|

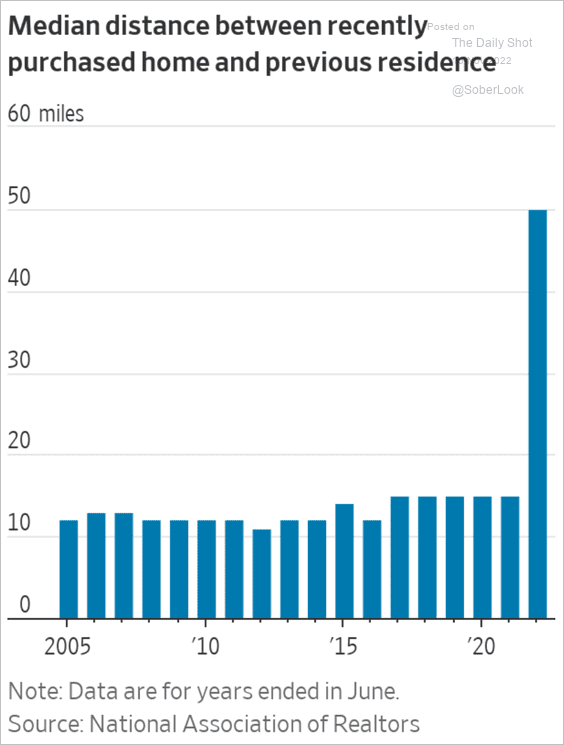

GETTING OUT OF TOWN

NAR surveys show that for the last 15 years the median distance between a new home and the buyer's previous residence was about 10-15 miles. Last year it was 50 miles. The NAR explains: "Family support systems still prevailed as a motivating factor when moving and in neighborhood choice. For others, housing affordability was a driving factor to seek homes in areas farther away. For many, remote work decisions were formalized in the last year, providing clarity for employees to permanently move to more distant areas."

The shares of buyers who purchased homes in small towns (29%) and rural areas (19%) were the highest ever recorded, while the shares of homes purchased in suburban (39%) and urban (10%) locations declined from one year ago.

|