|

*This electronic message contains information that is intended exclusively for the use of the individual to whom it is addressed. It may not be redistributed or shared via social media.*

Please enable images to view this email in full.

To view this email as a web page: Click Here

| |

|

Last Week In Review

Monday, August 7, 2023

| |

|

■ ABS ISSUANCE SUMMARY

- ABS Supply In The Last 12 Months

■ MARKET PERFORMANCE

- Primary Market

- Secondary Market

■ FORWARD CALENDAR

- Pending Deals

- Recently Filed ABS-15Gs

| |

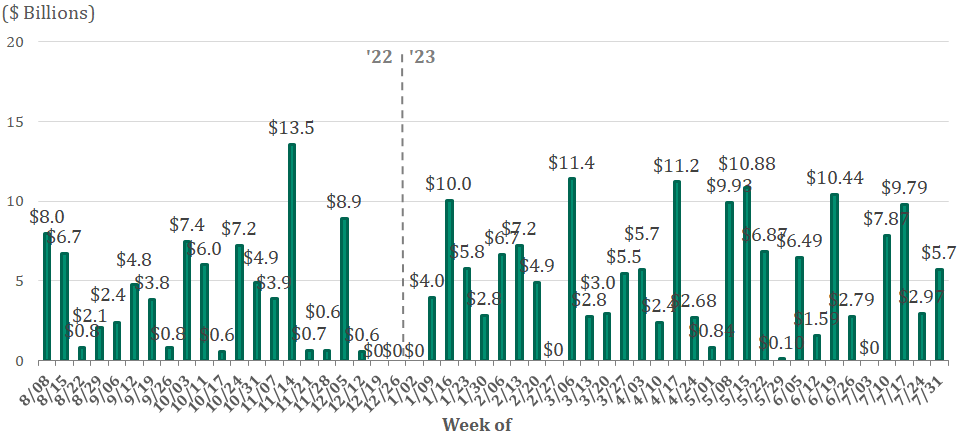

Last week, the US ABS new issue market saw nine issuers price $5.7 billion. | |

|

August MTD US ABS Volume

- Amount: $5.5 Billion

- # of Deals: 8

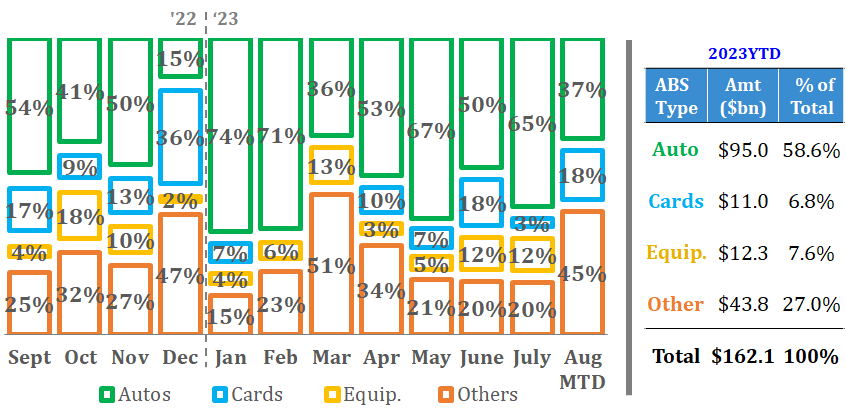

2023YTD US ABS Volume

- Amount: $162.3 Billion

- # of Deals: 238

- YoY: -15.13%

| |

ABS Supply (Last 12 Months) | |

ABS primary activity picked up last week after the market saw a slight slowdown the prior week. Issuance is expected to be heavy this week with 13 deals currently in the pipeline. | |

Last Week's Largest Deals by Type | |

|

Auto

Ford Credit Auto Owner Trust

FORDR 2023-2

Priced: 8/1/2023

Size: $1.38 Billion (Upsized from $820 Million)

| |

|

Cards

Synchrony Card Issuance Trust

SYNIT 2023-A1

Priced: 8/2/2023

Size: $1 Billion (Upsized from $500 Million)

| |

|

Others

Frontier Communications

FYBR 2023-1

Priced: 8/1/2023

Size: $1.59 Billion (Upsized from $1.06 Billion)

| |

|

NFP came and went. Last week was marked by increased volatility for the first time in several weeks. Spread volatility also increased. Many people questioned the downward movement in both the equity and bond markets last week. It is becoming clearer that the Fed is in a good place to continue to tread water, hoping that past rate increases continue to slow the economy while taking little nips out of inflation. Higher for longer really means higher for longer and the markets are starting to come around to this. With treasury supply announcements pointing to hefty issuance and short rates remaining elevated with no end in sight, the question becomes, does one really want to own duration? The market is adjusting, and the curve has been steepening as a result with short rates anchored. All of this has implications for structured products.

-

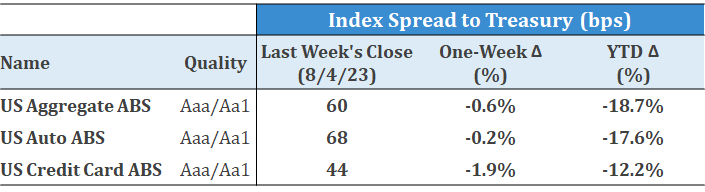

ABS – This shorter duration asset class continues to benefit from the inverted curve and quickly delevering assets. With the economy continuing to look strong and the soft landing scenario becoming much more popular, the consumer is becoming less feared. A month ago, the focus was on subprime delinquencies and losses. This has been supplanted by increased interest in these securities and other consumer-related ABS up and down the capital structure. Supply continues to be low. Not long ago, issuers were retaining their subs and now, there are not enough to meet demand. Last week, there was a bit more selling than we have seen but not enough to meet demand. This asset class has been supported by the technical created by the inverted curve and now the economic fundamentals have created a tailwind.

- CMBS – In the private label market, AAAs tightened 9 bps two weeks ago, and last week, there was good selling in the LCFs. This market is still cloudy with these assets still finding their footing. Also, if an investor wants to sell duration, this is a good sector to sell with these unknowns and recent tightening. In agency CMBS, there was the typical Freddie floating deal FHMS K-F159 that priced S+78. The non-lending banks are still buying and with the lack of DUS/PC supply, Freddie deals will continue to be well bid. We expect spreads to continue to ride these levels for DUS as we are right on top of the spread these banks need vs funding.

- MBS – Spreads were volatile, in line with the general market. We traded between the low 160s to mid 170s, finishing the week at the upper end of the range. We continue to watch the economic landscape as we increase the expectation for a soft landing where investors will want more credit risk. In addition, the lack of demand for duration will play a role as it did last week with the widening. Still, spreads for MBS are attractive and the supply outlook is dim at these rate levels while the FDIC is about 90% done with their selling. The technicals of this market will continue to support these spreads though we do not see further tightening in the near-term.

| |

|

Auto

Carvana Auto Receivables Trust 2023-n2

| |

|

Equipment

Leaf Capital Funding LLC

| |

|

Others

Nelnet Inc

Citi Held for Asset Issuance LLC

| |

DISCLAIMER

This electronic mail message and any attachments contain information that is intended for the exclusive use of the individual or the entity to whom it is addressed and may contain information that is proprietary and/or confidential. If you are not the intended recipient, please notify the sender, by e-mail or telephone of any unintended recipients and delete the original message without making any copies.

Information contained in this email is based on data obtained from sources we deem to be reliable. However, it is not guaranteed as to accuracy and does not purport to be complete. Nothing contained in this email is intended to be a recommendation of a specific security or company nor is any of the information contained herein intended to constitute an analysis of any company or security reasonably sufficient to form the basis for any investment decision.

*Sources: Bloomberg, Informa Global Markets, SEC EDGAR Filings.

© 2022 Cabrera Capital Markets LLC 227 W. Monroe St., Suite 3000, Chicago, Illinois, 60606

Additional information is available upon request. www.cabreracapital.com

| | | | |