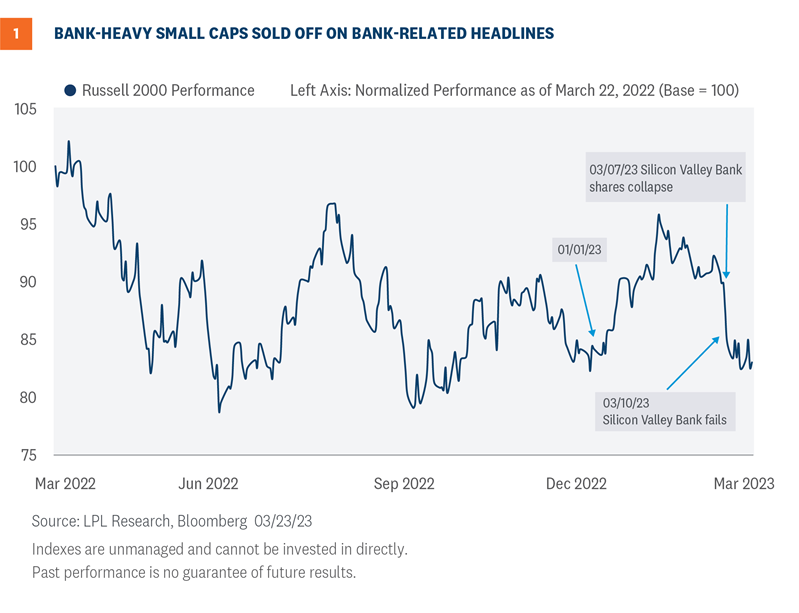

The swift crash of Signature Bank, the third largest bank failure in U.S. history, following the demise of SVB, which held $160 billion in deposits, along with Silvergate Bank, has investors and depositors questioning if the banking system is as “sound and resilient with strong capital and liquidity” as suggested recently by both Fed Chair Jerome Powell and Secretary of the Treasury Janet Yellen.

To be sure, the Fed’s emergency bank lending facility, the Bank Term Funding Program, which was quickly put in place to help strengthen the banks, also served to restore confidence as banks grapple with depositors who are seeking higher rates elsewhere, and who are also increasingly concerned about the viability of the banks themselves.

Finger pointing: Who’s to blame?

No sooner had news regarding the run on SVB hit the media, generalized fear and panic spread quickly. Depositors mounted a modern-day run on the bank using their smart phones, and over the course of 36 hours, the bank was forced to sell $21 billion of long duration bonds at a loss of $1.8 billion.

The blame was quickly focused on venture capitalists who sent out immediate warnings to their start-up companies to withdraw their funds at once. SVB’s large client base was broadly made up of fledgling technology companies backed by venture capital. It didn’t take long for depositors to exit.

A widely followed newsletter that covers the venture capital world, “The Diff,” has also been considered the spark that led to the mass exodus of deposits, when in late February the report indicated that SVB’s debt-to-asset ratio was 185 to 1, implying that the bank was virtually insolvent. The underlying culture of the tech world has also come under scrutiny as to how rapidly conclusions were drawn and how instantaneously they were acted upon.

Mismanagement and regulatory failures

The deficit of a functioning risk management team has been the most enduring criticism of SVB, while criticism has similarly been leveled at the supervisory team at the San Francisco Fed, which is supposed to monitor the operations of the banks within its regulatory jurisdiction. The lack of communication from the bank’s senior leadership didn’t help matters.

Silvergate Bank, with $12 billion in deposits, is most closely associated with crypto activities, but suffered a swift run on its holdings around the same time as the SVB failure. Despite early warnings of fragility in the wider crypto world, and with risks climbing, there was apparently, according to media reports, little contact with supervisors from the San Francisco Fed.

At the Federal Open Market Committee (FOMC) meeting press conference on March 22, Powell addressed criticism that there wasn’t any supervision of operations at SVB. He stressed that there were red flags raised months ago by examiners from the San Francisco Fed, but he couldn’t say whether the warnings were escalated. “We’re doing the review of supervision and regulation,” Powell said, and “My only interest is that we identify what went wrong here.”

Senator Elizabeth Warren, the leading Democrat on the Senate Banking Committee, blamed Powell for the banking crisis in no uncertain terms, saying that he was an integral part of the process that weakened regulatory oversight of regional banks, “Fed Chair Powell’s actions contributed to these bank failures.”

Monetary and fiscal policy

Moving up the blame chain leads directly to the monetary and fiscal policies that flooded the banking system with government transfers to consumers and small businesses, coupled with interest rates that stayed near zero for too long, which allowed risk to intensify across the investing spectrum.

With the Fed’s insistence that the inflationary effect was “transitory” and primarily due to COVID-19-related supply chain challenges, the central bank was slow to begin raising interest rates. With financial conditions remaining loose, risk taking was elevated in venture capital, private equity, and real estate, especially commercial real estate. But as the Fed finally launched its aggressive rate hiking campaign, the dynamic changed.

The collapse of SVB, followed by the other banks that were victims of the immediate panic that ensued, is emblematic of the changing landscape. When all is said and done, the blame falls on all of the above for failing to recognize the risks associated with policies that allowed risk taking but then quickly turned off the spigots.

Asset Allocation Views

In the current environment of elevated volatility and concerns about banks, LPL Research believes tactical investors should still maintain multi-asset allocations at or near benchmark levels with an emphasis on diversification.

Within fixed income, LPL Research continues to like the preferred sector to take advantage of attractive valuations with less risk than equities.

Within equities, the technology sector looks better to us here, which, along with the Strategic and Tactical Asset Allocation Committee’s (STAAC) recent decision to downgrade healthcare to neutral, suggests limiting the size of any style tilts toward value. The Committee continues to take a wait and see approach on the banks while closely watching the latest developments. Finally, precious metals-related investments warrant consideration on the long side, in our view.

Quincy Krosby, PhD, Global Macro Strategist, LPL Financial

Jeffrey Buchbinder, CFA, Chief Equity Strategist, LPL Financial