. Protectionism aimed at China will not have any big effect on the overall US deficit.

- The protectionism should eventually reduce imports from China, but it will also reduce US exports and increase US imports from other locations. Much of US imports from China are intermediate products used by US firms to be more competitive.

- Taxing these will naturally result in some lost business for US firms, both in the domestic market and in export markets. If the protection stays in place long enough, global value chains will adjust. Some labor-intensive final assembly will shift to countries like Vietnam in order to avoid the 25% tax.

- Suppliers such as Japan, South Korea and Taiwan will retain more production at home rather than off-shoring to China. China is likely to remain the center of the Asian production hub but will concentrate even more than it does now on intermediates and less on final goods for the US markets.

- All of this will shift some of the trade deficit away from US-China toward larger trade deficits with the rest of Asia and Europe. But the overall US trade deficit will not change in any significant way.

|

|

Question 5: Will the China-US trade conflict impact the emerging markets and the MENA refgion?

|

The trade war will definitely have implications in other markets

- The prospect of other countries being pushed to take sides could enlarge the scale of US-China trade conflict and the resultant spillover effects would be felt all over including the Middle East region. The impact of trade conflict would be most felt in the economic growth and immediately felt in the equity markets. The first is due to the decreased economic activity as demand for exports will fall and the second is due to the increased risk aversion that would mostly lead to withdrawal of capital from risky assets. As most of the Middle Eastern markets are classified as emerging markets, a capital outflows could be witnessed.

-

A trade conflict between the two largest economies in the world presents a

significant threat

to global economic growth and

stability

. A scenario where a trade conflict encourages other markets to begin adopting a

protectionist

attitude

may lead to

less demand

for some

UAE exports

which could

negatively impact growth

. The

uncertainty

from such developments may fuel risk aversion, consequently impacting

equity markets

and

local stocks

in the

Middle

East

. The Middle East could also be affected indirectly if the trade conflict

worsened

and

turned

to a trade war. The region accounts for

40%

of China oil imports and if industrial activity falls as a result of the trade war,

demand for oil exports

from the

MENA

could

fall

. Global trade tensions could negatively impact oil as it threatens global growth and could subsequently lower the demand for oil.

- The bullish price action witnessed in oil suggests that this risk has not been fully priced in; this is something that would need to be considered if a trade war becomes a reality. With the primary dynamics driving markets still based around geopolitical tensions and rising production from US, this could be another volatile trading quarter for oil.

- While the GCC countries have been steadily diversifying their economies, the primary income is still generated from oil revenues. Therefore, any volatility in oil could reduce confidence among investors and affect the regional markets. It is unsure how long the economic tension between the world's two largest economies will last. But the longer it lasts, the larger the impact will be on oil prices.

|

|

|

Conclusion

The China-US trade dispute is a long-term issue, and

perhaps,

huge threat of a broader changing bilateral relationship. However, there is still huge potential for trade and investment cooperation, considering the strong complementarity of the two economies. The two countries have responsibility to maintain the stability of global trade system, and should solve trade conflict through multilateral mechanism.

No one wins a trade war.

|

|

|

|

Dubai Office:

Office No. N 415, North Tower, Emirates Financial Towers, DIFC, P.O Box 506726, Dubai, UAE.

Tel:

+97142820301

|

Cairo Office:

Z

epter Office Building

S5-6,

Area 5, District 1, 5th Settlement,

New Cairo, Egypt.

P.O. Box:

1147

|

|

|

|

|

Please like and follow us:

|

|

|

|

|

|

|

|