|

Key Issues Facing the U.S. Rice Market

The current state of the U.S. long-grain rice market raises several pressing questions regarding policy and market dynamics. Among these are whether the United States should increase its GSM-102 export credit guarantees for rice to alleviate low milling supplies, whether regulatory limits should be placed on large speculators who are exerting significant influence over the market by holding extensive short positions, and whether there should be restrictions on rice imports from countries where farmers receive substantial government support that ensures profitable production levels. These are all vital questions that warrant thorough consideration and action.

The Situation for U.S. Rice Producers

U.S. rice producers are experiencing economic hardship, with November futures at $10.75 and southern cash prices ranging from even to $0.40 above futures, but even lower in the delta. Most need $15.50–$17.00 just to break even, so current prices fall 33%–40% short, causing significant financial pressure. As a result, many farmers are thinking about quitting, while some who want to continue farming face bankruptcy. As one banker said in a recent meeting, “It is going to be a long winter working to get these guys refinanced.”

For the 2026 crop cycle, financial challenges include a 20-30% increase in fertilizer prices, equipment repair costs rising by 6-9%, and persistent labor shortages affecting all sectors. Nevertheless, the predominant concern for most farm budgets as 2026 approaches will be the market price of rice.

Rice Supply & Export Trends

According to the latest WASDE report, the ending stocks for the 2025–2026 crop year are projected to be 35.4 million cwt of long-grain rice. Despite this inventory, widespread adverse weather conditions across all major growing regions have led to lower milling quality compared to previous years. This decline in quality has negatively affected demand for U.S. long-grain rice.

In terms of exports, the data shows a significant downturn in the 2024–2025 crop year, with exports falling by 14.3 million cwt, representing a 19% decrease from the prior year. Although the current estimates for the 2025–2026 crop year anticipate an increase of 3.2 million cwt year-over-year, this figure remains well below the export levels achieved in the 2023–2024 crop year.

This export demand loss can be attributed to the very poor milling grades across the entire long-grain rice six-state growing area along with bumper crops grown in South America which Central American buyers were able to source with much better milling yields.

U.S. Long Grain Rice Competition

Historically, South America was not a significant exporter of rough rice. However, in recent years, increased production in the region has resulted in a surplus available for export. Despite this development, the most significant global competitors for U.S. long-grain rice continue to be India, Thailand, and Vietnam.

In March 2025, the International Trade Commission published a report titled “Rice: Global Competitiveness and Impacts on Trade and the U.S. Industry.” This report provides a detailed examination of the unfair trade practices employed by competing countries, shedding light on the substantial challenges faced by the U.S. rice industry in terms of global demand. In summary, the competitive environment for U.S. rice producers is far from a level playing field.

Short-Term Policy Solutions

Addressing Supply to Stabilize Prices

The longstanding adage claims that "low prices cure low prices," but experienced farmers recognize that this is not accurate. Reducing supply is necessary to address persistently low prices. Immediate action must be taken to tackle excess supply, or the industry risks a surge in bankruptcies among rice producers.

Expanding the GSM-102 Program

One potential measure to help alleviate the surplus of low milling long-grain rice in the U.S. involves the GSM-102 program, which provides export credit guarantees to encourage sales of rice and other bulk commodities to developing countries. Under this program, rice could be provided to eligible developing countries willing to accept a blend of white milled rice with up to 50% brokens. This may require USDA to add more countries to the GSM-102 eligible list, especially emerging markets with improving risk profiles and approve a wider base of foreign financial institutions for participation in the program. Although this proposal would include a relatively high proportion of broken rice, there is currently a large inventory of that is milling below 50 pounds of head rice in the United States. Certain countries, especially those facing food shortages, may be open to accepting this rice to feed their populations. Implementing this program would likely incur lower costs compared to emergency payments, and the expected reduction in inventory could result in increased rice prices, potentially offsetting the need for direct payments to farmers. While some producers may favor direct payments due to the time required to approve additional foreign financial institutions and reassess country risk profiles under GSM-102 arrangements, the program presents a viable alternative for inventory reduction and price support. In addition, as traditional food assistance programs such as Food for Peace are reformed by refocusing on its original purposes of using surplus U.S. agricultural commodities for foreign food assistance this rice could be utilized.

Imported Rice vs. Exported Rice Barriers

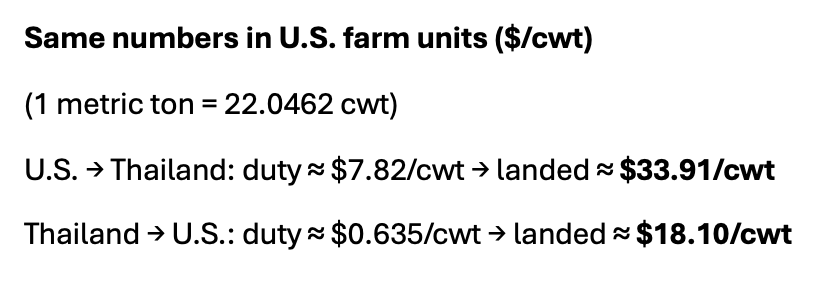

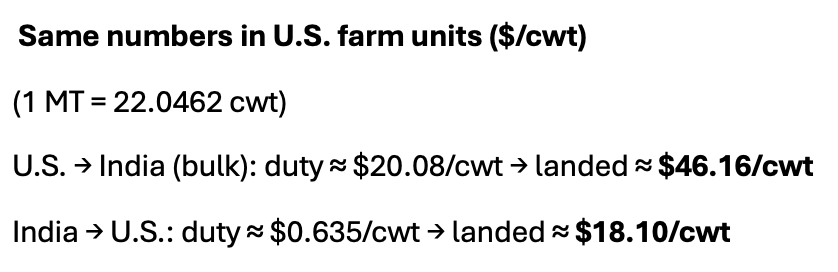

A major contributor to the large U.S. rice carryover supply is imports, which are at 44 million cwt — exceeding current ending stocks of 35.4 million cwt. While most imported rice is aromatic, about 2.4 million cwt is plain white rice competing with domestic crops. The U.S. is actively working to develop a Jasmine rice variety that can rival Thai Jasmine in both quality and scale. Last year, domestic production reached an estimated 2.1 million cwt. In comparison, Thai Jasmine made up 59.5% of all U.S. rice imports, totaling about 26.2 million cwt.

If we take the current export prices in Thailand ($385/mt) and the U.S. export price ($575/mt) and add the duty in each country, the U.S. price in Thailand goes up $172/ton. For rice imported into the U.S., the price goes up only $14/ton. See below:

|