Here are the next two fables in our continuing special series on myths of private credit:

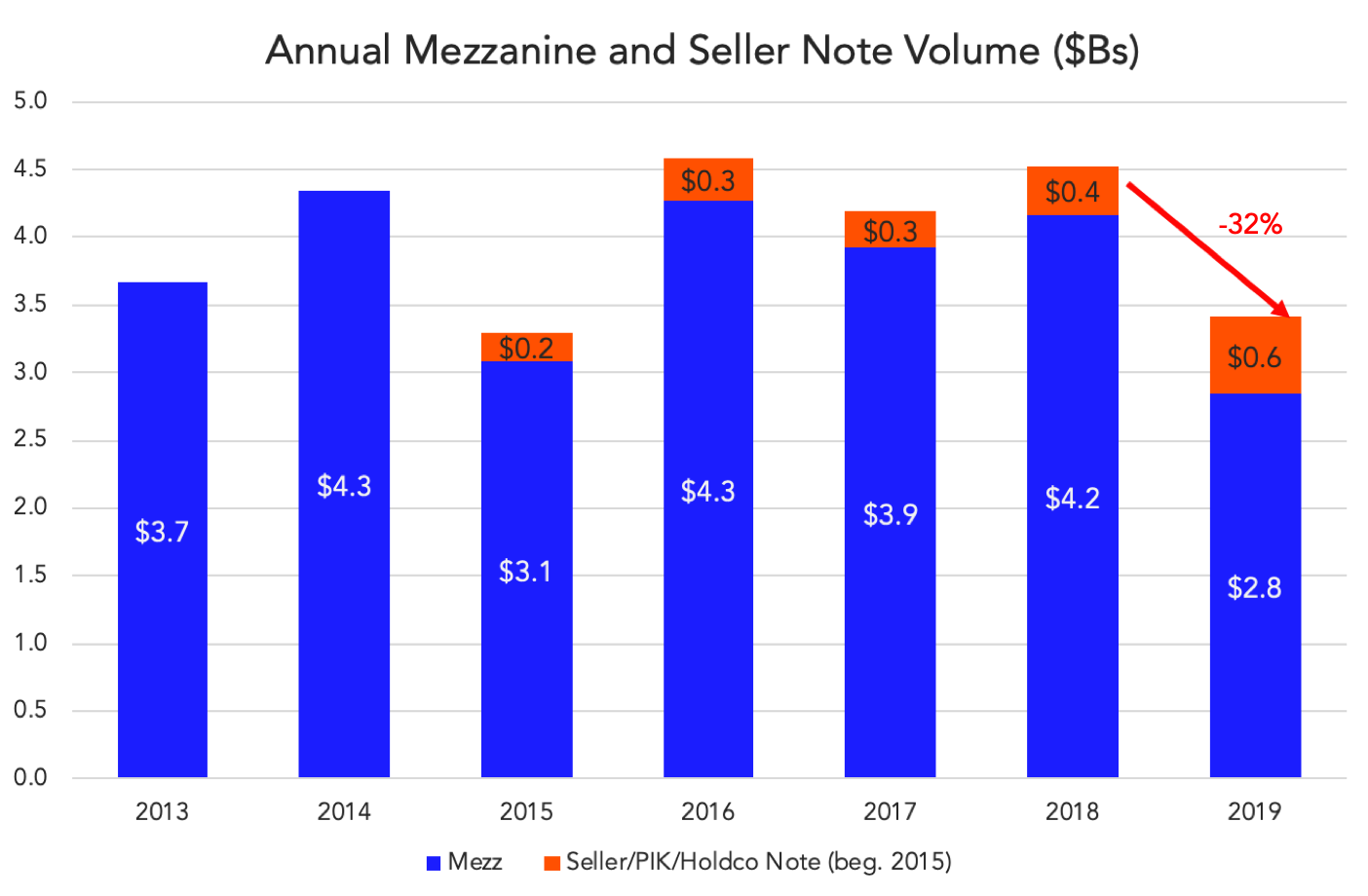

Myth #5: “No one uses mezzanine debt anymore.”

As we detailed over four years ago (

link

), private sub debt regularly gets kicked around at conferences for being “dead.” This has particularly been the case since the advent of the unitranche, which has certainly disintermediated a share of senior/junior two-tranche financings.

Yet mezz (or whatever you want to call it – sub or junior debt, second lien, PIK notes) has been a feature of the private capital landscape for decades and remains as active as ever. Why? In part because of its use as a private equity substitute...