|

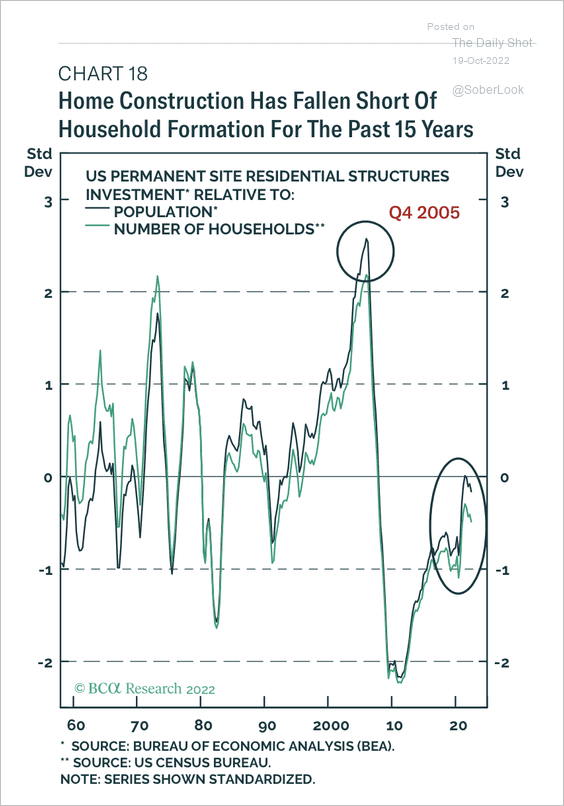

This factor by itself should create strong demand for new homes but there’s another underlying factor, and it a tsunami. The chart below shows the longer term trend for three key age groups: 20 to 29, 25 to 34, and 30 to 39 (the groups overlap). We can see the surge in the 20 to 29 age group last decade (red). Once this group exceeded the peak in earlier periods, there was an increase in apartment construction. This age group peaked in 2018 / 2019 (until the 2030s), and the 25 to 34 age group (orange, dashed) will peak around 2023. The 30 to 39 age group (blue) is important for buying and will be increasing over this decade. The current demographics are now very favorable for home buying - and will remain positive for most of the decade. For Houston, the annual number of 30-39 years will range between 1.2 and 1.6 million, roughly 15-20% of the region's total population.

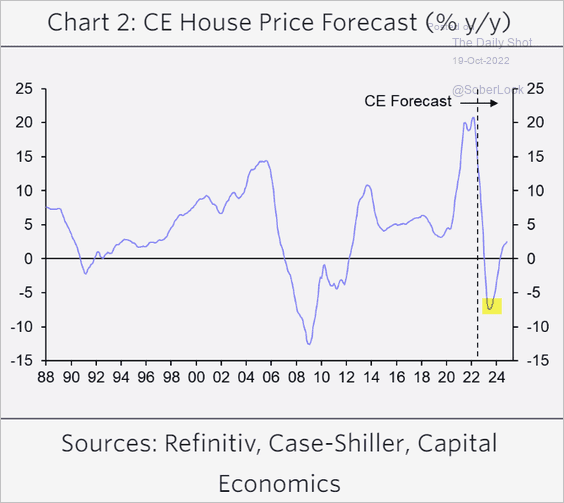

It’s very likely that we will have gone through the virtual decimation of our industry at the hands of the Fed to control home price inflation, only to have exactly the same factors driving home prices higher reappear as soon as we emerge from any likely recession. That’s one more reason why “I’m here from the government and I’m here to help you” remain the scariest words in the English language.

|