We spent our winter break last week at an Arizona dude ranch. In the horse barn we spotted a sign: “There will be a $5 charge for whining.”

Heading into the home stretch of our special series on private credit myths, we like the cost for complaining. For faithful readers of

The Lead Left

, however, there’s no charge.

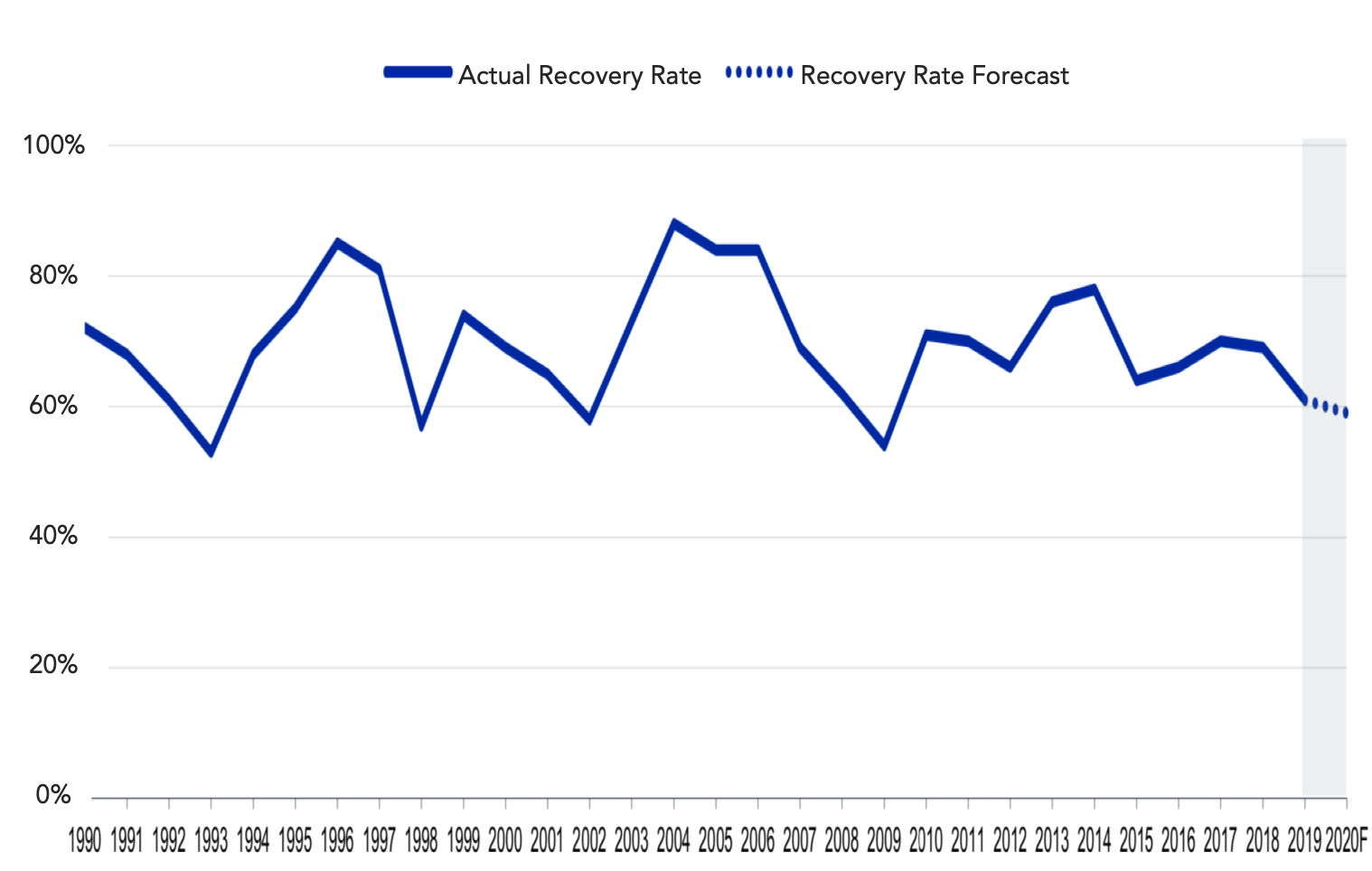

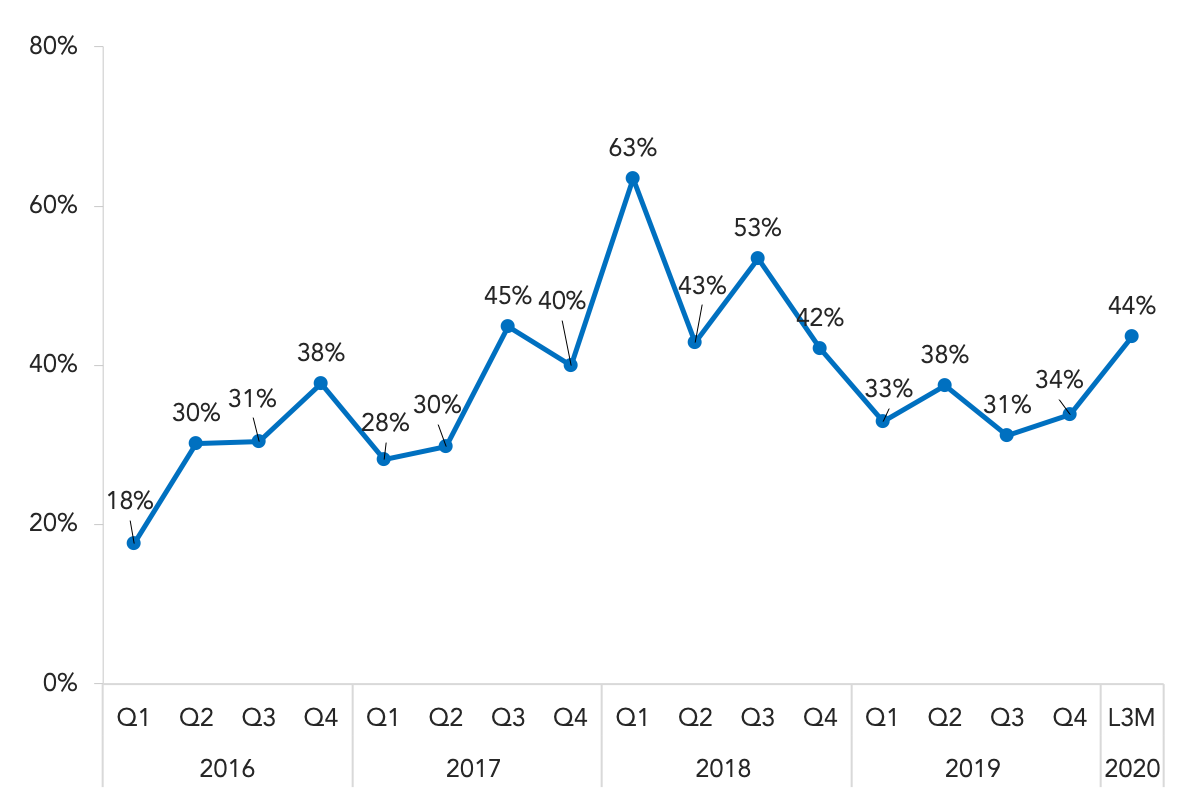

Myth #7: “Private credit recoveries will be worse than 2009”

The notion that leveraged loan performance will be worse during the next recession rests on the current prevalence of record high borrower leverage and cov-lite structures. If performance deteriorates, lenders have no triggers until a payment default...