|

Dear Clients and Friends,

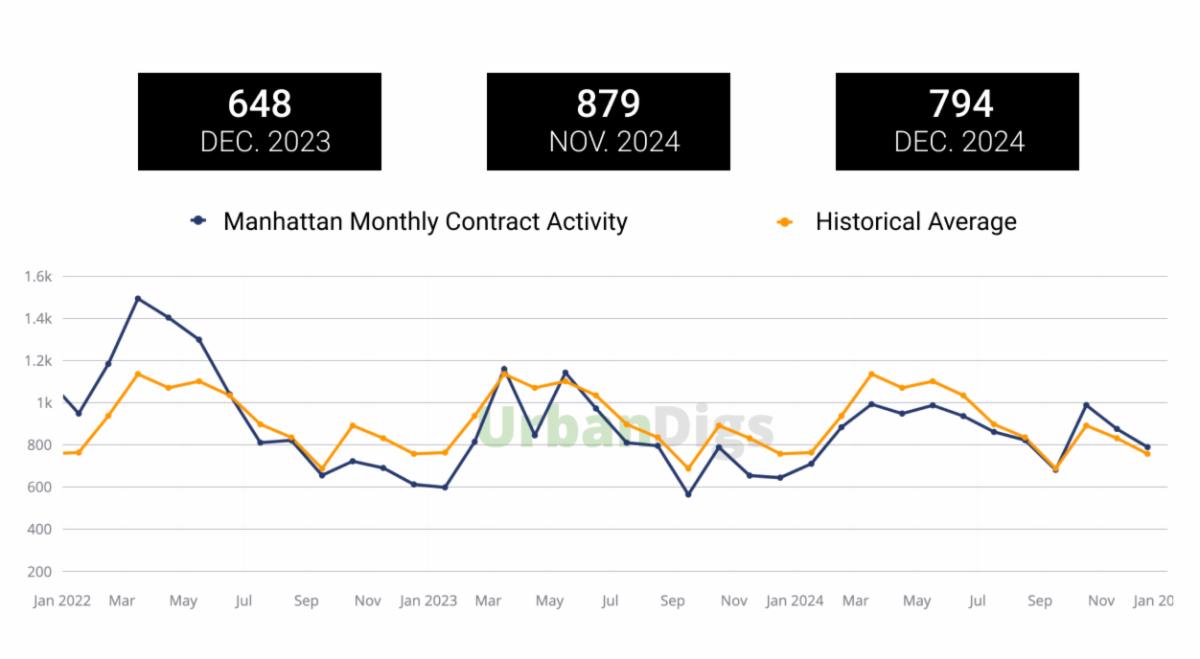

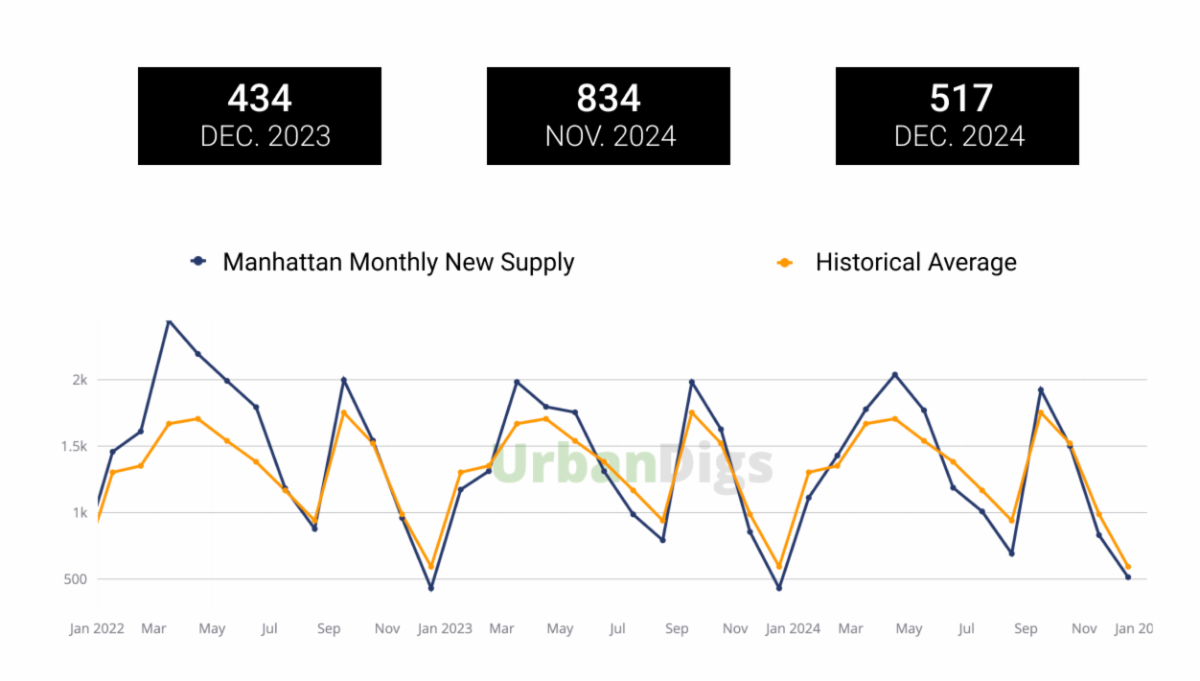

While both new listings and signed purchase contracts declined in December 2024 versus November 2024, the drop in new apartment inventory was nearly 20% greater than the dip in contracts signed. Generally, buyer/seller leverage is ‘neutral’ in the NYC residential market, though slightly favoring sellers of prime product due to a lack of supply. That said, individually evaluating each properties’ micro-location, renovation level, and alignment with buyer-preferences is more crucial than ever in determining strategy and pricing.

There were 144 contracts signed in December for Manhattan properties above $4M (up from 124 in November). The luxury sector has consistently outperformed the broader market throughout 2024, driven by affluent rate-insensitive buyers, gains in the stock market, and several trophy new development projects coming to market. Brooklyn townhouses have also had a banner year, breaking records for individual asking price, price/square foot, and volume of contracts signed. In fact, the number of Brooklyn townhouse contracts signed from July – November 2024 was 88% higher than the same time-frame last year. We are personally now seeing prime Brooklyn neighborhoods (Brooklyn Heights, Boerum Hill, Cobble Hill, Carroll Gardens, etc.) compete for the same buyers as coveted downtown Manhattan locations like Tribeca and Greenwich Village.

Looking forward to 2025, we are confident that NYC will remain a top global destination to buy, sell, and invest, as evidenced by the significant residential, office, and retail commitments made over the last year. The City offers a unique combination of preeminent schools, a diversified base of finance/tech/fashion/media industry hubs, and a highly walkable plethora of adjacent neighborhoods with distinct cultural, retail, and architectural offerings.

Sincere thanks you for your valued trust and business as always!

|