TAX+BUSINESS

ALERT

News for your business and your life.

| Hawkins Ash CPAs

|

|

In this edition

January 21, 2020

Every Business Owner Needs an Exit Strategy

PODCASTS:

Legislation Updates: How They Affect Your Tax and Financial Planning

Do You Know Your Tax Bracket?

Determining an Employee’s “Home” for Reimbursement Purposes

Tax Calendar

|

|

|

Every Business Owner Needs an Exit Strategy

|

|

As a business owner, you have to keep your eye on your company’s income and expenses and applicable tax breaks. But you also must look out for your own financial future. And that includes creating an exit strategy.

Buy-Sell Agreement

When a business has more than one owner, a buy-sell agreement can be a powerful tool. The agreement controls what happens to the business if a specified event occurs, such as an owner’s retirement, disability or death. A well-drafted agreement provides a ready market for the departing owner’s interest in the business and prescribes a method for setting a price for that interest. It also allows business continuity by preventing disagreements caused by new owners.

A key issue with any buy-sell agreement is providing the buyer(s) with a means of funding the purchase. Life or disability insurance often helps fulfill this need and can give rise to several tax issues and opportunities. One of the biggest advantages of life insurance as a funding method is that proceeds generally are excluded from the beneficiary’s taxable income, provided certain conditions are met.

Succession Within the Family

You can pass your business on to family members by giving them interests, selling them interests or doing some of each. Be sure to consider your income needs, the tax consequences, and how family members will feel about your choice.

Under the annual gift tax exclusion, you can currently gift up to $15,000 of ownership interests without using up any of your lifetime gift and estate tax exemption. Valuation discounts may further reduce the taxable value of the gift.

With the gift and estate tax exemption approximately doubled through 2025 ($11.4 million for 2019), gift and estate taxes may be less of a concern for some business owners. But others may want to make substantial transfers now to take maximum advantage of the high exemption. What’s right for you will depend on the value of your business and your timeline for transferring ownership.

Get Started Now

To be successful, your exit strategy will require planning well in advance of retirement or any other reason for ownership transition. Please

contact us for help.

|

|

|

|

Contact:

Matt Cantlon

Direct: 507.252.6672

|

|

PODCASTS:

Legislation Updates: How They Affect Your Tax and Financial Planning

|

|

|

|

Planning for Year-End Spending Package Extenders

|

From extensions for individual and business expenses

—

including the Work Opportunity Tax Credit

—

to a change in the kiddie tax, catch up on some of the latest laws and updates.

|

|

|

|

SECURE Act: Part I – New Rules for 401(k)s and IRAs

|

Signed in December 2019, the SECURE Act made a number of changes to 401(k) plans, to Individual Retirement Accounts (IRAs) and to help smaller employers set up their own plans.

|

|

|

|

SECURE Act: Part II – Do the New Distribution Rules Affect You?

|

What happens to 401(k)s and IRAs after someone passes away? The SECURE Act outlines some new distribution rules that might affect you.

|

|

Do You Know Your Tax Bracket?

|

|

Although the Tax Cuts and Jobs Act (TCJA) generally reduced individual tax rates through 2025, there’s no guarantee you’ll receive a refund or lower tax bill. Some taxpayers have actually seen their taxes go up because of reductions or eliminations of certain tax breaks. For this reason, it’s important to know your bracket.

Some single and head of household filers could be pushed into higher tax brackets more quickly than was the case pre-TCJA. For example, the beginning of the 32% bracket for singles for 2019 is $160,725, whereas it was $191,651 for 2017 (though the rate was 33% then). For heads of households, the beginning of this bracket has decreased even more significantly, to $160,700 for 2019 from $212,501 for 2017.

Married taxpayers, on the other hand, won’t be pushed into some middle brackets until much higher income levels through 2025. For example, the beginning of the 32 percent bracket for joint filers for 2019 is $321,450, whereas it was $233,351 for 2017. (Again, the rate was 33 percent then.)

As before the TCJA, the tax brackets are adjusted annually for inflation. Because there are so many variables under the law, it’s hard to say exactly how a specific taxpayer’s bracket might change from year to year.

Contact us for help assessing what your tax rate likely will be for 2020—and for help filing your 2019 tax return.

|

|

|

|

Contact:

Curt Bach

Direct: 715.748.1351

|

|

Determining an Employee’s “Home” for Reimbursement Purposes

|

|

Despite the prevalence of web-based meetings, many of today’s businesses still have plenty of employees who travel. If you still have sales staff or other workers out on the road, and you’re reimbursing them on a tax-free basis for their travel expenses, it’s important for you as the employer to stay up to date on the rules that determine the location of a person’s tax home.

Principal Workplace

Internal Revenue Code Section 162 imposes three requirements for travel expense deductions:

- The expenses must be ordinary and necessary,

- They must be incurred while traveling away from the individual’s tax home, and

- They must be incurred in pursuit of business.

An employee’s “tax home” is generally determined by where he or she works, not by where the employee lives. A tax home isn’t limited to one building or property; it includes the entire city or area in which the tax home is located. For employees with one regular workplace, their tax home is that workplace. If an employee has more than one regular workplace, his or her tax home is the employee’s principal workplace.

If an employee has no principal workplace, his or her tax home is the employee’s “regular place of abode in a real and substantial sense.” Those who have no principal workplace and no regular abode are considered “itinerants,” and their tax home is wherever they work. Itinerants can never get a travel expense deduction or qualify for tax-free reimbursement of their travel expenses because they’ll never be “away from home.”

Three-Factor Test

The IRS uses a three-factor test to determine whether an employee with no principal workplace has a tax home or is itinerant. The three factors involve whether the employee:

- Performs a portion of his or her work near the claimed abode and uses that abode for lodging purposes when working there,

- Must leave the abode to perform his or her job, which duplicates the employee’s living expenses incurred at the abode, and

- Hasn’t abandoned the vicinity of his or her historical place of lodging and the abode; has marital or lineal family members currently residing at the abode; or uses the abode frequently for lodging.

If all three factors are satisfied, the individual’s abode is the tax home. If only two are satisfied, the answer will depend on the facts and circumstances, so you may need to consult with your tax advisors. If only one factor is satisfied, the employee is an itinerant.

The actual or expected length of an employee’s assignment to another location may affect whether the expenses are treated as incurred while “away from home.” Assignments of indefinite duration can change a taxpayer’s tax home, but temporary assignments won’t if the assignment is realistically expected to last, and in fact lasts, for one year or less.

Importance of Substantiation

Finally, keep in mind that travel expenses generally must be substantiated with information about the amount, time, place and business purpose of each expense. Our firm can help you determine your employees’ respective tax homes and follow the rules.

|

|

|

|

Contact:

Jeff Uhlir

Direct: 920.684.2550

|

|

January 31

File 2019 Forms W-2 (“Wage and Tax Statement”) with the Social Security Administration and provide copies to your employees.

File 2019 Forms 1099-MISC (“Miscellaneous Income”) reporting nonemployee compensation payments with the IRS and provide copies to recipients.

Most employers must file Form 941 (“Employer’s Quarterly Federal Tax Return”) to report Medicare, Social Security and income taxes withheld in the fourth quarter of 2019. If your tax liability is less than $2,500, you can pay it in full with a timely filed return. If you deposited the tax for the quarter in full and on time, you have until February 11 to file the return. Employers who have an estimated annual employment tax liability of $1,000 or less may be eligible to file Form 944 (“Employer’s Annual Federal Tax Return”).

File Form 940 (“Employer’s Annual Federal Unemployment [FUTA] Tax Return”) for 2019. If your undeposited tax is $500 or less, you can either pay it with your return or deposit it. If it’s more than $500, you must deposit it. However, if you deposited the tax for the year in full and on time, you have until February 11 to file the return.

File Form 943 (“Employer’s Annual Federal Tax Return for Agricultural Employees”) to report Social Security, Medicare and withheld income taxes for 2019. If your tax liability is less than $2,500, you can pay it in full with a timely filed return. If you deposited the tax for the year in full and on time, you have until February 11 to file the return.

File Form 945 (“Annual Return of Withheld Federal Income Tax”) for 2019 to report income tax withheld on all nonpayroll items, including backup withholding and withholding on pensions, annuities, IRAs, etc. If your tax liability is less than $2,500, you can pay it in full with a timely filed return. If you deposited the tax for the year in full and on time, you have until February 11 to file the return.

February 28

File 2019 Form 1096, along with copies of information returns with the IRS.

2019 tax returns must be filed or extended for calendar-year partnerships and S corporations. If the return isn’t extended, this is also the last day for those types of entities to make 2019 contributions to pension and profit-sharing plans.

|

|

More Resources from CPA-HQ

|

|

Congratulations to Our New Partner

The partners at Hawkins Ash CPAs recently voted to promote Vincent Schamber, CPA, to partner.

|

|

New W-4 for Use in 2020

2020 is here, and so is a revised Form W-4. This article provides a brief overview of the updates.

|

|

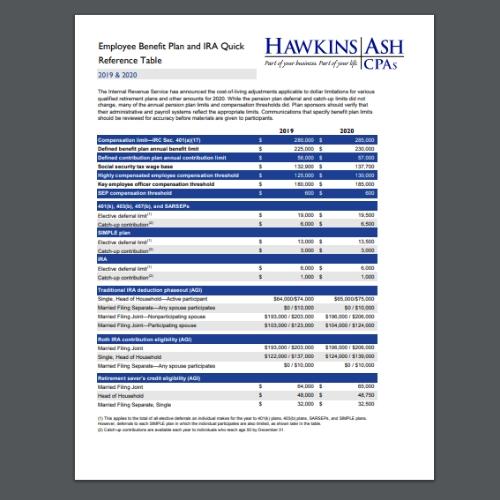

Employee Benefit Plan and IRA Quick Reference Table

Review these cost-of-living adjustments for the new year.

|

|

Part of your business. Part of your life. | www.HawkinsAshCPAs.com

|

|

|

|

|

|

|