|

The Bank of Canada (BoC) has an upcoming rate announcement on October 25th, tomorrow. Many analysts, but not all, believe that the BoC will likely increase the prime rate again. A quarter point increase would bring Bank Prime from 7.20% to 7.45%. Why? The BoC sees the economy as not yet cooling and would much prefer a recession to further inflation. Of course, the ideal result is the prime rate increases to date (4.75% in rate increases since 2022) will produce a “soft landing” and not a full-blown recession. For the leadership at the BoC, if we get a hard landing, so be it, we need to get this plane on the ground.

What makes the BoC’s approach easier to understand is the number of Canadian home owners with mortgages rolling in 2024 and 2025 (35%+ of home owners have low rate term loans rolling in this period). If the BoC cannot lower rates by 2025, it could lead to significant pain and insolvency across the country. Ottawa and the BoC are desperate to avoid this scenario.

How is this impacting commercial mortgages? Variable rate loans (land loans and construction loans) are moving ahead, but with meaningfully larger interest reserves. Most loans are at approximately Prime + 1.0% (8.20% today). Citifund is arranging new land loans and new construction loans every month. The clients moving forward in the fall of 2023 are better capitalized and can deal with the larger equity requirements. Positively, select condo product and industrial product is selling (see project examples below). At this moment, there seems to be a decent volume of viable projects in good locations along with some unviable projects in less popular locations.

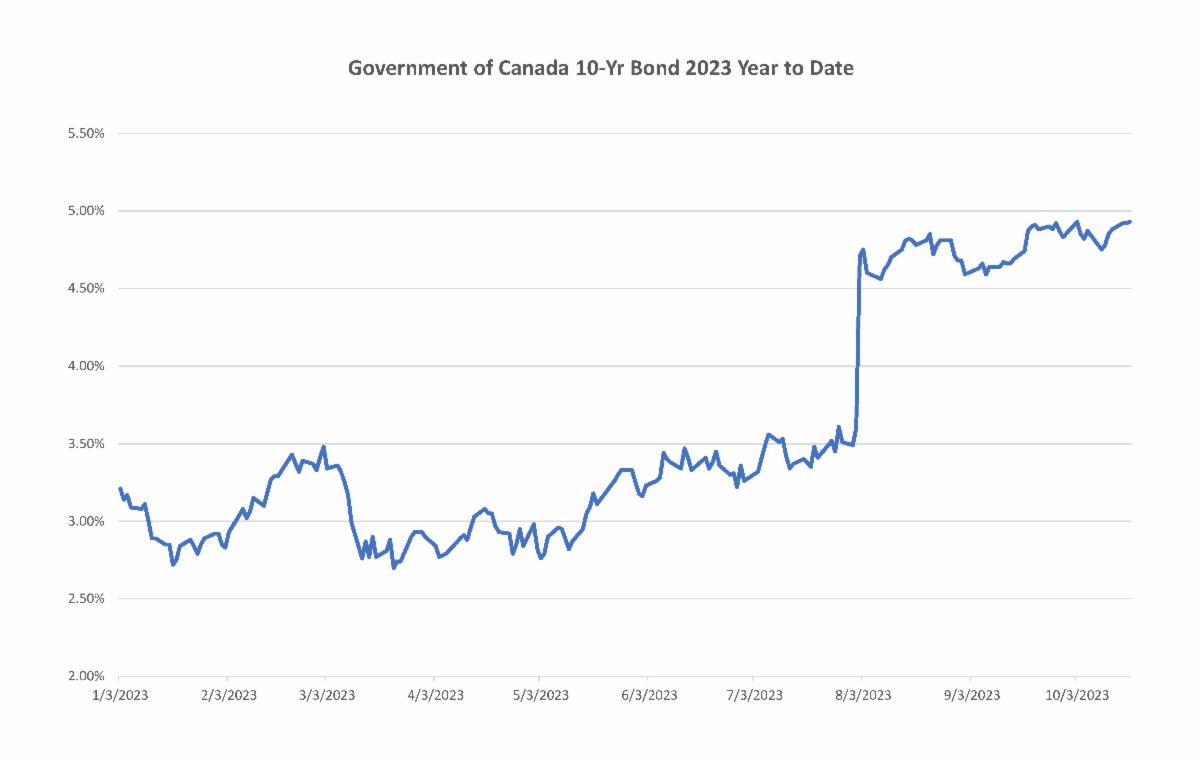

Regarding the CMHC, the MLI Select product has been wildly popular given its ability to deliver up to 95% loan to cost construction financing with a 50-year amortization. The current bond yields (10-year CMHC rates of approximately 5.0%) are requiring more equity. See the CMB chart below. In April 2023, our CMHC applications had ceiling rates of +/- 3.90%. This 110-basis point increase is moving the average apartment leverage from up to 95% loan to cost to approximately 83% loan to cost (with land at value). Generally speaking, CMHC insured apartment projects are moving ahead with clients prepared to invest 10% to 15% more in equity than they would have needed in the spring of this year. That said, rising rental rates are softening the impact of interest rate increases and there are some secondary markets (with low land costs) that are still allowing full 95% LTC leverage.

In addition to bond yields increasing, CMHC announced in April that premiums would be increasing after June and that “underwriting tests would be reviewed”. This announcement led to an unprecedented number of spring applications. The backlog of applications is still being assigned and timelines with CMHC are now unusually long. More importantly, beyond the premium increases and the timelines is the “underwriting review”. CMHC is tightening the MLI Select program with a variety of new rules and regional restrictions. The CMHC insurance path is still open and attractive but harder to navigate. As a long standing CMHC correspondent with a market leading volume of business Citifund continues to get investment and construction insurance approved but the process is requiring much more data and negotiation.

Given the challenges mentioned above, many clients are opting for shorter term product, such as two year term loans, in anticipation of a more favorable mortgage market in 2025.

For any questions on Land, Investment, Construction or CMHC financing, please contact a Citifund broker.

|