| |

Most information reflected in this

report is through November 2025

By Karr Ingham

InghamEcon, LLC

| | |

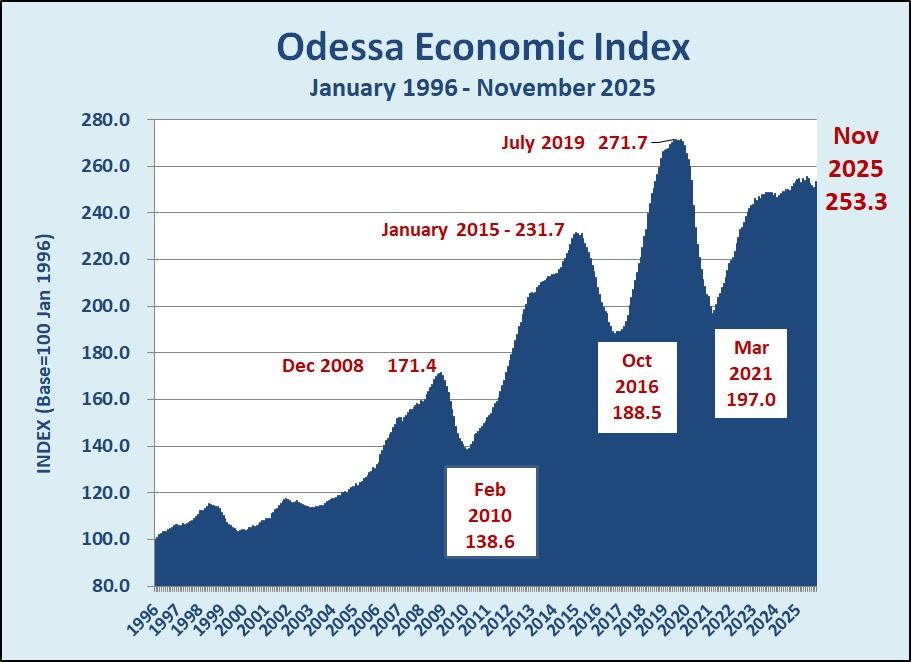

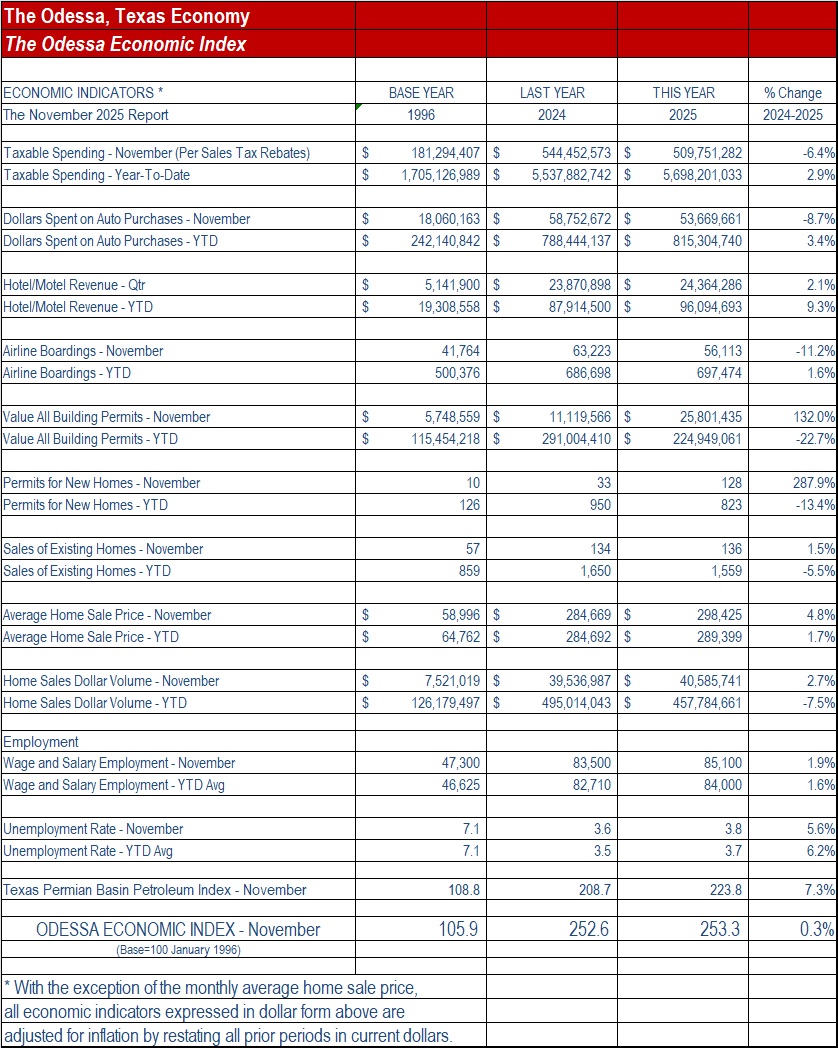

Following four straight months of decline, the Odessa Economic Index rebounded in November with a strong increase to 253.3 up from 251.0 in October, and up 0.3% from the November 2024 OEI of 252.6.

Whereas housing and construction have been in large part the culprit in recent months, they were the catalyst for the increase with strong numbers in November, at least compared to generally weak numbers in November 2024.

Existing home sales were up slightly in November, though still lower for the year-to-date, and the average price of those sales improved on sharply increased numbers from November of a year ago.

At the same time, however, general spending and auto spending were lower for the month, along with airport passenger activity. Current employment estimates – soon to be revised – continue to indicate modest job growth in Odessa, though the unemployment rate is still higher compared to its year-ago level.

| | The Texas Permian Basin Regional

Oil and Gas Economy | | |

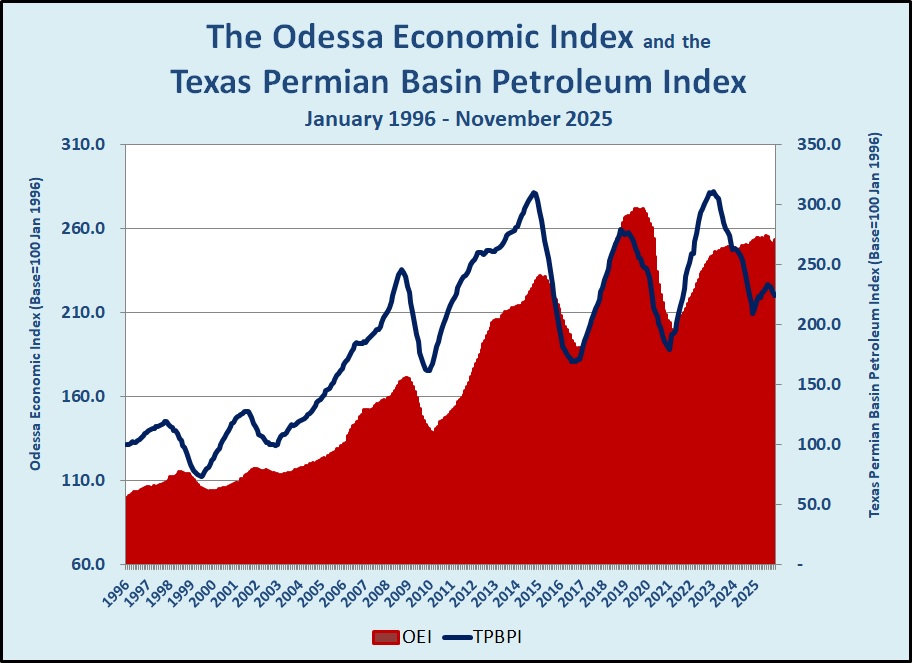

The Texas Permian Basin Petroleum Index continued its retreat in November declining to 223.8 for the month down from 226.9 in October, but still up 7.3% from the November 2024 TPBPI of 208.7. Lower crude oil and natural gas prices, along with a still-declining rig count and lower drilling permit numbers continue to push the index downward.

The monthly average crude oil price (WTI posted) of $55.43 was down by over 15% in November compared to the November 2024 monthly average (and down by 17.5% year-over-year in real terms). After spending the first eight months of the year in the black, regional natural gas prices (Waha Hub) turned negative in September, and that was also the case in October, and now again in November at a minus 46 cents/mmbtu.

The regional rig count (total of RRC districts 7C, 8, and 8A) also declined again in November dropping to 155 on average down from 158 in October, and down 24% from the November 2024 rig count of 205. The number of drilling permits issued in November was the lowest monthly total of the year at 249 and was off compared to the November 2024 total by close to 40%.

Crude oil production in the Texas Permian Basin has flattened considerably after topping out at over 4.5 million barrels per day in July 2024. Total Permian Basin crude oil production continued to climb throughout 2025, however, reaching an estimated 7.0 million barrels per day for the first time on record in November. Again, however, New Mexico is driving that growth with slowing production on the Texas side.

Direct upstream (exploration and production) oil and gas employment has flattened out in late 2025, but at or near record levels. Again, however, we must reiterate the possibility – even likelihood – that industry employment for 2025 will be revised downward in the coming weeks.

| | |

The Odessa General Economy

Updated data suggests that downward revision may indeed NOT be coming for total employment in Odessa, though only time will tell. But if that is true then the current estimates suggesting continued modest growth in Odessa employment may be more accurate than we may have thought.

That data continues to suggest modest employment growth – but again, growth nonetheless – through November at 1.9% year-over-year growth, or about 1,600 jobs added over the last 12 months. Unlike October, the Texas Workforce Commission released unemployment data for November, with an unemployment rate of 3.8% for the month, up from 3.6% in November 2024.

Elsewhere in the economy, the spending numbers were lower in November. General real (inflation-adjusted) spending per November sales tax rebate to the city was down by 6.4% compared to November 2024. That is only the third year-over-year decline in 2025, however, and the year-to-date total remains higher compared to its year-ago level by some 2.9%

| | |

The same is true of auto spending – lower for the month, but higher for the year-to-date. Inflation-adjusted spending on new and used motor vehicles was down in November by 8.7% compared to November 2024 auto spending, which in turn was down by 16% compared to November of the prior year. Year-to-date auto spending is still positive compared to year-ago levels, however, up by 3.4% compared to the first eleven months of 2024, which was a lower auto spending year compared to 2023.

The travel and tourism indicators were mixed with slightly higher hotel/motel spending for the quarter, but a drop in Midland International Airport passenger enplanements in November. The number of passenger boardings was the lowest for November since 2021, and the total was down by over 11% compared to November of a year ago.

The November building permit total was sharply higher compared to November of last year, but that is principally because the November 2024 total was very low – by far the lowest of 2024. The inflation-adjusted valuation of new commercial and residential construction was up by more than 135% year-over-year. That was not sufficient to reverse the year-to-date declines, however, and the permit valuation total remains down by about 22% compared to year-ago-levels.

| | |

Contributing to that increase was a solid month for new housing construction. The 128 new single-family housing permits issued was the highest monthly total in 2025 and was nearly four times higher compared to a relatively low total in November 2024. Again, however, the year-to-date total remains negative, down by about 13% compared to the total through November 2024.

Existing home sales were slightly improved in November, with two additional closed sales reported in November 2025. Year-to-date housing sales remain lower, however, off by 5.5% compared to the total number of sales through November of a year ago. Average prices continue to climb, however, with the November monthly average home sale price up by 4.8%, and the average for the year-to-date up by 1.7% over the average through November 2024, which in turn was up by 10% compared to the previous year.

The real (inflation-adjusted) dollar volume of existing home sales was up by 2.7% in November compared to November 2024, which in turn was up by a sharp 15% year-over-year. The year-to-date inflation-adjusted value of those transactions remains down by 7.5% compared to the first eleven months of 2024.

On balance, aggregate economic activity in Odessa remains generally solid, especially given lower crude oil prices and falling levels of exploration and production activity. That the Odessa economy has merely leveled off, as opposed to sharp or sustained decline, suggests a shifting nature of the oil and gas industry’s impact on the Odessa general economy.

| | For more information on how the Odessa Development Corporation can help your local business expand, contact our office at (432) 333-7881. | | Follow the Odessa Development Corporation: | | | | |