|

Stocks Gain

The major U.S. stock indexes produced gains of around 2.0% in the first full trading week of 2026. The S&P 500 and the Dow surpassed record highs set two weeks earlier, and the NASDAQ climbed to within 1.2% of its historic peak set more than two months ago.

A U.S. small-cap benchmark outperformed its large-cap peers by a wide margin and eclipsed a record high set four weeks earlier. The Russell 2000 Index added 4.6% for the week. Over the past month and a half, the index has added nearly 14%.

Precious metals prices rebounded from the previous week’s declines, extending rallies that began to pick up momentum in early 2025. Gold was trading above $4,520 per ounce on Friday afternoon and near a record level set two weeks earlier. Silver surpassed $80 per ounce for the first time on Tuesday and was trading just below that record level on Friday afternoon.

Oil prices fluctuated widely amid a heavy flow of geopolitical news affecting commodity markets. The price of U.S. crude fell to as low as $56 per barrel on Wednesday before rebounding to as high as $60 on Friday, resulting in a more than 3% weekly gain.

Friday’s jobs report provided further evidence of a labor market slowdown. The economy generated a below-forecast 50,000 jobs in December, and initial estimates for the previous two months were revised downward by a combined 76,000 jobs. In 2025, payroll gains averaged 49,000 per month – less than one-third of 2024’s 168,000 average.

U.S. consumer sentiment is up for the second month in a row and at its highest level in four months, based on Friday’s preliminary monthly report from a University of Michigan survey. The index’s initial January reading was 54.0, up from December’s final figure of 52.9. Both results marked a modest rebound following a string of recent monthly declines amid weakening jobs growth.

The growth rate for dividend payments by U.S. companies accelerated in 2025’s fourth quarter. The $13.1 billion in net dividend increases recorded by companies in the S&P 500 was well above the previous quarter’s $10.6 billion, according to S&P Dow Jones Indices, which said it expects 2026’s first quarter to be a busy period for dividend increases due to record-high earnings and sales levels.

A Consumer Price Index report scheduled for release on Tuesday will show whether a recent downturn in inflation extended into December. The most recently released CPI report showed an annualized rate of 2.7% in November, well below economists’ consensus forecast for a 3.1% figure.

Source: John Hancock Investment Management

| | |

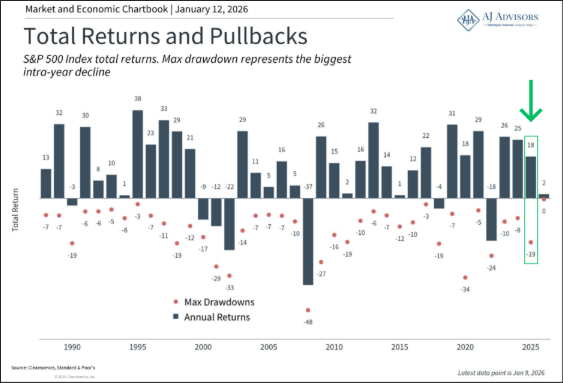

This chart shows total returns of the stock market (bars) and the largest intra-year decline (dots) each year. The average year sees a significant intra-year drop. However, most years still end in positive territory, especially with dividends.

In retrospect, 2025 (highlighted with a green arrow and box) was another typical year for the US stock market. The S&P 500 index returned 18% on the calendar year while experiencing a double-digit pullback as the market tends to do each year. Of course, the cause of the pullback is always something different. Volatility in prices is a normal part of investing. On average, the market experiences a 10-14% pullback most calendar years.

| | Retirement: Fighting the Inflation Battle | | |

We’ve all heard stories about how much – or how little – our parents and grandparents paid for their first car or their first home. In 1960s, a brand-new Oldsmobile cost less than $3,000, and the average U.S. home price was $17,800.

Rising prices – a phenomenon called inflation – are a significant risk to retirement. That’s why it’s critical to save as much as you can and invest it to keep pace with or beat inflation over time. In recent years, legislation has made it possible for American workers to boost the amount of money they’re saving in tax-advantaged workplace retirement plans, including:

- 401(k) plans, which are for private-sector workers,

- 403(b) plans, which are for public-sector and non-profit workers, and

- 457(b) plans, which are for government workers.

Catch-up contributions allow people to save more than the maximum plan contribution of $24,500 in 2026. There are four types of catch-up contributions:

-

Age 50 catch-up contributions. Participants in 401(k), 403(b), or 457(b) plans can save an additional $8,000 in 2026, as long as they will be age 50 or older by the end of the year.

-

Age 60 to 63 catch-up contributions. Participants in 401(k), 403(b), or 457(b) plans, who will be between the ages of 60 and 63 by the end of 2026, can save an additional $11,250 in 2026.

-

Fifteen-year catch-up contributions. People who participate in a 403(b) plan and have completed 15 years of service with their organizations can contribute a higher amount to their plans annually, regardless of age. The lifetime limit for these catch-up contributions is $15,000.

-

Three-year catch-up contributions. People who save in a 457(b) plan can defer up to twice the annual contribution limit during the three years before normal retirement age (as established by the plan). The amount of the catch-up contribution depends on amounts previously saved in the plan.

In general, one type of catch-up contribution cannot be combined with another type of catch-up contribution. You must choose which to make.

If you have questions about your workplace retirement plan, please get in touch. Just as important, if you don’t have a workplace retirement plan and would like to begin saving for retirement, please contact us. There are other tax-advantaged ways to save for retirement.

| | |

AJ Advisors

www.ajadvice.com

|

|

|

Phone: (615) 709-8709

Fax: (615) 709-8709

| |

| |

John Stauffer, CFP®

Partner

| |

Andrew Quinn, CFP®

Partner

| | Past performance does not guarantee future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, strategy, or product (including those recommended or undertaken by AJ Advisors, LLC), or any non-investment related content, made reference to directly or indirectly in this communication will be profitable, equal any indicated historical performance level(s), be suitable for your portfolio or individual circumstances, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. You should not assume that any discussion or information contained in this communication serves as the receipt of, or as a substitute for, personalized investment advice. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to their individual situation, they are encouraged to consult with the professional adviser of their choosing. AJ Advisors, LLC is neither a law firm nor a certified public accounting firm and no portion of the content herein should be construed as legal or accounting advice. If you are an AJ Advisors, LLC client, please remember to contact the firm, in writing, if there are any changes in your financial situation or investment objectives or if you wish to impose, add, or modify any reasonable restrictions on our investment advisory services. Until so notified, AJ Advisors, LLC will continue to rely on the most recent information provided. A copy of our current written disclosure statement discussing our advisory services and fees continues to remain available upon request. | | | | |