|

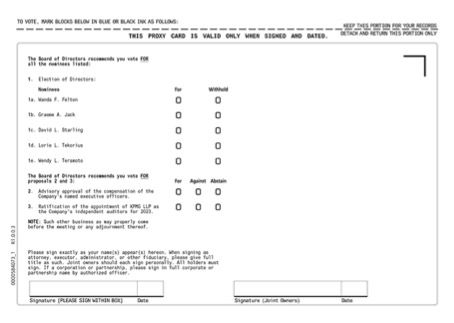

At this ASM, each of five candidates ran unopposed. So, five people for five BoD seats. GBX has a majority vote standard.

For each of the five, shareholders can vote "For" or "Withhold". A withhold campaign would urge shareholders to not vote "For" some or all candidates, and instead check "Withhold". What does this accomplish?

Realistically, nothing. Withhold votes seek to trigger a majority vote problem for a candidate. As we've shown before, the majority vote standard almost never serves to remove a director.

Mechanics of Withhold Votes

The "withhold" vote is in part a placeholder. It allows a shareholder to show affirmatively it opposes a given candidate. Depending on a company's bylaws, a shareholder could have the same impact if it leaves that candidate's line blank. "Withhold" just gives a shareholder something to check if it doesn't like the candidate.

At some companies, the majority vote standard means a director needs a majority of "For" votes at the ASM, relative to the total number of votes cast. So, a "Withhold" vote just helps a shareholder to not vote "For" a director. It gives them something else to check-off.

At other companies, including GBX, the majority vote standard works more strictly. A candidate that receives more "Withhold" votes than "For" votes means he or she failed to receive a majority of votes cast for that candidate. This then triggers the resignation process within the majority vote mechanics.

Sometimes, a "Withhold" vote is more than a placeholder. After all, "Withhold" means the shareholder literally declines to grant authority to the proxy holder (the company) to vote on its behalf. Suppose a shareholder leaves the director's line blank, and does not vote either "For" or "Withhold". If the company's voting rules so provide, then it will have authority to vote at its discretion. Of course, it will use that discretion to vote "For" that director. Then, a shareholder could vote "Withhold" to protest, and prevent the company from voting "For" instead. But, even if the "For" votes fall short, and the director fails to win a majority, nothing ever happens, see above...

What about companies without majority vote?

Then you're really wasting your time. For the half of US companies that don't have a majority vote standard, we can't think of any reason to run a withhold campaign. A "Withhold" vote will have literally no impact on the outcome, either mechanically or practically.

Universal proxy makes withhold even less relevant

If the voting rules allow it, then withhold votes can in principle affect the outcome of a director election, say in the GBX example. Yet, in the few times they trigger a majority vote failure, they almost never result in the director actually leaving the BoD.

So, an activist can run a withhold campaign and likely see nothing happen at the company. Or, it can nominate one or more candidates using UPC, and pressure the company seriously. A proxy contest does cost more than a withhold campaign. The SEC rule making on UPC reminds us how an activist can prosecute a proxy contest economically.

"Withhold" was a reasonable, if ineffective way for an activist to object to a company's directors. With UPC, activists now have a much better way to do that.

|